In 2026, the National Pension System (NPS) is no longer a "one-size-fits-all" retirement plan. Following the massive PFRDA overhaul, the system has shifted from rigid mandates to subscriber-led flexibility.

The most innovative addition to this new landscape is the Systematic Lump Sum Withdrawal (SLW) facility. SLW is designed for the retiree who wants the best of both worlds: the market-linked growth of a lump sum and the disciplined cash flow of a monthly salary. Instead of emptying your retirement bucket on Day 1, SLW lets you install a "tap," giving you complete control over how your money flows while keeping the rest invested and tax-efficient.

This guide explains how you can use SLW in 2026 to turn your retirement corpus into a smart, steady, and customizable income stream that lasts as long as you need.

1. “I Don’t Want All My NPS Money at Once”

Imagine the day you retire. You log into your NPS account and see a balance of ₹50 Lakh.

For many, this isn't a moment of joy; it’s a moment of panic.

- "What if I spend it too fast?"

- "What if I invest it poorly and lose it?"

- "What if I get hit with a huge tax bill?"

The Reassurance:

You are not alone. Managing a massive pile of cash is stressful. That is why the Systematic Lump Sum Withdrawal (SLW) facility exists. It is designed for people who want the control of a lump sum but the discipline of a monthly salary. It turns a "cash shock" into a steady stream.

2. What Is SLW in NPS?

In simple terms, SLW allows you to withdraw your eligible lump-sum money in phases rather than taking it all on Day 1.

Think of it like a Systematic Withdrawal Plan (SWP) in Mutual Funds:

- Instead of emptying your bucket, you install a tap.

- You decide how much flows out (Monthly, Quarterly, or Annually).

- The remaining water (money) stays in the bucket and continues to grow.

In 2026, for Non-Government subscribers, this "Lump Sum" is a massive 80% of your total corpus.

- Instead of taking ₹40 Lakh from a ₹50 Lakh corpus at once, you can stagger it.

- The remaining 20% must still go toward a mandatory annuity (pension).

- Your money stays in your PRAN and continues to earn market returns until the day it is paid out to you.

Crucial Distinction:

SLW applies ONLY to the "Lump Sum Component" (typically, 60% of your corpus that you can keep).It has nothing to do with the "Annuity Component" (the 40% that must go to an Insurance Company).

Read about [NPS Withdrawal Rules 2026: The Ultimate Guide]

3. Checklist: When Is SLW Actually Available?

SLW is a feature, not a default setting. You can choose it only if you meet specific criteria.

You are eligible for SLW in if:

- Normal Exit: You have reached age 60 OR completed 15 years of subscription.

- Tier-I & Tier-II: SLW is available for both. (Note: Tier-II allows SLW at any age).

- Extended Timeline: You can now run your SLW schedule all the way until age 85 (up from 75).

- Death Claims: Nominees can now also opt for SLW instead of a one-time lump-sum payout.

SLW is NOT available for:

- The Annuity Portion: That 40% must buy a pension plan.

- Premature Exit: If you exit before 60, you typically cannot use SLW.

- Partial Withdrawals: It is for the final settlement, not emergency dips.

4. How SLW Actually Works (Step-by-Step Logic)

Here is the workflow of a Systematic Lump Sum Withdrawal:

- Initiate Exit: You request to exit NPS at age 60.

- Segregate Funds: The system splits your money.

- Choose SLW: Instead of clicking "Withdraw 60% Now," you select "Phased Withdrawal".

- Set Frequency: You choose to receive the money Monthly, Quarterly, or annually.

- Set Timeline: You decide how long this lasts (e.g., till age 75).

- Growth Continues: The money awaiting withdrawal remains invested in your chosen NPS funds (Equity/Debt) and continues to earn market returns.

5. Comparison: SLW vs. One-Time Lump Sum

Which strategy fits your retirement personality?

| Factor | SLW (Systematic Withdrawal) | One-Time Lump Sum |

| Cash Flow | Gradual (Like a Salary) | Immediate (All at once) |

| Spending Discipline | High (Prevents overspending) | Low (Risk of splurging) |

| Market Exposure | Continues (Unwithdrawn money grows) | Stops (You exit the market) |

| Tax Impact | Smoothed over years | One-time event |

| Flexibility | Moderate (Can be changed later) | High (Money is in your hand) |

Key Takeaway:

SLW suits people who want income-like discipline without locking their capital into a rigid pension plan forever.

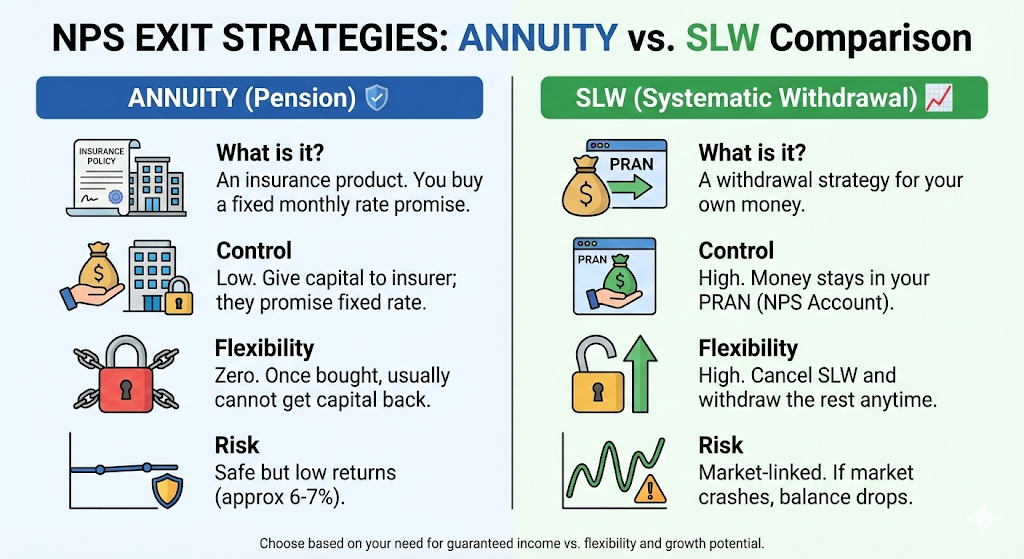

6. Confusion Alert: SLW is NOT an Annuity

This is the most common misunderstanding. Let's clear it up.

Annuity (Pension)

- What is it? An insurance product.

- Control: You give your capital to an insurer; they promise a fixed monthly rate.

- Flexibility: Zero. Once bought, you usually cannot get your capital back.

- Risk: Safe but low returns (approx 6-7%).

SLW (Systematic Withdrawal)

- What is it? A withdrawal strategy for your money.

- Control: The money stays in your PRAN (NPS Account).

- Flexibility: High. You can cancel SLW and withdraw the rest whenever you want.

- Risk: Market-linked. If the market crashes, your balance drops.

Bottom Line: SLW is NOT a pension replacement. It is a smarter way to handle your cash component.

7. The Tax Angle: Does SLW Save You Money?

This is a "proceed with caution" area in 2026:

- The 60% Rule: Under Section 10(12A), only 60% of the corpus is explicitly tax-exempt.

- The 20% Gap: Since PFRDA now allows you to withdraw 80%, the "extra 20%" taken via SLW may be taxed at your slab rate unless specifically exempt by the latest Finance Act.

- Growth: The returns earned on the balance during the SLW period are technically market gains; currently, there is no separate tax on these within the NPS umbrella, making it more efficient than a bank FD.

Example:

If you take ₹20 Lakh at once, it sits in your Savings Account earning interest (which is fully taxable). If you leave it in NPS via SLW, it potentially earns higher market returns, and you only deal with the cash flow you actually need.

8. Risks & Limitations (The Balanced View)

SLW is powerful, but it isn't magic.

- Market Risk: Your unwithdrawn balance is still in the market. If the stock market crashes the year after you retire, your remaining balance will shrink.

- Longevity Risk: Unlike an annuity, which pays for life, SLW stops when the money runs out (usually by age 75). You could outlive your SLW.

- Requires Monitoring: You cannot just "set it and forget it." You need to track your NAV and balance.

9. Decision Guide: How to Choose What’s Right for You

Ask yourself these three questions:

- "Do I trust myself with ₹50 Lakh cash?"

- "Do I need a guaranteed income for life?"

- "Do I want to stay invested in the market?"

Official Sources & References

1. Pension Fund Regulatory and Development Authority (PFRDA)

- PFRDA Circular – Facility of Systematic Lump Sum Withdrawal (SLW) for NPS Subscribers

- PFRDA Regulatory Circulars – Active Communications

- PFRDA – National Pension System (NPS) for All Citizen Model

2. NPS Trust – Subscriber Information

3. Government-Recognized Regulatory Framework

- PFRDA (Exits and Withdrawals under the National Pension System) Regulations, 2015 – Official PDF

- PFRDA (Exits and Withdrawals under the National Pension System) Amendment Regulations, 2025

- Government of India (PIB) Note on Tax Treatment of NPS Withdrawals

4. Official Coverage of 2025–2026 NPS Rule Changes

- https://economictimes.indiatimes.com/wealth/save/nps-changes-10-new-rules-you-must-know

- https://timesofindia.indiatimes.com/business/india-business/nps-rules-changed

10. When You Should Get Expert Help (Kustodian Life Bridge)

Choosing between SLW, Annuity, and Lump Sum is a math problem with tax consequences.

You should seek help if:

- You are confused about which "Tier" of your money is eligible.

- You have a large corpus and are worried about tax leaks.

- You are an NRI and unsure if SLW rules allow repatriation.

We Can Help: At Kustodian, we don't just process forms. We model your retirement cash flow to tell you exactly how much to take via SLW vs. an annuity.

Also read about [The NRI’s Guide to EPF & NPS Taxation, TDS & DTAA (2026)]

Conclusion:

Is SLW the Right Choice for Your Retirement? The introduction of the Systematic Lump Sum Withdrawal (SLW) facility has fundamentally changed how NPS subscribers plan their exit. By allowing you to stagger your withdrawals, the PFRDA has essentially turned your retirement corpus into a secondary pension, one that keeps earning returns while providing regular cash flow.

However, SLW isn't a "one-size-fits-all" solution. While it offers tax efficiency and discipline, it may not suit those with immediate large-ticket expenses like home renovation or debt repayment. The best approach is to assess your liquidity needs for 2026 and beyond. If you value a steady income stream over a lump-sum payout, SLW is likely your strongest ally in securing a worry-free retirement.

11. FAQ NPS SLW

Q1: What is SLW in NPS?

SLW stands for Systematic Lump Sum Withdrawal. It is a facility that allows you to withdraw your permitted lump-sum portion (60%) in instalments (Monthly/Quarterly/Yearly) till age 75, instead of taking it all at once.

Q2: Is SLW better than a one-time lump sum?

It depends on your discipline. If you are worried about spending your retirement money too fast, SLW is better. If you have a better investment opportunity outside NPS (like buying a house), a one-time lump sum is better.

Q3: Is SLW taxable?

The principal amount (the 60% corpus) is tax-exempt. However, the gains/returns accumulated on the balance during the SLW period may be taxable as per the income tax laws applicable in the year of withdrawal.

Q4: Can SLW replace my Annuity?

No. You still have to use at least 40% of your corpus to buy an Annuity. SLW only applies to the remaining 60%.

Q5: Can I stop SLW in the middle?

Yes. If you start SLW and later decide you need the remaining money urgently, you can usually cancel the instruction and withdraw the remaining balance as a lump sum.

Q6: What is the maximum age for SLW?

In 2026, you can avail the SLW facility until you reach 85 years of age. If any balance remains at 85, it is compulsorily redeemed and paid to your bank account.

Q7: Can I use SLW if my corpus is small?

Yes! If your corpus is ₹8 Lakh or less at retirement, you don't need to buy an annuity at all. You can put the entire 100% into an SLW plan and receive it as a monthly "salary" for years.

(Disclaimer: This guide is based on PFRDA regulations active in 2026. Rules regarding phased withdrawals are subject to change. Always consult a financial advisor before finalising your exit strategy.)