Can NRIs Withdraw EPF?

Yes, Non-Resident Indians (NRIs) can withdraw their EPF (Employee Provident Fund) balance, but only under specific conditions. Typically, withdrawal is allowed after 2 months of unemployment or immediately if you have permanently left India for employment or settlement abroad. NRIs can apply online through the UAN portal or offline via EPFO claim forms. However, factors like tax deductions, the correct bank account type (NRO vs NRE), and proper documentation play a critical role in whether your claim gets processed smoothly or rejected. This process is also commonly referred to as PF withdrawal for NRIs or EPF withdrawal after moving abroad.

When Should NRIs Withdraw EPF?

- After leaving a job and completing 60 days without employment

- Immediately when moving abroad for work

- Avoid applying before eligibility to prevent rejection

NRI EPF Withdrawal Rules (Quick Answer)

- NRIs can withdraw EPF after 2 months of unemployment

- Immediate withdrawal allowed if leaving India permanently for work

- EPF must be credited to an NRO account (not NRE)

- TDS applies if the service is less than 5 years

- Withdrawal can be done online (UAN) or offline

Why Most NRI EPF Claims Get Stuck

- No access to the Indian mobile number (OTP issue during claim submission)

- Incorrect bank account (NRE account used instead of NRO)

- The employer has not approved the exit or the marked date of leaving

1. Eligibility for NRI EPF Withdrawal

Understanding eligibility is the first step—most claim rejections happen because users apply at the wrong time or under the wrong condition.

EPFO Rules for NRI EPF Withdrawal (Simplified)

Based on EPFO guidelines:

- EPF withdrawal is allowed after 2 months of unemployment

- Immediate withdrawal is permitted if the individual is leaving India for employment abroad

- KYC verification is mandatory before claim submission

- EPF funds are credited only to Indian bank accounts

Who is Considered an NRI for EPF?

For EPF withdrawal purposes, an individual is treated as an NRI when they are no longer residing in India and have taken up employment or settled abroad. In practical terms, EPFO considers you an NRI if:

- Your employment in India has ended, and

- You have moved abroad for work, business, or long-term residence

Unlike strict legal definitions under FEMA, EPFO focuses more on your employment status and relocation, rather than technical residency classification.

When Are NRIs Eligible to Withdraw EPF?

NRIs can withdraw their EPF balance under two primary scenarios:

1. After 2 Months of Unemployment

If you leave your job in India and are not employed for at least 60 days, you become eligible to withdraw your EPF. This is the standard rule applicable to most employees.

2. Immediately After Leaving India for Employment Abroad

If you relocate abroad for a job or permanent settlement, you may not need to wait for 2 months. EPFO allows immediate withdrawal in such cases, provided the correct exit reason is selected and supported with appropriate documentation.

Important Note

If you are still employed—either in India or through a structure linked to your Indian employer—you generally cannot withdraw your EPF balance.

NRI EPF Withdrawal Rules (Quick Matrix)

| Situation | Can Withdraw? | Timeline | Key Requirement |

|---|---|---|---|

| Left India permanently for work | Yes | Immediate | Passport/visa proof |

| Unemployed for 2 months | Yes | After 60 days | KYC completed |

| Still employed (India or abroad) | No | Not allowed | — |

This matrix simplifies the decision: eligibility depends primarily on employment status and location, not just residency label.

2. When Can NRIs Withdraw EPF?

Timing is one of the most misunderstood aspects of EPF withdrawal, especially for NRIs. Applying too early or under the wrong conditions is a common reason for claim rejection.

The 2-Month Rule

If you resign from your job in India, EPFO requires you to wait for 60 days of unemployment before you can withdraw your EPF balance. This rule applies even if you plan to move abroad but have not yet formally done so.

Immediate Withdrawal After Moving Abroad

If you have already left India for employment or permanent settlement, you may be eligible for immediate withdrawal. In this case:

- You must select the correct reason for exit (such as “abroad settlement”)

- Supporting documents, such as a passport or visa, may be required

- The employer should have marked your exit correctly

Edge Cases to Be Aware Of

- Direct switch to a job abroad: You may qualify for immediate withdrawal without waiting 2 months

- Short employment gaps: If your employment status is unclear, EPFO may still enforce the 60-day rule

- Incorrect exit reason: Selecting the wrong reason during claim submission can delay or reject your claim

Key Takeaway

Your eligibility timing is determined by how and when your employment ended, not just your NRI status. Ensuring that your exit is properly recorded and aligned with your actual situation is critical to a smooth withdrawal process.

3. How to Withdraw EPF for NRIs (Step-by-Step)

If you're an NRI, withdrawing EPF is less about “knowing the steps” and more about executing them correctly. Most failures happen due to OTP issues, KYC mismatches, or employer delays—not because people don’t know the process. This process is done through the UAN (Universal Account Number) portal, and is often searched as “UAN PF withdrawal process” or “EPF claim through UAN login.”

the

EPF Withdrawal Process for NRIs (Quick Steps)

- Log in to the UAN portal

- Verify KYC (Aadhaar, PAN, bank)

- Select claim form (Form 19/10C)

- Enter bank details (NRO account)

- Complete OTP verification

- Submit claim

Below is a practical, step-by-step breakdown of what to do, what can go wrong, and how to avoid delays.

Online EPF Withdrawal Process

The online method is the fastest and preferred route—provided your KYC and mobile access are in order. To start the process, log in to the UAN (Universal Account Number) portal, which is used for all EPF claims and account access.

Step 1: Log in to the UAN Member Portal

Visit the EPFO UAN portal and log in using your UAN and password.

What can go wrong:

- Password issues or inactive UAN

- OTP not received (common for NRIs)

Tip: Ensure your UAN is active and linked with Aadhaar before starting.

Step 2: Verify KYC Details

Go to the “KYC” section and confirm that your Aadhaar, PAN, and bank details are verified.

What can go wrong:

- PAN not linked → higher TDS

- Bank account not approved by the employer

- Name mismatch across documents

Tip: Your name must match exactly across Aadhaar, PAN, and bank records.

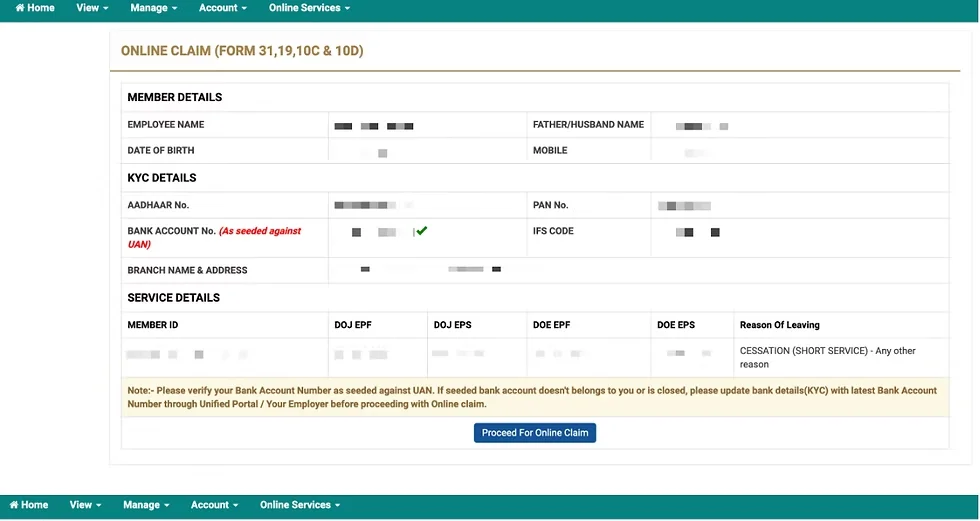

Step 3: Navigate to the Claim Section

Go to:

Online Services → Claim (Form 19, 10C, 31)

Step 4: Verify Bank Account

You will be asked to enter and verify your bank account details.

What can go wrong:

- Entering the NRE account instead of the NRO

- IFSC mismatch

- Dormant or closed account

Tip: Always use an active NRO account linked to your UAN.

Step 5: Select Type of Withdrawal

Choose the appropriate claim:

- Form 19 → EPF balance

- Form 10C → pension component

Step 6: Enter Exit Details

Select the reason for leaving:

- “Cessation (short service)”

- “Abroad settlement”

What can go wrong:

- Incorrect exit reason → rejection

- Employer has not marked exit

Tip: Check with your employer that your date of exit is updated. If your employer has not updated your exit, your claim may get stuck. Here’s how to fix employer approval delays in EPF claims → https://www.kustodian.life/resources/epf-claim-stuck-employer-approval-guide

Step 7: OTP Verification

An OTP is sent to your registered mobile number.

What can go wrong:

- No access to the Indian number

- OTP delays or failures

👉 This is the biggest blocker for NRIs.

Step 8: Submit Claim

Once OTP is verified, submit the claim.

You will receive a reference number to track the status.

Processing Timeline

- Typically: 7–20 working days

- Delays occur due to employer, KYC, or bank issues

Which EPF Forms Should NRIs Use

Understanding the correct forms is important to avoid incomplete withdrawals.

- Form 19 is used to withdraw your EPF (Provident Fund) balance

- Form 10C is used to withdraw your EPS (pension component) if you have less than 10 years of service

In most cases, NRIs should apply for both Form 19 and Form 10C together to withdraw the full amount.

| Form Name | Purpose | Eligibility / Condition | Result of Missing It |

|---|---|---|---|

| Form 19 | Withdraw core EPF balance | Standard withdrawal conditions | You leave your main PF corpus behind. |

| Form 10C | Withdraw EPS (Pension) | Total service must be less than 10 years | You leave your pension corpus behind. |

What can go wrong:

- Applying only for Form 19 → pension balance remains

- Confusion about eligibility for pension withdrawal

Tip: If your service is less than 10 years, ensure both forms are submitted to avoid leaving money behind.

Offline EPF Withdrawal Process

The offline method is useful when online withdrawal is not possible—especially for NRIs facing OTP or KYC issues.

When to Use the Offline Method:

- No access to the registered mobile number

- Aadhaar not linked

- Employer not cooperating

- KYC cannot be updated online

Steps:

- Download the Composite Claim Form (Aadhaar or Non-Aadhaar version)

- Fill in your UAN, personal details, and bank information

- Attach supporting documents:

- Passport (proof of NRI status)

- Bank proof (cancelled cheque)

- Sign the form (attestation may be required)

- Submit to the relevant EPFO regional office

What can go wrong:

- Missing or incorrect documents

- Signature mismatch

- No employer attestation (if required)

Tip: If you are submitting from abroad, you may need embassy attestation depending on your case.

How to Withdraw EPF Without an Indian Mobile Number

This is one of the most common and critical problems NRIs face.

Since EPFO requires OTP verification, not having access to your Indian mobile number can block the entire online process.

Option 1: Update Mobile Number via Employer

Your employer may be able to help update your mobile number linked to UAN.

Limitation: Not always reliable, especially if the employer is unresponsive.

Option 2: Use Aadhaar-Based Workaround

If your Aadhaar is linked and updated with a new number, OTP may be routed accordingly.

Limitation: Works only if Aadhaar is properly seeded and updated.

Option 3: Switch to Offline Process (Most Reliable)

If OTP access is not possible, the safest route is:

- Use the offline claim form

- Submit with the required documents

- Avoid dependency on OTP

Key Insight: For NRIs, offline is often more predictable than online, especially when mobile access is broken.

Common Errors During NRI Withdrawal

Even when the process is followed correctly, small mistakes can lead to delays or rejection.

1. Name Mismatch: Differences between Aadhaar, PAN, and bank records can cause claim failure.

2. Incorrect Bank Account: Using an NRE account instead of an NRO leads to rejection.

3. PAN Not Linked: Results in higher TDS (up to 30%).

4. Employer Has Not Marked Exit: Without an exit date, withdrawal cannot proceed.

5. KYC Not Verified: Unapproved KYC details block claim submission.

Final Takeaway: The EPF withdrawal process for NRIs is straightforward on paper—but in practice, it depends heavily on:

- Clean KYC

- Correct bank setup

- Employer coordination

- Mobile access

Getting these right up front can save weeks of delays and prevent rejection altogether.

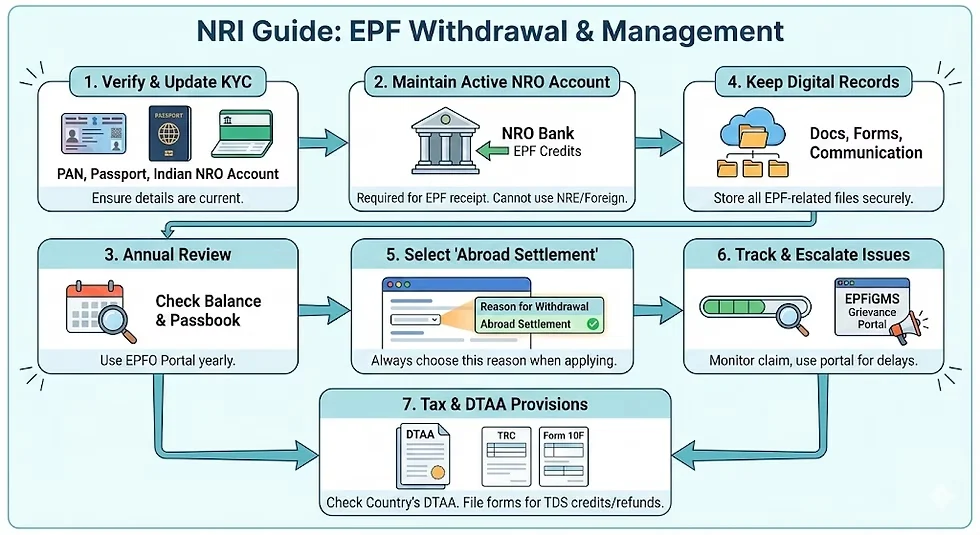

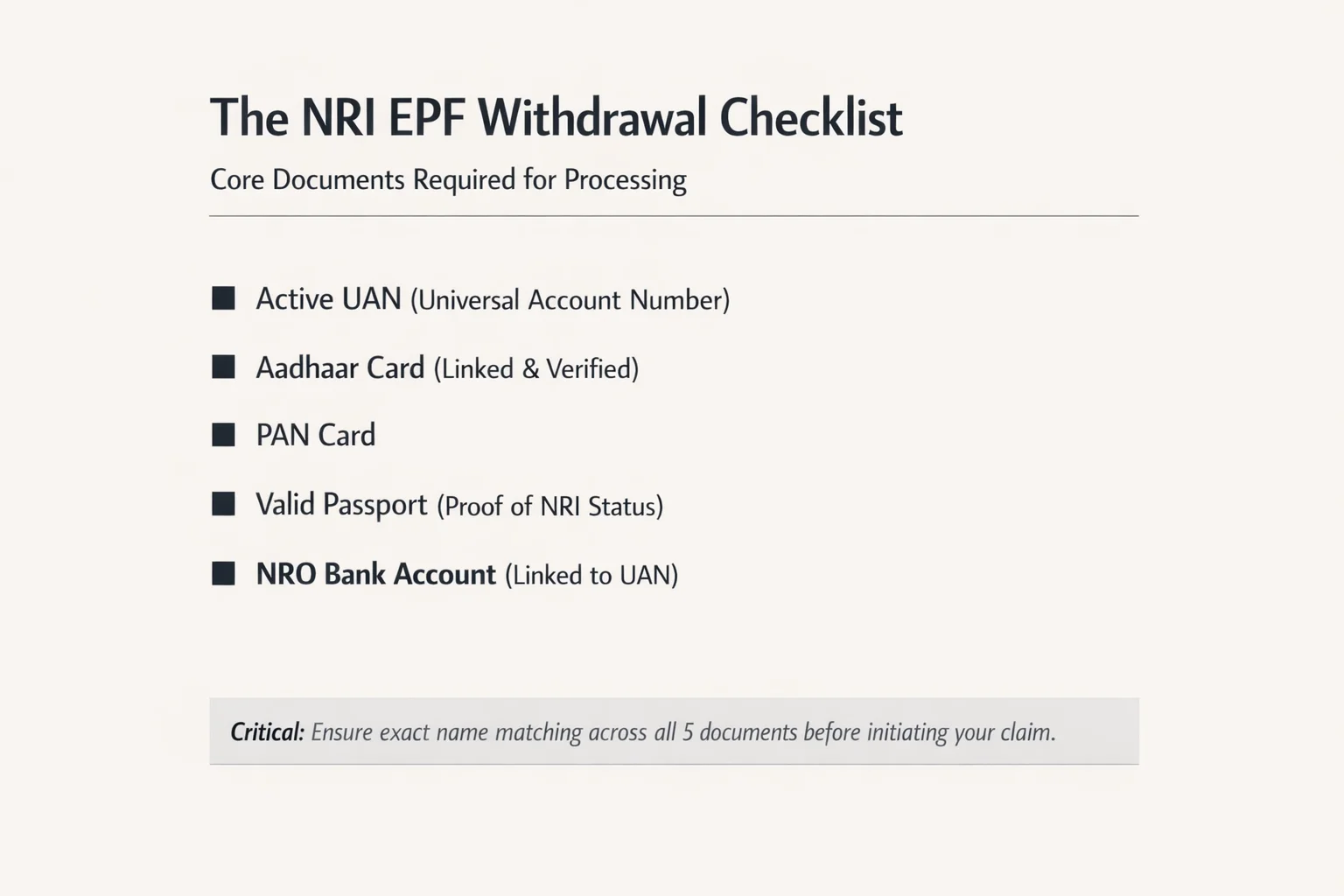

4. Documents Required for NRI EPF Withdrawal

Having the correct documents in place is critical - most EPF claim delays and rejections happen due to incomplete or mismatched documentation. For NRIs, this becomes even more sensitive because of cross-border identity and banking requirements.

,

Basic Documents

To initiate an EPF withdrawal, NRIs must have the following core documents in place:

- UAN (Universal Account Number)

- Aadhaar (linked and verified)

- PAN card

- Passport (proof of leaving India / NRI status)

- Bank account details (linked to UAN)

These documents must be consistent across all systems. Even minor differences—such as initials vs full name—can lead to rejection or delays.

Tip: Before applying, verify that your KYC is fully approved in the UAN portal. If any document is pending approval, your claim may not even be processed.

Embassy Attestation (When Required)

Embassy attestation is required in certain offline or exceptional scenarios, especially when verification cannot be completed digitally.

Typically required when:

- You are applying through the offline process from abroad

- Your employer is unavailable or unresponsive

- There is a signature mismatch or identity concern

In such cases, your documents (especially claim forms and identity proofs) may need to be attested by:

- Indian Embassy

- Notary public (in some jurisdictions, subject to EPFO acceptance)

What can go wrong:

- Submitting unattested forms when attestation is required

- Incorrect attestation format

Tip: Always confirm with the EPFO regional office or consultant before proceeding with attestation, as requirements can vary based on your case.

Bank Account Requirement (NRO Rule)

One of the most important—and commonly misunderstood—requirements for NRI EPF withdrawal is the bank account type.

Key Rule:

👉 EPF funds can only be credited to an Indian bank account, and for NRIs, this is typically an NRO (Non-Resident Ordinary) account.

Why NRO and Not NRE?

- EPFO processes are designed for domestic credit flows

- NRE accounts are meant for foreign income and repatriation, and are often not accepted for EPF settlement

- Attempting to use an NRE account frequently leads to claim rejection or failure to credit funds

What must match:

- Name on bank account = name in UAN

- IFSC code must be correct

- Account must be active and KYC-compliant

Common Issues:

- Claim approved, but money not credited → due to bank mismatch

- Rejection due to incorrect account type

Tip: Before applying, ensure your NRO account is:

- linked in UAN

- verified by employer

- active and capable of receiving funds

What Happens If Documents Don’t Match

Document mismatch is one of the biggest silent killers of EPF claims.

Common mismatch scenarios:

- Name variation between Aadhaar, PAN, and the bank

- Old surname vs updated surname

- Initials vs full name

- Date of birth mismatch

What happens:

- The claim may get rejected outright

- Or remain stuck in “under process”

- Or funds may not be credited even after approval

How to fix:

- Update details in the UAN portal

- Submit a correction request via the employer

- Use Joint Declaration (if required)

Key takeaway:

Even small inconsistencies can break the process. Align all documents before initiating your claim to avoid delays of several weeks.

5. Where Will Your EPF Money Be Credited?

EPF withdrawals are credited only to bank accounts linked with your UAN, and for NRIs, this follows strict rules.

Key Rules:

- Funds are credited only to Indian bank accounts

- The NRO account is mandatory in most cases

- NRE accounts are generally not supported for EPF settlement

How the credit works:

- Once your claim is approved, EPFO processes a direct bank transfer

- No international transfer is done by EPFO

- Funds must first land in your NRO account

Common delays and failures:

- Bank account not verified in UAN

- Name mismatch between UAN and the bank

- Incorrect IFSC or inactive account

- Using NRE instead of NRO

Important Insight: Even if your claim is marked as “settled,” the money may not be credited if your bank details are incorrect. This creates confusion and requires reprocessing.

Tip: Treat your bank setup as a critical step—not a formality. Most post-approval issues happen here.

6. Tax on EPF Withdrawal for NRIs

EPF withdrawal for NRIs is subject to specific tax rules, including TDS and DTAA provisions**.** Taxation is one of the most important—and most misunderstood—aspects of EPF withdrawal for NRIs. Incorrect handling can lead to unnecessary deductions of 20–30% or more.

| Scenario | TDS | What You Should Do |

|---|---|---|

| <5 years + PAN | 10% | Claim a refund if the excess is deducted |

| <5 years no PAN | 30% | Link PAN before withdrawal |

| >5 years | 0% (usually) | Verify eligibility |

| DTAA applicable | Reduced | Submit TRC + Form 10F |

TDS Rules for NRIs

EPF withdrawals for NRIs are subject to Tax Deducted at Source (TDS) depending on service duration and documentation.

Key rules:

- If service is less than 5 years → TDS applies

- If service exceeds 5 years → generally tax-free (with conditions)

TDS Rates:

- 10% TDS → if PAN is submitted

- 30% TDS → if PAN is not available

Additional considerations:

- TDS is deducted at source by EPFO

- Final tax liability may differ based on your country of residence

Common mistake:

Many NRIs do not link PAN, leading to 30% deduction, which could have been reduced.

When Is EPF Withdrawal Tax-Free?

EPF withdrawal can be tax-free under certain conditions:

Primary condition:

- Continuous service of 5 years or more

Also applicable if:

- Termination due to ill health

- Employer shutdown

- Other valid reasons recognised by EPFO

Important note for NRIs: Even if EPFO does not deduct TDS, you may still need to declare income in your country of residence depending on local tax laws.

DTAA Benefits Explained Simply

DTAA (Double Taxation Avoidance Agreement) ensures that you are not taxed twice—once in India and again in your country of residence.

How it helps:

- Reduces or eliminates double taxation

- Allows credit for tax paid in India

What you need:

- Tax Residency Certificate (TRC)

- Form 10F

- PAN

Example: If TDS is deducted in India, you may be able to claim credit in your resident country under DTAA provisions.

Key insight: DTAA doesn’t eliminate tax—it ensures fair taxation across countries.

Form 10F (Latest Update)

Form 10F has become increasingly important for NRIs claiming DTAA benefits.

What it is:

- A declaration is required when claiming DTAA benefits

- Submitted along with TRC

When required:

- When you want to avoid or reduce TDS

- When claiming a foreign tax credit

Common issue: Many NRIs are unaware of Form 10F and miss out on tax optimisation opportunities.

Form 15G / 15H for PF Withdrawal

This is one of the most misunderstood aspects.

Key rule: Form 15G/15H is generally not applicable to NRIs

Why:

- These forms are meant for resident individuals

- NRIs typically cannot use them to avoid TDS

Common mistake:

NRIs submit Form 15G expecting zero TDS—this often leads to rejection or no effect.

Takeaway: Do not rely on Form 15G as an NRI—focus on PAN, DTAA, and proper documentation instead.

What If TDS Is Deducted Incorrectly?

In many cases, TDS may be deducted incorrectly due to:

- PAN not linked

- Incorrect service record

- Lack of DTAA documentation

What you can do:

- File an income tax return in India

- Claim a refund for excess TDS

- Provide correct documentation

Important: TDS is not the final tax—it is an advance deduction. You can recover excess amounts.

How NRIs Can Claim Tax Refund on EPF

If excess tax has been deducted, NRIs can claim a refund through the Indian income tax system.

Steps:

- File Income Tax Return (ITR) in India

- Declare EPF withdrawal and TDS deducted

- Claim a refund for excess tax

Requirements:

- PAN

- TDS details (Form 26AS)

- Bank account for refund

Timeline:

- Refund is typically processed within a few months

Tip: Even if you are an NRI, filing ITR in India can help recover significant tax deductions.

Example Scenarios

Case 1: Service <5 years, PAN available → 10% TDS deducted

Case 2: Service <5 years, no PAN → 30% TDS deducted

Case 3: Service >5 years → Generally tax-free

Case 4: TDS deducted but DTAA applicable → Claim refund or tax credit

How to Reduce TDS on EPF Withdrawal (For NRIs)”

- Ensure PAN is linked

- Check DTAA eligibility

- Submit TRC + Form 10F

- File ITR to claim a refund

Final Takeaway: Tax is not just about compliance—it’s about optimisation.

If handled correctly, you can:

- reduce TDS

- avoid double taxation

- recover excess deductions

If handled incorrectly, you can lose a significant portion of your EPF unnecessarily.

7. How Long Does NRI EPF Withdrawal Take?

The processing time for NRI EPF withdrawal typically ranges between 7 to 20 working days after successful claim submission. However, this timeline assumes that all details—KYC, bank account, and employer exit—are correctly in place. The waiting period or PF withdrawal waiting period after leaving a job is typically 60 days.

What affects the timeline:

- Employer approval delays (exit not marked)

- KYC not fully verified

- Bank account issues (NRO mismatch or incorrect details)

- High claim volume at EPFO

Practical insight:

- Online claims with clean KYC are processed faster

- Offline claims may take longer due to manual verification

Key takeaway: Most delays are not due to EPFO processing itself, but due to errors or gaps in your application setup.

8. Why EPF Claims Get Rejected for NRIs

- Employer exit is not updated

- KYC mismatch

- Wrong bank account (NRE instead of NRO)

- Incorrect withdrawal reason

Even when the process seems straightforward, NRIs often face delays or rejections due to operational and documentation issues. Understanding these problems upfront can help you avoid weeks of back-and-forth.

Employer Approval Delays

One of the most common blockers is when the employer has not updated your date of exit in the EPFO system.

Why this matters:

- EPFO does not allow withdrawal unless employment is officially closed

- Your claim may remain pending indefinitely

Common scenarios:

- Employer is unresponsive

- The company has shut down

- Exit details were never updated

What you can do:

- Contact your employer to update your exit

- Use the EPFO grievance system if needed

- Switch to an offline process in extreme cases

Learn how to resolve EPF employer approval pending issues → https://www.kustodian.life/resources/epf-claim-stuck-employer-approval-guide

Claim Rejected by EPFO

Claims can be rejected due to small but critical errors.

Common reasons:

- Incorrect bank account (NRE instead of NRO)

- Name mismatch across documents

- Incomplete KYC

- Incorrect withdrawal reason selected

What happens next:

- You must correct the issue

- Reapply for withdrawal

Tip: Always check the rejection reason carefully—fixing the root cause is essential before reapplying.

Understand why claims fail and how to fix EPF claim rejection reasons → https://www.kustodian.life/resources/epf-troubleshooting-masterclass-real-solutions-for-common-pf-problems

KYC / Name Mismatch Issues

Mismatch in personal details is a silent but frequent cause of failure.

Common mismatches:

- Aadhaar vs PAN name difference

- Initials vs full name

- Date of birth inconsistency

Impact:

- Claim rejection

- Delay in approval

- Bank credit failure

Fix:

- Update details in the UAN portal

- Submit a correction via the employer

- Use the Joint Declaration if required

Step-by-step guide to fixing EPF KYC errors and corrections → https://www.kustodian.life/resources/epf-troubleshooting-masterclass-real-solutions-for-common-pf-problems#epf-kyc-update-aadhaar-linking-issues-how-to-fix-mismatches

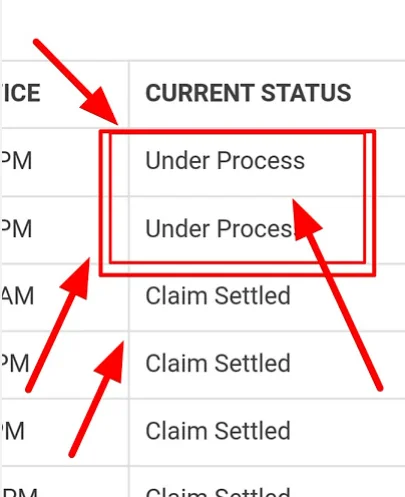

What “Under Process” Actually Means

Many NRIs see their claim stuck in “Under Process” and assume something is wrong.

What it actually means:

- The claim has been submitted and is being reviewed

- Verification is pending at the EPFO or the employer level

When it becomes a problem:

- Status remains unchanged for more than 15–20 days

- No movement due to backend or verification issues

What to do:

- Wait for the standard processing window

- If delayed, raise a grievance or follow up

Claim Settled, but Amount Not Received

This is one of the most confusing situations.

What it means:

- EPFO has approved the claim

- Payment has been processed

Why money is not received:

- Bank account mismatch

- Incorrect IFSC code

- Account inactive or closed

What to do:

- Verify bank details in UAN

- Contact the bank for incoming transaction issues

- Raise an EPFO grievance if needed

If your claim is settled but money is not credited, here’s how to resolve EPF claim settled but amount not received → https://www.kustodian.life/resources/pf-claim-settled-but-money-not-received-why-payments-fail-after-approval

Common Claim Rejections & Fixes

| Problem | Likely Cause | Fix |

|---|---|---|

| No OTP received | Indian mobile is not active | Use an offline process |

| Claim rejected | KYC mismatch | Update details in UAN |

| Money not credited | Wrong bank account | Use NRO account |

| Stuck “under process” | Employer/EPFO delay | Wait or raise a grievance |

Key takeaway:

Most EPF issues are not random—they are predictable and preventable if you understand where things usually break.

9. FAQs on NRI EPF Withdrawal

Q. Can NRIs Withdraw PF Online After Moving Abroad?

Yes, NRIs can withdraw their PF online after moving abroad for employment or permanent settlement. In such cases, EPFO typically allows immediate withdrawal without waiting for the 2-month unemployment period, as long as your exit from employment is properly recorded.

To complete the process successfully:

- Your date of exit must be updated by your employer

- Your KYC (Aadhaar, PAN, bank account) must be verified

- You must select the correct reason, such as “abroad settlement”, while applying

If these conditions are not met, the claim may be delayed or rejected, even if you are eligible.

Q. Is EPF withdrawal taxable for NRIs?

Yes, EPF withdrawal may be taxable depending on your service duration and whether PAN is linked. TDS may be deducted, but you can claim refunds if excess tax is paid.

Q. Can EPF be credited to an NRE account?

No, EPFO typically credits funds only to NRO accounts. Using an NRE account may result in rejection or failure to receive funds.

Q. What if I don’t have access to my Indian mobile number?

You may face issues with OTP verification. In such cases, you can:

- Update your mobile number

- Or use the offline withdrawal process

Q. Can I withdraw EPF without Aadhaar?

Yes, but only through the offline process. Online withdrawal requires Aadhaar linkage.

Q. What if my employer is not responding?

If your employer has not marked your exit, you can:

- Follow up directly

- Raise a grievance with EPFO

- Or explore offline submission

Q.How long does it take to receive EPF money?

Typically, 7–20 working days after submission. Delays may occur due to KYC or bank issues.

Q. Can I withdraw both PF and pension?

Yes. Use:

- Form 19 → PF balance

- Form 10C → pension component

Q. What happens if my claim is rejected?

You need to:

- Identify the rejection reason

- Correct the issue

- Reapply

Q. Can EPF Be Withdrawn Without Aadhaar or OTP?

Yes, but only through the offline process. Online EPF withdrawal requires Aadhaar linkage and OTP verification. If you do not have access to your registered mobile number, you can submit a physical claim form along with the required documents.

Q. Can NRIs withdraw the employer contribution in PF?

Yes, NRIs can withdraw both employee and employer contributions from EPF, along with the pension component (subject to eligibility). However, the correct forms (Form 19 and 10C) must be selected during the withdrawal process.

10. What Should You Do Next?

At this stage, your next step depends on your current situation:

✅ If you are eligible and ready

You can proceed with the online EPF withdrawal process—ensure your KYC, bank account, and employer exit details are correctly set up before applying.

⚠️ If your claim is stuck or rejected

Identify the exact issue—whether it’s KYC mismatch, employer delay, or bank error—and resolve it before reapplying. Most repeated failures happen because the root issue is not fixed.

❓ If you’re unsure or facing multiple issues

It’s better to get clarity before proceeding. EPF withdrawal for NRIs involves multiple dependencies, and a small mistake can lead to significant delays or tax losses.

Key Takeaways for NRI EPF Withdrawal

- You can withdraw EPF after 2 months or immediately if moving abroad

- Always use an NRO account

- Most issues happen due to KYC or employer delays

- Tax can be reduced with proper PAN and DTAA usage

Need Help with NRI PF Withdrawal?

Withdrawing EPF as an NRI can be more complex than it appears—especially when dealing with documentation, tax rules, and coordination with employers and EPFO.

With the right support, you can:

- Avoid rejection and delays

- Reduce unnecessary tax deductions

- Complete the process faster and with confidence

If you’re facing issues or want to ensure a smooth withdrawal, getting expert help can save both time and money.

![Why E-Khata Applications Get Rejected in Bangalore (And How to Fix Them) [2026]](/_next/image?url=https%3A%2F%2Fwebsite-assets-wix.s3.ap-south-1.amazonaws.com%2Fimages%2Fposts%2F3031ceb9f0274289aad5c5f140be716f.webp&w=828&q=75)