Contents

Introduction

- Why NPS Withdrawal Rules Feel Confusing

- Key Terms You Must Understand

- What NPS Withdrawal Rules Actually Control

- Normal Exit Rules (2026 Update)

- The "Smart" Exit: Systematic Lump Sum Withdrawal (SLW)

- Premature Exit Rules (Before Retirement)

- The "Unfortunate" Exit: Death Claim Rules

- Partial Withdrawal Rules (While Staying Invested)

- Tax on NPS Withdrawal (The Real Trap)

- Decoding the Annuity Options (The "Pension" Part)

- Tier I vs. Tier II: The "Hidden" Rules

- Common Rule Misunderstandings

- How Rules Translate Into Action

- FAQs

Introduction:

The "80% Rule" Changed Everything (But Watch Out for the Tax Trap)

If you are planning your retirement in 2026, you are looking at a completely different landscape than just a year ago.

For years, the biggest complaint about the National Pension System (NPS) was the "forced pension." You were mandated to buy an annuity with 40% of your hard-earned money, leaving you with only 60% cash in hand.

The Good News: In a massive update for 2026, the PFRDA has flipped the script for private sector subscribers. You can now withdraw up to 80% of your corpus as a lump sum, leaving only 20% for the mandatory annuity.

The Bad News (The "Trap"): While the pension regulator says you can take 80% home, the taxman hasn't necessarily agreed to let you keep it all tax-free.

This guide decodes the new 2026 rules, the "hidden" tax implications, and the smart strategies (like SLW) you need to exit the NPS without losing your peace of mind.

1. Why NPS Withdrawal Rules Feel Confusing

If you’ve tried reading the official circulars, you probably felt like you were decoding an ancient script. The confusion usually stems from three sources:

- The “Locked Money” Myth: Many believe NPS money is untouchable until age 60. In reality, it’s not locked; it’s structured to ensure you don't outlive your savings (longevity risk).

- The Two Masters: Rules are set by PFRDA (the regulator), but taxes are decided by the Finance Ministry. Sometimes, they don’t talk to each other, creating situations where you can withdraw money but shouldn't due to tax hits.

- The Shift: NPS has evolved from a rigid "Pension-Only" product to a flexible "wealth-management" tool. The 2026 rules reflect this shift, moving from a strict annuity focus to giving you more control over your cash.

2. Key Terms You Must Understand

Before we dive into the rules, let's kill the jargon:

- Exit vs. Withdrawal: "Exit" means closing your account permanently (usually at retirement). "Withdrawal" usually refers to taking money out while keeping the account active (partial withdrawal).

- Lump Sum: The cash you get in hand immediately.

- Annuity: The portion you must give to an insurance company, which they pay back to you as a monthly pension for life.

- SUR (Systematic Unit Redemption) / SLW: The modern alternative to a one-time lump sum. Instead of taking all your cash at once, you keep it invested and withdraw a fixed amount periodically (like a reverse SIP).

3. What NPS Withdrawal Rules Actually Control

Think of the rules as a gatekeeper managing three pillars:

- Lump-sum Limits: How much hard cash you can take home.

- Pension Mandate: The minimum percentage that must be converted into a monthly pension (annuity).

- Slab-based Flexibility: New rules that change your options based on how much money you have accumulated.

4. Normal Exit Rules (2026 Update)

This applies when you retire at age 60 or reach superannuation.

4.1 Eligibility

- Age: You must generally be at least 60 years old.

- Tenure: You must have been in the scheme for at least 10 years. (If less than 10 years, it is treated as a Premature Exit, see Section 6).

4.2 Corpus-Based Slabs (The "How Much" Guide)

PFRDA has raised the limits in 2026 to help smaller investors avoid being forced into tiny, meaningless pensions.

| Your Total Corpus | Withdrawal Rule |

| ≤ ₹8 Lakh | 100% Lump Sum allowed. No annuity required. You can take the whole amount tax-free and close the account. (Limit raised from ₹5L). |

| ₹8 Lakh – ₹12 Lakh | Hybrid Zone. You can withdraw up to ₹6 Lakh as a lump sum. The remaining balance must go into an Annuity or SUR (Systematic Withdrawal). |

| > ₹12 Lakh | Standard Rule. This depends on your sector (see 4.3 below). |

4.3 Government vs. Private Subscribers (The Big Split)

Here is where the confusion peaks. The rules are not the same for everyone.

- Private Sector (All Citizens & Corporate Models):

- Government Employees (Central & State):

4.4 Deferment Rules

Not ready to retire? You have options:

- Defer Lump Sum: You can delay taking your lump sum until age 75.

- Stay Invested: You can now keep contributing to NPS up to age 85 (extended from 70).

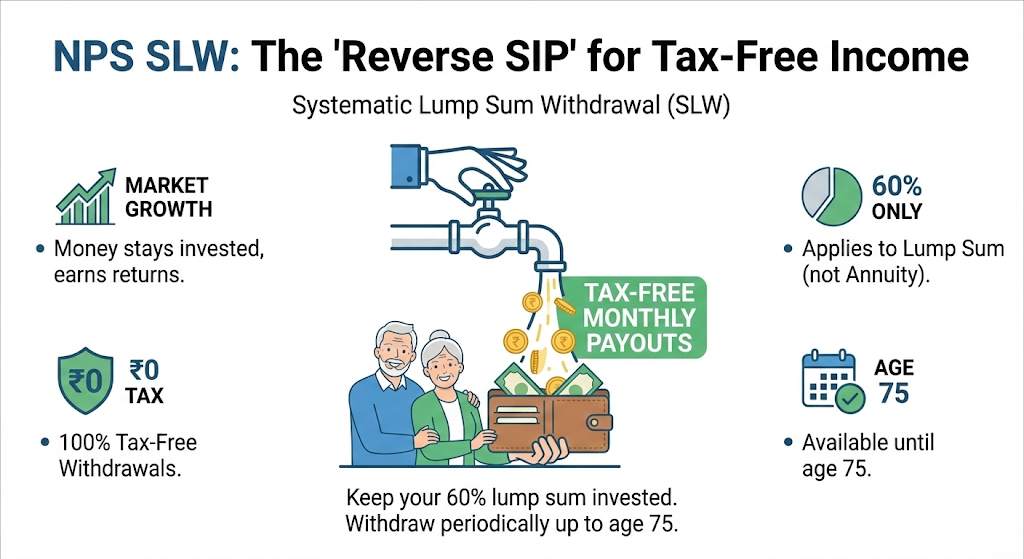

5. The "Smart" Exit: Systematic Lump Sum Withdrawal (SLW)

Gone are the days when you had to take your 60% (or 80%) lump sum all at once. PFRDA now allows Systematic Lump Sum Withdrawal (SLW). Think of this as a "Reverse SIP" for your retirement cash.

- How it works: Instead of taking your eligible lump sum instantly at retirement, you keep it in the NPS. You then instruct the system to pay you, say, ₹50,000 every month.

- Why use it?

- The Rules:

Alternative for EPS: SLW is great for your NPS lump sum. But what about your EPS pension? If you are eligible for a monthly pension under EPS, learn how to claim it with EPF Form 10D: The 2026 Guide to Claiming Your Monthly Pension.

6. Premature Exit Rules (Before Retirement)

If you want to close your account before age 60 (and you've completed 5 years in NPS):

- The Penalty: The rules are harsh to discourage raiding your nest egg. You can only withdraw 20% as a lump sum. You must use 80% of your money to buy an annuity.

- Small Corpus Relief: If your total corpus is ≤ ₹2.5 Lakh, you can withdraw 100% of it without buying an annuity.Need cash before retirement? If you need funds for emergencies like marriage, medical treatment, or home buying, you can also explore taking an advance from your EPF. Check the rules here: EPF Form 31: PF Advance / Loan Rules, Limits & Online Apply.

7. The "Unfortunate" Exit: Death Claim Rules

What happens to the money if the subscriber passes away? The rules depend heavily on your sector.

7.1 Private Sector (All Citizens & Corporations)

- 100% Refund: The entire corpus (Lump sum + Annuity portion) is paid to the nominee/legal heir.

- No Annuity Mandate: The nominee is not forced to buy a pension. They can take the full cash.

- Tax Status: This withdrawal is fully tax-exempt for the nominee.

7.2 Government Sector

- The Spouse Protection Rule: The rules are stricter to protect the spouse.

- Mandatory Annuity: 80% of the corpus must be used to buy a default annuity (pension) for the spouse. The nominee gets only 20% cash.

- Exception: If the total corpus is ≤ ₹5 Lakh, the nominee can withdraw 100% as cash.

Crucial Resource: Dealing with financial matters after a death is difficult. Beyond NPS, you may need to locate other assets. Our guide on How to Find a Deceased Person’s Bank Accounts, Property & Unclaimed Assets in India (2026) can be an invaluable resource during such times.

8. Partial Withdrawal Rules (While Staying Invested)

Need money for an emergency but want to keep the account open?

- Eligibility: You must be a subscriber for at least 3 years.

- Limit: You can withdraw up to 25% of your OWN contributions (not the total corpus, and not the employer’s match).

- Frequency: Allowed up to 4 times during the entire tenure (changed from 3 times).

- Reasons: Strictly defined Higher education, marriage or children, purchase/construction of a house, or treatment of specified critical illnesses.

9. Tax on NPS Withdrawal (The Real Trap)

Warning: This is the most critical section.

PFRDA rules allow Private sector employees to withdraw 80% of their corpus. However, the Income Tax Act currently only exempts 60%.

- The Gap:

- How SUR Helps: Instead of taking that extra taxable 20% as a lump sum, you can use Systematic Unit Redemption (SUR) to withdraw it slowly over the years, potentially lowering the tax impact if your income drops after retirement.

Note: Always check the latest Finance Act, as this tax mismatch is a frequent subject of budget petitions.

Master Retirement Taxation: To fully understand the tax landscape for all your retirement funds in 2026, including VPF and TDS on withdrawals, read our comprehensive guide: EPF and PF Taxation India 2025 - Complete Guide on VPF, Withdrawal TDS, Exemptions & Form 15G.

10. Decoding the Annuity Options (The "Pension" Part)

When you are forced to buy an annuity with your remaining corpus, you will see confusing options. Here is the cheat sheet:

| Annuity Typeyour | What it Means | Who is it for? |

| Annuity for Life | You get the highest monthly pension, but when you die, the money vanishes. The insurance company keeps the corpus. | Singles with no dependents who want maximum monthly cash. |

| Joint Life Annuity | You get a pension. If you die, your spouse gets the pension for life. | Couples who want to secure the surviving partner. |

| ROP (Return of Purchase Price) | You get a lower monthly pension, but when you (and spouse) die, the original money is returned to your children/nominee. | Most Popular. For those who want to leave a legacy (inheritance) for their kids. |

11. Tier I vs. Tier II: The "Hidden" Rules

Many users mistakenly apply Tier I rules to Tier II.

- Tier I (Pension Account): Strict lock-in until age 60. Tax benefits on entry (80C/80CCD).

- Tier II (Investment Account):

12. 3 Common Rule Misunderstandings

- “I’m allowed 80%, so why did I get taxed?”

- “Why can’t I withdraw the employer part in a partial withdrawal?”

- “Why do government & private rules differ?”

Fixing Records is Key: Just like with NPS, errors in your personal details can cause major issues with EPF withdrawals. If you need to correct your name, DOB, or other details, here is the definitive guide: EPF Joint Declaration Form: Name, DOB & Detail Correction Guide.

13. How Rules Translate Into Action

Knowing the rules is step one. Doing it is step two.

- Check your Corpus: Log in to your CRA (NSDL/Protean or KFintech) to see which slab you fall into.

- Select Exit Type: Choose "Superannuation" (if 60+) or "Premature Exit".

- Choose Annuity: If you are in the >₹8L slab, you will be forced to select an Annuity Service Provider (ASP) for the pension portion.

How Kustodian Can Help

- PF Eligibility Guidance: Understand how much of your PF balance is actually withdrawable based on your employment status and service duration.

- Claim Preparation Support: Get help choosing the correct withdrawal category (advance vs. final settlement) before filing a claim.

- KYC & Record Checks: Ensure your Aadhaar, PAN, bank details, and employment records are correctly updated to avoid rejections.

- Error Resolution: Assistance with fixing common EPFO issues such as incorrect Date of Exit (DOE), service gaps, or multiple PF accounts.

- Withdrawal Planning: Understand tax implications and plan withdrawals in a way that minimizes unnecessary deductions.

Useful Links & Official Resources

To help you better understand the National Pension System and related retirement processes, here are some important resources and guides referenced in this article.

Official Government Sources

- PFRDA (Pension Fund Regulatory and Development Authority)Official NPS regulator responsible for policy updates and withdrawal rules.https://www.pfrda.org.in

- National Pension System (NPS) Official Portal Central portal for account access, withdrawals, and subscriber services.https://www.npscra.nsdl.co.in

- Protean CRA (NSDL) – NPS Account Services Manage your NPS account, exit request, and withdrawal forms.https://cra-nsdl.com

- KFintech CRA – NPS Services Alternative CRA platform for NPS account management.https://nps.kfintech.com

- Income Tax Department of India Official tax rules governing NPS withdrawal taxation.https://www.incometax.gov.in

- eNPS Portal – Open or Manage an NPS Account Onlinehttps://enps.nsdl.com

Important Documents & Circulars

If you want to read the actual regulations behind NPS withdrawals, refer to:

- PFRDA Exit & Withdrawal Regulations

- Latest NPS Withdrawal Circulars (2025–2026 updates)

- Income Tax Act Section 80CCD, 10(12A) related to NPS taxation

These are available on the PFRDA circulars section of the official website.

14. FAQs

Is an annuity compulsory for everyone?

No. If your corpus is ₹8 Lakh or less, you can skip the annuity and take 100% cash.

Can rules change after I invest?

Yes. NPS rules are "retrospective" regarding withdrawals the rules active on the day you exit apply to you, not the rules from when you joined.

Are NPS withdrawals ever fully tax-free?

Yes, if you stick to the 60% lump sum limit. If you withdraw more (like the new 80% option), the amount above 60% is taxable.

Does the corpus slab apply at the exit date or the contribution date?

It applies to the accumulated corpus value on the Date of Exit. Market movements right before you exit can push you into a different slab.

What is the "Penny Drop" verification?

Before processing your withdrawal, the CRA (Protean/KFintech) will deposit a small amount (e.g., ₹1) into your bank account to verify it is active. If this fails (due to name mismatch or dormant account), your withdrawal will get stuck. Ensure your bank KYC is perfect before hitting "Withdraw".

If I use SLW (Systematic Withdrawal), can I still contribute to NPS?

No. Once you activate SLW on your Tier I account, you are in "payout mode." You cannot add fresh contributions to Tier I, though you can still use Tier II.

Can I withdraw 80% of my NPS corpus tax-free in 2026?

No. While PFRDA allows an 80% withdrawal for private subscribers, the Income Tax Act currently only exempts 60%. The remaining 20% is taxable as per your income slab.

What is the limit for 100% NPS withdrawal without annuity?

As per the 2026 update, if your total corpus is ₹8 Lakh or less, you can withdraw the entire amount as a lump sum. You are not required to buy an annuity.

Is the monthly payout from NPS Systematic Lump Sum Withdrawal (SLW) taxable?

No, it is tax-free. Since SLW withdraws from your tax-exempt lump sum component (the 60% portion), the monthly payouts you receive are completely tax-free, unlike taxable FD interest or annuity pension.

How are NPS withdrawal rules different for Govt vs. Private employees?

Private sector employees can withdraw up to 80% lump sum (20% annuity), whereas Government employees generally must follow the 60% lump sum (40% annuity) rule, unless their corpus is small.

What is the penalty for closing NPS before age 60 (Premature Exit)?

If you exit before age 60, you can only withdraw 20% of your savings as cash. You are mandatorily required to use 80% of the corpus to buy a life pension (annuity), unless your total balance is under ₹2.5 Lakh.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.