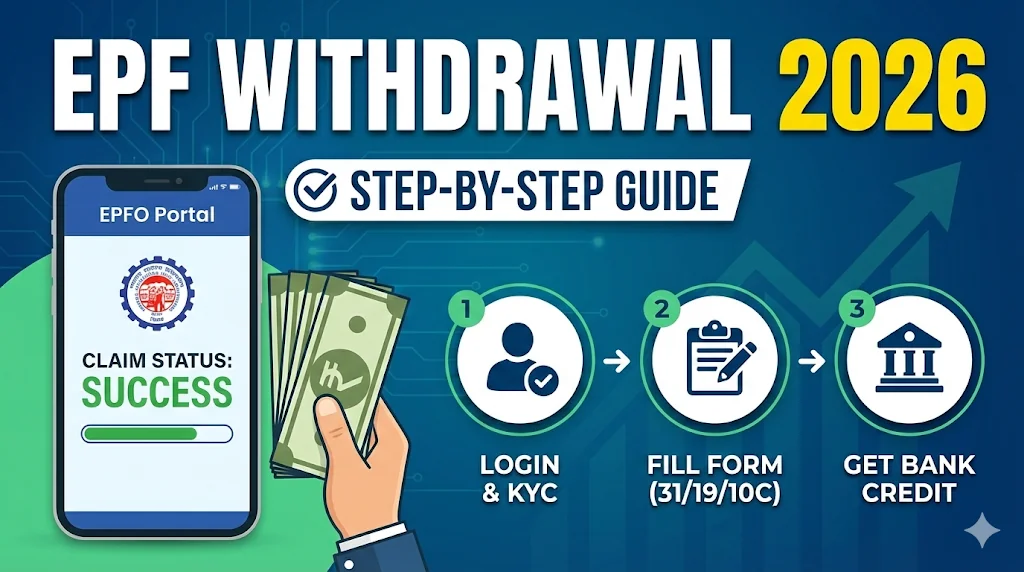

In 2026, withdrawing EPF online requires logging into the UAN Member Portal or UMANG App using an activated UAN and Aadhaar-linked mobile number. Ensure your Aadhaar, PAN, and bank KYC are fully verified. Use Form 19 for full settlement, Form 10C for pension, or Form 31 for advances.

Updated July 2026

Before filing for withdrawal, make sure you're actually eligible for final settlement. Under the Employees' Provident Funds Scheme, 2026, full withdrawal generally requires 12 months of unemployment, replacing the previous 2-month requirement.

Introduction

If you’ve ever switched jobs, retired, or faced an urgent financial need, you might have considered withdrawing money from your Employee Provident Fund (EPF). In the past, this often meant paperwork, employer signatures, and long visits to the regional PF office. But today, in 2026, the EPF withdrawal process has become much simpler and is now almost fully online.

In this guide, we’ll explain everything you need to know about how to withdraw EPF online in 2026, including eligibility rules, the latest EPFO requirements, documents you’ll need, and a step-by-step process using the UAN Member Portal and the UMANG App. In 2026, the new EPFO 3.0 framework has simplified the rules to help you get your money without the 'rejection' heartbreak.

Think of this blog as your complete EPF withdrawal checklist - clear, updated, and easy to follow.

What is EPF Withdrawal?

EPF withdrawal simply means accessing the savings you’ve accumulated in your Employees’ Provident Fund account. This includes a pool of money from your and your employers' contributions.

This pool of money includes:

- Your own monthly contributions

- Your employer’s contributions

- The interest is earned on both.

When it comes to withdrawing, there are two main options:

Full Withdrawal

You can withdraw your entire EPF balance after retirement or after becoming eligible for final settlement under the EPF Scheme, 2026 (generally after 12 months of unemployment, or in other eligible exit situations such as permanent disability, retrenchment, VRS or emigration).

Partial Withdrawal (Advance)

Instead of closing your account, you can take out only a portion of your savings. This is allowed under certain conditions, such as:

- Essential Needs (Illness, Marriage, Education).

- Housing Needs (Purchase, Construction, Loan Repayment).

- Special Circumstances (Unemployment, Natural Calamity).

Note: The service requirement for partial withdrawals has been standardised to 12 months (down from 7 years for marriage/education in some older rules).

Frequency update: members can now withdraw for Education up to 10 times and Marriage up to 5 times during their career.

Tip: As of 2026, claims up to ₹5,00,000 for illness, education, or marriage are now auto-settled within 72 hours without human intervention.

When Can You Withdraw EPF? (Eligibility Rules - 2026)

Under the latest EPFO rules (2026), withdrawals are allowed in these situations:

- At Retirement (58 years): You can withdraw the entire EPF balance.

- Unemployment (12 months): Members generally become eligible for full EPF settlement after remaining unemployed for 12 months under the Employees' Provident Funds Scheme, 2026.

- Partial Withdrawal: You don’t have to wait until 58. Advances are allowed in real-life scenarios such as:

Important Rule: Linking your PAN with EPF is now mandatory to avoid higher TDS on withdrawals.

Documents Required for EPF Withdrawal in 2026

Before starting the process, make sure these are ready:

- UAN (Universal Account Number) - Activated and linked with Aadhaar.

- Aadhaar card - For eKYC verification.

- PAN card - To avoid higher TDS deductions.

- Bank account details - Must be linked with UAN.

- Mobile number linked with Aadhaar - For OTP verification.

If you’re confused about missing documents or KYC mismatches, you can request a Free EPF Audit from Kustodian. life to verify everything before applying.

Step-by-Step Guide: EPF Withdrawal Online Process

There are two main ways to withdraw EPF online. You can use the EPFO official website or the UMANG App:

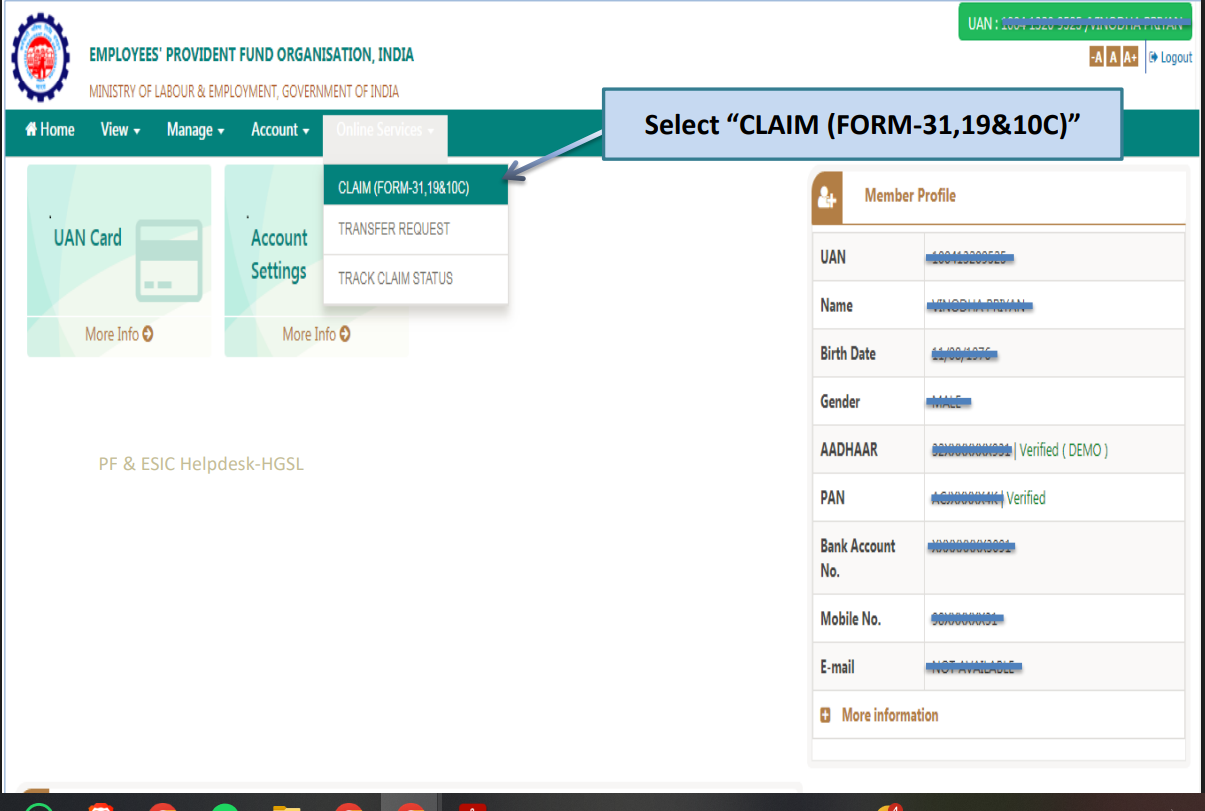

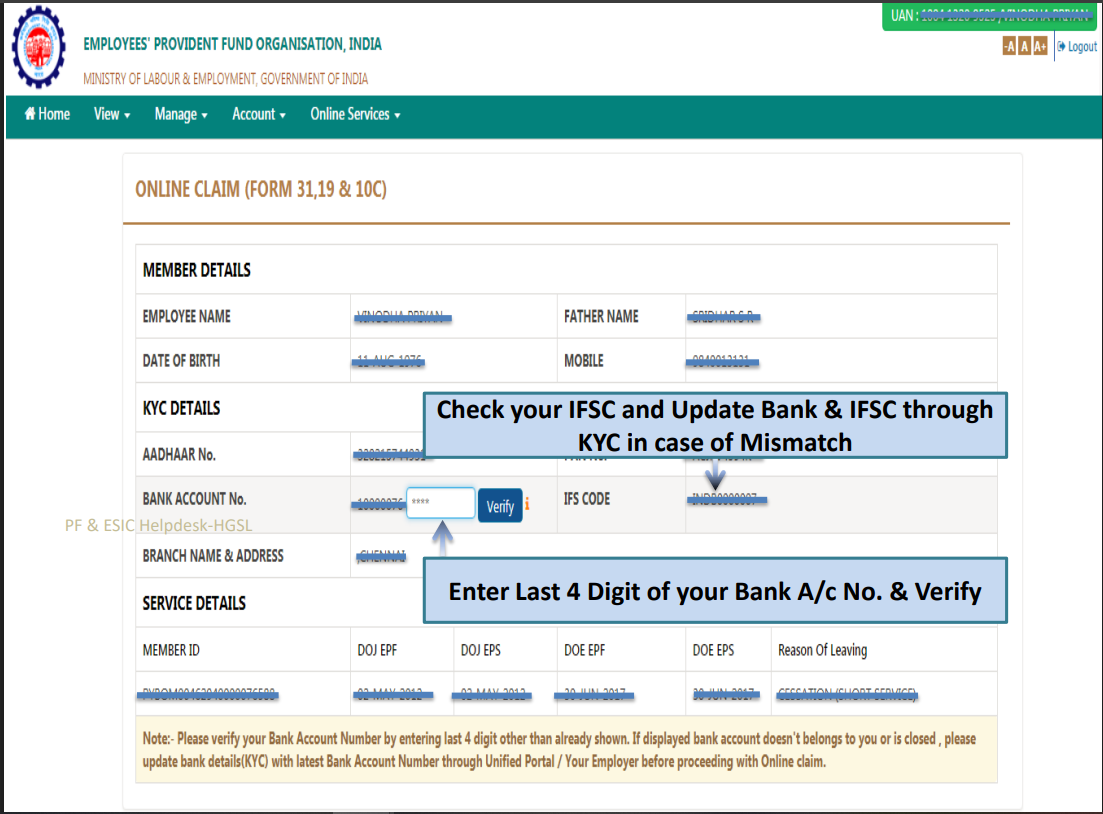

Method 1: Through the UAN Member Portal (EPFO Website)

- Login:

- Verify KYC:

- Go to Online Services:

- Authenticate:

- Choose Claim Type:

- Submit Claim:

Once submitted, you’ll get an SMS notification. Processing usually takes 5–15 working days. Amount is credited directly to your bank account.

Method 2: Through the UMANG Mobile App

- Download UMANG App (available on Android/iOS).

- Log in with an Aadhaar-linked mobile number. (You can also log in using the FaceRD app using face authentication.)

- Go to EPFO services → Employee Centric Services → Raise Claim.

- Enter UAN and verify OTP.

- Select claim type (PF final settlement, advance, pension withdrawal).

- Submit the claim online.

UMANG is a handy alternative if you don’t want to log in via the website.

How Much EPF Can You Withdraw?

- Full Withdrawal: Allowed only on retirement or 12 months of unemployment.

- Partial Withdrawal: Amount varies according to the requirement (marriage, medical emergency, buying a house, etc).

| Withdrawal Category | Eligibility | Maximum Withdrawal |

|---|---|---|

| Medical Treatment | 12 months membership | Up to the eligible balance |

| Education | 12 months membership | Up to the eligible balance (10 withdrawals) |

| Marriage | 12 months membership | Up to the eligible balance (5 withdrawals) |

| Housing Needs | 12 months membership | Up to 75% |

| Final Settlement | Retirement / 12 months unemployment | 100% |

Tax Rules for EPF Withdrawal in 2026

- If the service is less than 5 years:

- If service is 5 years or more:

- Threshold condition:

Important Clarification

- Even if TDS is not deducted, withdrawals before 5 years of service may still be taxable as “Income from Salary” (employee’s contribution + interest) and “Income from Other Sources” (employer’s contribution + interest).

- If you submit Form 15G/15H and your income is below the taxable limit, no TDS will be deducted.

5 Common Reasons Why EPF Withdrawal Gets Rejected

- Aadhaar is not linked with UAN.

- KYC not verified (PAN, bank details mismatch).

- Incorrect bank account details.

- Signature mismatch in uploaded documents.

- Multiple member IDs are not merged under one UAN.

Before reapplying, get a Free EPF Audit from Kustodian.life to detect the exact reason for rejection and prevent delays.

Still not sure why the EPF claim got rejected?

You’re not alone. Kustodian specializes in fixing EPF rejections quickly.

Book a Free Expert Call and get your issue resolved fast.

Tips for a Smooth EPF Withdrawal in 2026

- Ensure KYC and Aadhaar are updated in advance.

- Use the same mobile number linked with Aadhaar.

- Keep documents scanned in PDF format.

- Track claim status regularly on the EPFO portal or UMANG.

Conclusion

The EPF withdrawal process in 2026 is now faster and more convenient than ever. By keeping your UAN active, KYC updated, and Aadhaar linked, you can easily withdraw your PF balance through the EPFO portal or the UMANG app without any unnecessary delays.

If you encounter any issues or face claim rejections, the team at Kustodian.life is here to guide you step by step, ensuring you receive your entitled PF balance quickly and hassle-free.

Frequently Asked Questions (FAQs)

1. How long does an EPF withdrawal take in 2026 ?

Usually 5-15 working days, provided KYC is complete.

2. Can I withdraw EPF while working?

Only partial withdrawals (advance) are allowed for specific purposes.

3. Is Aadhaar face authentication mandatory in 2026?

Yes, EPFO has made Aadhaar face authentication mandatory for certain services, especially for retirees/pensioners. For withdrawals, Aadhaar OTP verification is standard.

4. Can NRIs withdraw EPF online?

Yes, but they must have an active UAN, an Indian bank account, and Aadhaar.

5. Do I need employer approval for EPF withdrawal?

No, if your Aadhaar is linked with UAN and KYC is complete, employer approval is not required.

Q: How do I avoid TDS on EPF withdrawal if my service is less than 5 years?

A: If your total service is less than 5 years and the withdrawal amount exceeds ₹50,000, TDS is applicable. However, if your total annual income is below the taxable limit, you can submit Form 15G (for under 60) or Form 15H (for seniors) along with your claim to prevent TDS deduction.

Q: Is the pension portion (EPS) withdrawable along with PF?

A: Yes, but only if your total service is less than 10 years and you have left employment. You need to file Form 10C to withdraw the pension corpus. If your service is more than 10 years, you cannot withdraw the pension lump sum; you will receive a monthly pension certificate instead.

Q: Is the employer’s signature required for online EPF withdrawal?

A: No. If your Aadhaar is linked to your UAN and your bank KYC is digitally approved by your employer, you do not need physical signatures or employer approval to submit a withdrawal claim online.

Q: Why was my EPF claim rejected even though my documents are correct? A: Common reasons for rejection in 2026 include name mismatches between Aadhaar and Bank records, unclear cheque/passbook scans, or failing the "Penny Drop" verification (where the bank name doesn't match the UAN name perfectly). Merging old Member IDs before applying is also crucial.

Q: Can I credit my withdrawal to a bank account not linked to my UAN?

A: No. The withdrawal amount is credited only to the bank account currently verified and linked to your UAN. If you want to use a different account, you must update your Bank KYC on the portal and wait for employer approval before filing the claim.

Q: Can I withdraw my full EPF amount without retiring?

A: Yes, but only under specific conditions. You can withdraw your full EPF balance if you remain unemployed for 12 months or more. If you are still working, you cannot do a full withdrawal; you can only take a partial advance for specific needs like illness, marriage, or housing.

Q: What is the maximum limit for medical advance withdrawal in 2026?

A: For medical emergencies, you can withdraw the lower of: 6 months' basic salary (+DA) OR your entire employee share with interest. There is no minimum service requirement for this, and claims up to ₹1 Lakh (and sometimes higher under auto-mode) are often settled within 72 hours.

Q: Should I withdraw my EPF or transfer it when I change jobs?

A: It is highly recommended to transfer your EPF to the new employer rather than withdrawing it. Withdrawing resets your 5-year continuous service record, making future withdrawals taxable. Transferring keeps your service history intact and your money compounding

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. EPFO rules may vary based on individual records and processing practices.