If you are facing a sudden job change, a career break, or a financial emergency, the question is simple: “Can I take my NPS money out now, or is it locked until I’m 60?”

The short answer is yes, you can exit. However, unlike a savings account or a bank FD, a premature exit from the National Pension System (NPS) is a permanent decision with specific "rules of the road."

In 2026, the landscape has shifted. Following the latest PFRDA amendments, the "small corpus" relief has been raised to ₹10 Lakh, and new structured withdrawal options have been introduced. This guide walks you through the 2026 regulations, the tax impact, and how to avoid the "80% pension trap" to ensure you make the right move for your current needs and your future security.

At a Glance: 2026 NPS Rules

- 100% Cash-out: Now allowed for total corpus up to ₹5 Lakh for early exits, and up to ₹8 Lakh for normal exits (Age 60+).

- Max Lump Sum: Non-government subscribers can now withdraw up to 80% as a lump sum (up from 60%) for corpus amounts above ₹12 Lakh.

- Partial Withdrawal: Frequency increased to 4 times in a lifetime (with a 4-year gap between requests).

- Upper Age Limit: You can now remain invested and defer your exit until 85 years old.

1. “I Need My NPS Money Before 60”: Is it Possible?

If you are reading this, chances are life has thrown you a curveball. Financial urgency doesn't always wait for retirement age. We see it every day, subscribers facing unexpected life shifts that make them look at their NPS balance as a lifeline:

- Sudden Job Loss: You need a bridge to your next role.

- Career Break or Startup: You are pivoting to a new business venture.

- Emigration: You are moving abroad and want to settle your Indian accounts.

- Medical or Family Emergency: You need immediate liquidity for high-cost treatments.

The question at the top of your mind is: “I’ve invested in NPS for years, can I take my money out now, or is it locked until I’m 60?”

The Honest Answer

Yes, you can exit NPS before 60. However, unlike a standard Savings Account, Fixed Deposit (FD), or even the EPF, the National Pension System (NPS) has very specific "Rules of the Road" for early exits.

In 2026, following the latest PFRDA (Exits and Withdrawals) Amendment Regulations, the rules have become more flexible, but they still carry strict guardrails. NPS is fundamentally designed to protect your future self, so the system makes it intentionally difficult to "cash out" 100% of your wealth prematurely.

The "Process" Reality

Most people panic when they see the 80% annuity requirement (where most of your money is locked into a monthly pension). But understanding the difference between a Permanent Premature Exit and a Partial Withdrawal is the key to getting the funds you need without destroying your retirement nest egg.

2. What “NPS Exit Before 60” Actually Means

Before diving into the math, it is crucial to understand that a "Premature Exit" is not just a withdrawal; it is a permanent termination of your retirement contract. Many subscribers confuse this with a loan or a temporary draw-down, but the implications are far more serious.

Premature Exit = Permanent Closure

When you choose to exit the National Pension System before the age of 60 (or before 5 years of investment), the following triggers occur:

- Account Termination: Your Tier-I account is closed permanently.

- PRAN Deactivation: You cannot re-open or re-enter the NPS using the same Permanent Retirement Account Number (PRAN).

- Mandatory Annuity: Unless your corpus is very small, the system forces "pension preservation," meaning you cannot take all your cash home.

Exit vs. Withdrawal: Know the Difference

It is vital to distinguish between these two terms to avoid a permanent financial mistake:

| Feature | Partial Withdrawal | Premature Exit (Before 60) |

| Account Status | Stays Active | Closed Permanently |

| Purpose | Temporary liquidity for specific needs. | Total exit from the pension system. |

| Pension Lock-in | None. | 80% of the corpus must go to Annuity. |

| Future Benefit | Compounding continues on balance. | All future compounding stops. |

3. Who Is Allowed to Exit NPS Before 60?

While the National Pension System (NPS) is designed for long-term retirement planning, an "Early Exit" is possible. However, the eligibility and process depend heavily on your sector.

Non-Government Subscribers (All Citizens & Corporate)

Private sector employees and self-employed individuals have the most flexibility, though it is not an unconditional "ATM" facility.

- Minimum Tenure: As of 2026, you must have completed at least 5 years from the date of your first contribution to initiate a premature exit.

- The "Lock-in" Reality: For most, there is no automatic right to 100% cash. Unless your corpus is small (see Section 4), the system forces a pension mindset.

- CRA Governance: All exits are processed via the Central Recordkeeping Agency (CRA) and must comply with the latest PFRDA Master Circulars.

Government Subscribers

For those in the public sector, exiting before age 60 is usually a "service-linked" event rather than a personal financial choice.

- Trigger Events: Early exit is permitted only upon Resignation, Removal, or Dismissal from service.

- The "20-Year" Nuance: In 2026, government employees who resign after 20 years of qualifying service may be treated under "Retirement" rules, allowing for a 60% lump-sum withdrawal instead of the strict 20% premature limit.

If a job change triggers your exit, don't leave your old EPF balance behind. It can be merged or withdrawn separately. Check our Complete 2026 Guide to EPF Withdrawal & Service Mergers to ensure you aren't missing out on your employer's contribution.

4. Confirmed Premature NPS Exit Rules (2026 Update)

This is the most critical update for 2026. The PFRDA has significantly raised the limits to allow subscribers with smaller balances to exit without being forced into tiny, impractical pensions.

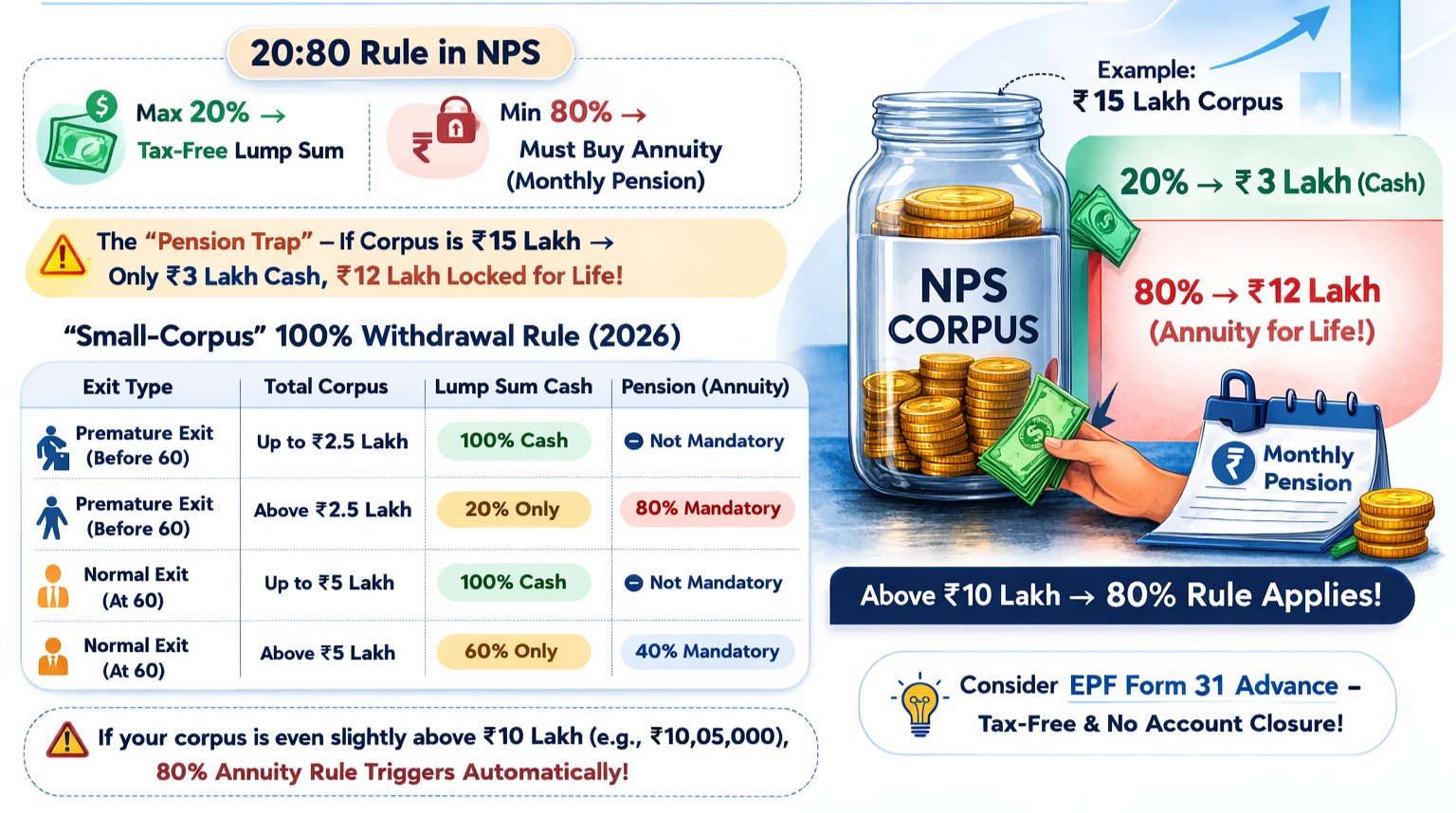

4.1 The 20:80 Rule in NPS

If your total corpus (contributions + market growth) exceeds the small-corpus threshold:

- Maximum 20%: Paid as a tax-free lump sum.

- Minimum 80%: Must be used to purchase an Annuity (Monthly Pension).

- The "Pension Trap": If you have ₹15 Lakh and exit early, you only get ₹3 Lakh in cash. The remaining ₹12 Lakh is locked away for life to pay you a monthly pension.

The 80% annuity requirement is the biggest hurdle for early exits. To understand how this compares to a normal retirement exit, see our Ultimate Guide to NPS Withdrawal for Retirees.

4.2 The "Small-Corpus" 100% Withdrawal Rule in NPS

In 2026, the threshold for a full cash-out has been increased to provide better liquidity.

| Exit Type | Total Corpus (Current Rule) | Lump Sum Cash Limit | Pension (Annuity) Requirement |

| Premature Exit (Before 60) | Up to ₹2.5 Lakh | 100% Cash | Not Mandatory |

| Premature Exit (Before 60) | Above ₹2.5 Lakh | 20% Only | 80% Mandatory |

| Normal Exit (At 60) | Up to ₹5 Lakh | 100% Cash | Not Mandatory |

| Normal Exit (At 60) | Above ₹5 Lakh | 60% Only | 40% Mandatory |

Official Source:https://www.pib.gov.in/PressReleasePage.aspx?PRID=2206763®=3&lang=1

Warning: If your corpus is even slightly above ₹10 Lakh (e.g., ₹10,05,000), the 80% annuity rule triggers automatically. You cannot "choose" to take more cash in this scenario.

If your corpus is above ₹10 Lakh and you hate the idea of an 80% lock-in, consider an EPF advance instead. It’s tax-free and doesn't close your account. Compare the two here: EPF Form 31: PF Advance Rules for 2026.

5. NPS Early Exit Limitations: 4 Things You Legally Cannot Do

Many NPS subscribers treat the system like a standard savings account or EPF. This is where most exit requests hit a wall. In 2026, the PFRDA made the system more flexible, but the core "pension preservation" philosophy remains.

If you are planning a premature exit, you must accept these four "No-Go" zones:

1. You cannot Take 100% Cash (If Corpus > ₹5 Lakh)

Unlike EPF, where you can often withdraw the full balance after two months of unemployment, NPS is strict.

- The Reality: If your total corpus (contributions + growth) is above ₹5 lakh, you are legally barred from taking more than 20% in cash. The remaining 80% must go into a monthly pension (annuity).

- Note: For a "Normal Exit" at age 60, this threshold is higher at ₹8 lakh.

2. You cannot "Skip" the Annuity

You might feel you can invest the money better yourself, but if you exit early with a corpus over ₹5 lakh, the annuity is mandatory. You cannot sign a waiver or pay a penalty to avoid it. The system is hard-coded to ensure you have a lifetime pension, whether you want one or not.

3. You Cannot Keep Your Tier-II Account Open

A common mistake is thinking you can close the "restrictive" Tier-I but keep the "flexible" Tier-II account active for trading or savings.

- The Rule: A Tier-II account is a "rider" to your Tier-I PRAN. When you initiate a permanent exit from Tier-I, your Tier-II account is automatically closed, and the balance is paid out to you.

4. You cannot re-open the Same PRAN

Once you exit prematurely, that Permanent Retirement Account Number (PRAN) is "retired" in the CRA system. You cannot change your mind six months later and "reactivate" it. You would have to start a brand new registration from scratch, losing your original account's history and tenure benefits.

6. NPS Early Exit vs. Partial Withdrawal: Which One Do You Need?

Before you take the irreversible step of closing your account, you must pause. In many financial emergencies, a Partial Withdrawal provides the liquidity you need without triggering the "80% Annuity Trap" that comes with a Premature Exit.

The Decision Matrix: Exit or Withdraw?

| Feature | Partial Withdrawal (Recommended) | Premature Exit (Last Resort) |

| Account Status | Stays Active and continues growing. | Closed permanently; PRAN deactivated. |

| Withdrawal Limit | Up to 25% of your own contributions. | 20% of the total corpus (if > ₹5 Lakh). |

| The "Pension Lock" | None. You keep 100% of the money. | 80% of your money is locked in a pension. |

| Tax Impact | 100% Tax-Free (Exempt-Exempt-Exempt). | A lump sum is tax-free; a pension is taxed yearly. |

| Frequency | Up to 4 times (New 2026 Limit). | Once-in-a-lifetime permanent decision. |

| Wait Period | Minimum 3 years of membership. | Minimum 5 years of membership. |

Why Partial Withdrawal is Usually Better

For most "life events" like a child's wedding, buying a first home, or a medical crisis, Partial Withdrawal is the superior choice.

- Zero Tax: Under Section 10(12B), partial withdrawals for specified purposes are not taxed at all.

- New 2026 Frequency: The PFRDA now allows you to withdraw up to 4 times in your lifetime, provided there is a 4-year gap between requests (though this gap is waived for medical emergencies).

- Compound Interest: Your account remains open, meaning the remaining 75% of your funds continue to earn market-linked returns.

When a Premature Exit Makes Sense

You should only choose a Premature Exit if:

- Emigration: You are permanently leaving India and have no intention of returning.

- Total Liquidation: Your total corpus is below ₹5 Lakh (allowing you to take 100% cash out and walk away).

- No Other Choice: You have already exhausted your 4 partial withdrawal limits and still have a dire need for funds.

7. Tax Impact of NPS Exit Before 60: The 2026 Guidelines

Many subscribers assume that if a withdrawal is "allowed," it is also "tax-free." This is a costly mistake. While NPS rules (PFRDA) determine how much you can take out, the Income Tax Act determines how much you keep.

1. Lump-Sum Taxation: The 60% Rule

- Under Section 10(12A) of the Income Tax Act, only up to 60% of your total corpus is exempt from tax upon exit.This is where the "shock" happens. The 80% of your money used to buy a pension is not taxed at the time of purchase, but:

- Let’s look at a subscriber with a ₹10 Lakh corpus exiting before age 60:

| Component | Amount | Tax Status |

| Lump Sum (20%) | ₹2,00,000 | Tax-Free (under 10(12A)) |

| Annuity (80%) | ₹8,00,000 | Invested Tax-Free |

| Monthly Pension | ~₹4,500/mo | Fully Taxable every month |

- While NPS's premature exit has specific tax rules, many users compare this with EPF for better tax efficiency. You can check the 2026 Guide to EPF Withdrawal to see which fund offers better immediate tax-free cash

8. How the NPS Early Exit is Processed (Step-by-Step)

Understanding the execution process reduces anxiety. In 2026, the PFRDA has streamlined the digital exit route, but the system's "security filters" are more sensitive than ever.

The Two Paths to Exit

- Online (Self-Authorisation): Best for eNPS subscribers. You log into the CRA portal (Protean/CAMS/KFintech) and use Aadhaar e-Sign to verify your request. No physical papers are required.

- Offline (POP Route): Necessary if your account is "Frozen," you lack Aadhaar, or you are a "Legacy" subscriber. You must visit your Point of Presence (POP) bank with physical forms.

The "Penny Drop" & Mismatch Filter

Before a single rupee is moved, the system performs a Mandatory Penny Drop Verification.

- What it is: The CRA sends ₹1 to your bank account to confirm it is active and belongs to you.

- The "Mismatch" Freeze: If the name on your PRAN (e.g., S. Kumar) does not match your Bank Account (e.g., Sandeep Kumar) or your Aadhaar, the request is not "rejected" it is frozen.

Typical Timelines for 2026

Once your exit is authorized by the Nodal Office or POP, the clock starts:

| Phase | Duration | What Happens? |

| Lump-Sum Credit | 2–4 Working Days | The 20% cash portion is wired to your verified bank account. |

| Annuity (Pension) Setup | 7–15 Working Days | Your data is shared with the Insurance Provider (ASP) to start your policy. |

| First Pension Paycheck | Next Monthly Cycle | Your first monthly pension starts hitting your account. |

9. Why Early Exit Requests Get Stuck And How to Fix Them

If your NPS exit status has been "Pending" or "Frozen" for more than 10 days, it is rarely a rejection. In 2026, the CRA (Central Recordkeeping Agency) has automated most checks, meaning any technical mismatch will put an immediate "Safety Lock" on your funds.

Here are the three most common reasons for a stuck exit and the direct fixes:

1. Failure (The Name Mismatch)

Before releasing funds, the system sends ₹1 to your bank. If your bank account name is "Sandeep K." but your PRAN record is "Sandeep Kumar," the Penny Drop will fail.

- The Fix: You must first update your bank details in the NPS portal to match your PRAN exactly. A successful Penny Drop is now a mandatory prerequisite for any exit in 2026.

2. FATCA Non-Compliance

The Foreign Account Tax Compliance Act (FATCA) is a mandatory self-declaration. If you haven't confirmed your tax residency (even if you've only ever lived in India), the "Exit" button may be greyed out, or the request will stay "In-Progress" indefinitely.

- The Fix: Log in to the Protean (NSDL) or CAMS portal, navigate to "Update Details," and complete the FATCA Self-Certification online. It takes 2 minutes and unblocks your account instantly.

3. Sector Mismatch (The ISS Issue)

Did you move from a Government job to a Private firm (or vice versa) but never updated your PRAN? This is called an Inter-Sector Shifting (ISS) mismatch. The system sees you as a "Government Employee", but you are applying as a "Private Citizen."

- The Fix: You must submit an ISS Form to your current Nodal Office or POP to "shift" your PRAN to the correct sector before initiating the exit.

Most "stuck" NPS requests are due to simple data errors. If your name or DOB doesn't match your records, the process will fail. Use our Joint Declaration Form Guide to learn how to fix profile errors across all your retirement accounts.

10. When You Can Get an Expert's Help

You should consider help if:

- Exit shows “Approved,” but no money is credited.

- An annuity is not generated.

- You switched between government and private jobs.

- NRI repatriation is involved

- Early exit causes large tax exposure.

Is Your Withdrawal Currently Frozen? Don't keep clicking "Resubmit" and risking a permanent block. Let our experts run a Free NPS Diagnostic Scan to identify the exact backend mismatch holding up your funds.

Useful Links & Official Resources

If you want to explore the National Pension System (NPS) rules in more detail or verify the latest regulations, the following official portals and guides can help.

Official NPS & Government Resources

- Pension Fund Regulatory and Development Authority (PFRDA) Official Websitehttps://www.pfrda.org.inThe primary regulator of the National Pension System. You can find official circulars, amendments, and policy updates here.

- National Pension System Trusthttps://www.npstrust.org.inProvides investor protection, operational transparency, and official information about NPS funds and trustees.

- National Securities Depository Limited (Protean CRA – NPS Portal)https://cra-nsdl.comThe main portal where subscribers can log in, check PRAN details, request withdrawals, or initiate an exit.

- Central Recordkeeping Agency (CAMS CRA Portal)https://npscra.nsdl.co.inAlternative CRA platform for managing NPS accounts, withdrawals, and updates.

- Press Information Bureau Government Release on NPS Amendmentshttps://www.pib.gov.in/PressReleasePage.aspx?PRID=2206763®=3&lang=1Official government update explaining recent NPS rule changes and withdrawal regulations.

Key NPS Services

- NPS Login / PRAN Account Accesshttps://cra-nsdl.com/CRA/

- Track NPS Withdrawal or Exit Request https://cra-nsdl.com/CRA/withdrawal

- Update FATCA / Personal Details in NPShttps://cra-nsdl.com/CRA/

FAQs

1. Can I exit NPS before the age of 60?

Yes, NPS allows exit before 60, but it is treated as a premature exit, not a normal withdrawal. This means your Tier-I account is closed permanently, and stricter rules apply compared to exiting at 60.

2. Is early exit allowed for all NPS subscribers?

Yes, but with different flexibility.

- All Citizen / Corporate subscribers → Early exit allowed under NPS rules.

- Government subscribers → Early exit allowed only in specific service conditions (resignation, removal, dismissal)

Government subscribers generally face more restrictions than private subscribers.

3. Does resigning from my job allow full withdrawal of NPS?

No. Resignation or job loss does not automatically allow full withdrawal.

Your withdrawal depends on:

- Your total NPS corpus

- Your subscriber category

- Applicable NPS exit rules at the time of request

If your corpus is above ₹5 lakh, the 20:80 rule still applies, even after resignation.

4. What happens to my NPS money if I exit before 60?

Your NPS corpus is split as follows:

- Up to 20% → Paid to you as a lump sum.

- Minimum 80% → Used to purchase an annuity, which pays a monthly pension

You do not lose money, but most of it becomes locked into future pension income, not immediate cash.

5. Can I withdraw 100% of my NPS before 60?

Only in one specific case.

If your total NPS corpus is ₹5 lakh or less at the time of exit:

- You can withdraw 100% as a lump sum.

- No annuity is required.

If your corpus exceeds ₹5 lakh even slightly, mandatory annuity applies.

6. Is partial withdrawal better than premature exit?

In most cases, yes.

Partial withdrawal:

- Keeps your NPS account active

- Allows limited withdrawal without pension lock-in

- Causes less long-term financial damage

Premature exit should be considered only when partial withdrawal is not sufficient or not allowed.

7. Is the lump-sum amount taxable if I exit early?

Generally:

- The permitted lump-sum portion is tax-exempt under current tax laws.

- Any withdrawal beyond permitted limits is taxed at your income-tax slab

Tax treatment depends on Income-Tax Act provisions, not just NPS rules.

8. Is the pension received from an annuity taxable?

Yes. Fully taxable.

- A monthly pension is treated as regular income.

- Taxed every year in the year of receipt

- No special tax exemption for early-exit pension

This is often the most underestimated cost of early exit.

9. Why does the pension amount look very low after early exit?

This is common and structural.

Reasons include:

- Early exit stops long-term compounding.

- A smaller corpus leads to a smaller pension.

- Annuity rates are market-linked, not high-return products

The pension feels low because NPS is designed for long-term retirement, not short-term exits.

10. What does it mean when my NPS exit request is “stuck”?

A “stuck” exit usually means the request is frozen, not rejected.

Common reasons:

- PRAN frozen due to missed minimum contribution

- FATCA compliance pending (common for NRIs)

- Bank / Aadhaar / PRAN name mismatch

- Sector history error (government ↔ private switch)

Once corrected, the exit usually proceeds.

Conclusion:

Deciding to exit NPS early is rarely easy; often, it is a choice forced by life’s unexpected financial pressures. It is completely understandable to feel like you need to access every available resource when things get tough. However, because NPS is designed to be your safety net for old age, the system penalises a premature exit by locking 80% of your hard-earned money into a small monthly pension that you cannot touch today.

Before you take this permanent step, please pause and look for other lifelines. Options like a partial withdrawal or accessing your EPF (if you are salaried) might provide the immediate relief you need without sacrificing your financial freedom. If you absolutely must exit, do so with full awareness, but try to treat this as your last resort; your future self will thank you for keeping this door open.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.

![Why E-Khata Applications Get Rejected in Bangalore (And How to Fix Them) [2026]](/_next/image?url=https%3A%2F%2Fwebsite-assets-wix.s3.ap-south-1.amazonaws.com%2Fimages%2Fposts%2F3031ceb9f0274289aad5c5f140be716f.webp&w=828&q=75)