For decades, the Employee Provident Fund (EPF) was celebrated as the ultimate "Triple Exempt" (EEE) investment tax-free at contribution, tax-free during growth, and tax-free at withdrawal. However, the rules have shifted. With the implementation of the New Labour Codes and recent Union Budget updates, the "tax-free" status of your PF now comes with fine print.

Whether it’s the ₹2.5 lakh interest threshold, the ₹7.5 lakh combined employer cap, or the strict 5-year service rule for withdrawals, staying informed is the only way to protect your retirement corpus from unexpected TDS and tax liabilities.

In this comprehensive 2026 guide, we break down exactly how your EPF, VPF, and PPF are taxed, helping you navigate the maze of Form 15G, NRI regulations, and the latest EPFO mandates.

Introduction - EPF and PF Taxation India 2026

Employee Provident Fund (EPF), Public Provident Fund (PPF), and Voluntary Provident Fund (VPF) are among the most trusted retirement and savings options for millions of Indians.

Different authorities regulate these schemes. EPF and VPF fall under the Employees' Provident Fund Organisation (EPFO) and the Income Tax Act, 1961. PPF is overseen by the Government of India through banks and post offices, with tax rules guided by the Central Board of Direct Taxes (CBDT).

The big advantage? All three are designed to help you build long-term wealth with attractive tax benefits. But here’s the catch: while contributions and interest are often tax-free, there are specific situations where tax on EPF withdrawals, income tax on PPF maturity, or VPF tax implications can come into play.

Understanding these rules in 2026 is not just about compliance; it’s about making smarter financial decisions. Knowing when withdrawals are tax-free, when TDS applies, and how forms like 15G/15H can help you avoid unnecessary deductions ensures you don’t lose money to taxes unknowingly.

Need expert help with your EPF tax planning?

Don’t let complex TDS and withdrawal rules eat into your savings.

Book a free call with Kustodian’s experts to get your PF taxation and withdrawal strategy reviewed.

Think of it like this: saving is only half the job; knowing the tax rules ensures you actually get to keep more of what you saved.

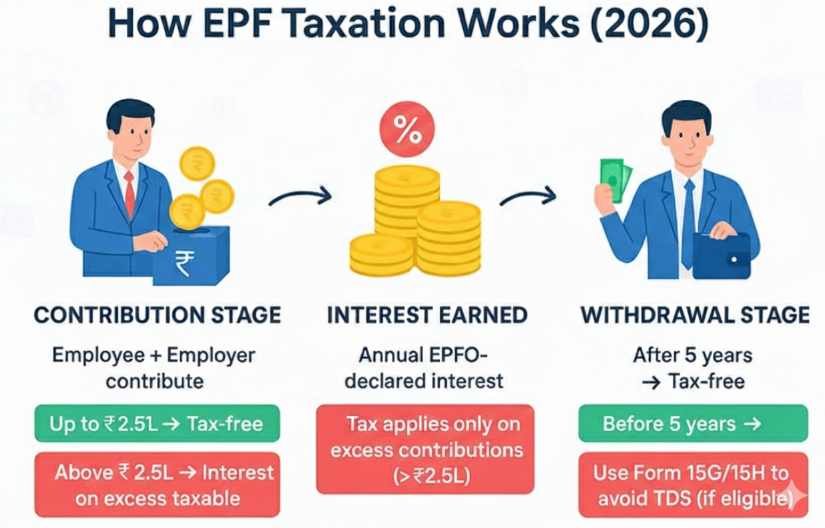

Understanding the Basics of EPF, PF & VPF Taxation in India

Before diving into rules on withdrawals, exemptions, and forms, it’s important to understand how Provident Fund taxation works at a fundamental level.

Every month, a portion of your salary (typically 12% of Basic + DA) goes into the Employees’ Provident Fund (EPF). Your employer also contributes, though part of it is diverted to the Employees’ Pension Scheme (EPS). Over time, this balance grows with interest declared annually by the EPFO, making EPF a powerful retirement tool.

Why Tax Rules Apply

Provident Funds enjoy an EEE (Exempt–Exempt–Exempt) status under the Income Tax Act:

- Exempt at Contribution Stage: Employee contributions qualify for deductions under Section 80C (up to ₹1.5 lakh).

- Exempt on Growth: Annual interest is tax-free up to the contribution limits.

- Exempt on Withdrawal: If conditions are met (like minimum service period), the final withdrawal is also tax-free.

However, since FY 2021-22, tax rules have tightened. Contributions above ₹2.5 lakh per year now attract tax on the interest portion. Withdrawals made before completing five years of service can also become taxable.

EPF, PF, and VPF remain highly tax-efficient, but knowing the limits and conditions is key to avoiding surprises.

| Scenario income | Tax Treatment | Action Required |

| Contribution ≤ ₹2.5 lakh | Fully tax-free | None |

| Contribution > ₹2.5 lakh | Interest on excess taxable each year | Report taxable interest in ITR. |

| Withdrawal after 5 years | Entire amount tax-free | None |

| Withdrawal before 5 years | Taxable + TDS deducted by EPFO | File Form 15G/15H if eligible |

Tax on Employee Contributions

For most salaried individuals, the first question is simple: “Is my contribution to EPF taxable?” The answer is, your mandatory contribution of 12% of Basic Salary + Dearness Allowance is fully exempt from tax, provided it stays within prescribed limits.

The ₹2.5 Lakh Annual Threshold

Under current rules:

- If your annual EPF contribution is up to ₹2.5 lakh, the entire contribution and the interest earned on it remain tax-free.

- If your contribution exceeds ₹2.5 lakh in a financial year, the interest earned on the excess portion becomes taxable in your hands.

Example: Suppose you contribute ₹3,00,000 in one financial year.

- Contribution up to ₹2,50,000 → fully exempt.

- Excess contribution = ₹50,000.

- Interest earned on ₹50,000 will be taxable as “Income from Other Sources” each year.

This rule was introduced to curb very high-income employees from parking unlimited funds in EPF only for tax-free interest.

Special Rule for Non-Contributory Employer Accounts

For employees where the employer does not contribute to EPF, typically government employees under the General Provident Fund (GPF) system, the limit is more generous.

- In such cases, the annual exemption limit is ₹5 lakh.

- Only if contributions exceed ₹5 lakh will the interest on the excess amount become taxable.

Why This Rule Matters

For most middle-income salaried employees, EPF contributions never cross the ₹2.5 lakh limit (since 12% of salary generally remains lower). But for high-salaried professionals or those making voluntary contributions (VPF), this rule is critical to remember.

It ensures you plan your investments holistically, for instance, by balancing EPF with NPS or ELSS, instead of relying on one instrument beyond the exemption threshold.

Tax on Employer Contributions

While your own EPF contributions have clear thresholds, the rules for employer’s contributions are slightly different and often overlooked by employees. Let’s break it down:

By law, your employer contributes 12% of your Basic Salary + Dearness Allowance (DA) towards your retirement benefits.

- A part of this goes into your EPF account.

- Another part may go into the Employees’ Pension Scheme (EPS).

As long as the employer’s contribution stays within 12% of your basic + DA, it is completely tax-free.

When Does It Become Taxable?

If your employer contributes more than 12% of your basic + DA to EPF, the excess contribution is treated as an extra taxable benefit in your hands.

- This amount gets added to your salary income and is taxed as per your slab rate.

Example: If your basic + DA = ₹50,000 per month, then 12% = ₹6,000.

- Employer contribution up to ₹6,000/month → tax-free.

- If the employer contributes ₹7,000/month → ₹1,000/month (₹12,000/year) will be taxable.

The ₹7.5 Lakh Combined Cap Rule

In 2020, a new rule was introduced to prevent high earners from receiving large tax-free benefits from retirement funds.

- Employer contributions to EPF, NPS, and Superannuation Fund are capped at ₹7.5 lakh per financial year.

- If the employer’s contribution across these three exceeds ₹7.5 lakh, the excess is taxable.

- Moreover, the interest, dividend, or returns earned on this excess contribution is also taxable every year.

Example:

- Employer contributes ₹3 lakh to EPF, ₹3 lakh to NPS, and ₹2.5 lakh to Superannuation.

- Total = ₹8.5 lakh.

- Exceeds ₹7.5 lakh cap by ₹1 lakh → this ₹1 lakh is taxable in your hands.

- Plus, any annual income generated on that ₹1 lakh is also taxable.

Why This Rule Matters

For middle-income earners, employer contributions usually remain within safe limits. But for CXOs, senior managers, and high-income professionals, employer contributions to EPF + NPS + Superannuation can easily breach the ₹7.5 lakh cap.

Failing to account for this could result in unexpected tax liability when filing returns. Keeping track of Form 16 details and your annual salary structure is essential.

Summary Table:

| Type of Contribution | Limit / Threshold | Tax Status | When It Becomes Taxable |

| Employee’s Contribution | 12% of Basic + DA (mandatory) | Fully exempt | If the total annual contribution exceeds ₹2.5 lakh (₹5 lakh if no employer contribution); interest on the excess is taxable. |

| Employer’s Contribution to EPF | Up to 12% of Basic + DA | Exempt | Contribution beyond 12% is taxable as a perquisite. |

| Combined Employer Contribution (EPF + NPS + Superannuation) | Up to ₹7.5 lakh per year | Exempt | If total > ₹7.5 lakh, the excess + returns on excess are taxable |

| Employee + Employer Withdrawal after 5 years | No limit | Fully exempt | Withdrawal before 5 years → taxable (TDS applicable if > ₹50,000) |

Tax on Interest Earned

The interest credited annually to your EPF account is what makes it such a powerful retirement savings tool. The rate is declared by the EPFO’s Central Board of Trustees every year and approved by the Ministry of Finance.

- For FY 2024-25, the EPF interest rate has been declared at 8.25%.

- This interest is calculated monthly on the running balance and credited to your account at the end of the financial year.

Is EPF Interest Always Tax-Free?

Not always. Until March 31, 2021, all interest earned on EPF contributions was fully tax-free. But from FY 2021-22 onwards, new rules were introduced to tax interest earned on excess employee contributions.

- As explained earlier, if your contribution exceeds the ₹2.5 lakh threshold, interest on the excess becomes taxable.

- For accounts where the employer does not contribute (like government employees under GPF), the limit is ₹5 lakh.

How Is Taxable Interest Calculated?

The EPFO now maintains two separate accounts within your PF:

- Non-Taxable Contribution Account → Contributions up to ₹2.5 lakh (or ₹5 lakh for govt employees) + interest earned on it → remains tax-free.

- Taxable Contribution Account → Contributions beyond the limit + interest earned on that excess → interest is taxable each year.

Example:

- Suppose you contribute ₹3,00,000 to EPF in FY 2024-25.

- Threshold = ₹2,50,000.

- Excess = ₹50,000.

- Interest rate = 8.25%.

- Interest on excess = ₹50,000 × 8.25% = ₹4,125.

- This ₹4,125 will be taxed as “Income from Other Sources” in your ITR for FY 2024-25.

Key Point to Remember

- Tax applies only to the interest on excess contributions, not on the entire balance.

- The EPFO provides annual passbooks where taxable interest is shown separately for transparency.

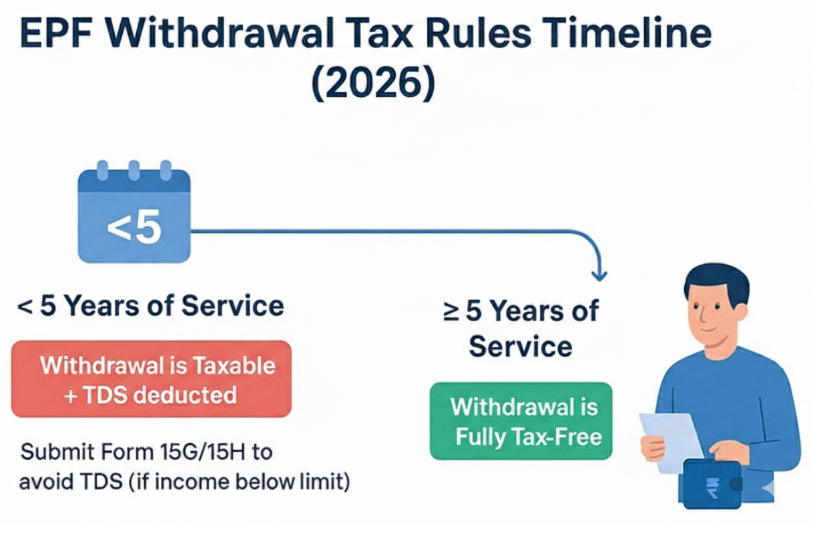

Tax on EPF Withdrawals

Withdrawing your EPF balance is one of the most crucial points where taxation comes into play. The rules depend on how long you have continuously contributed to EPF.

1. Withdrawal Before 5 Years of Continuous Service

If you withdraw your EPF before completing 5 years of continuous service, the withdrawal becomes taxable. Here’s the breakdown:

- Employee’s Own Contribution → Not taxed directly, but if you claimed a tax deduction under Section 80C, it will be reversed and added to your taxable income.

- Employer’s Contribution → Fully taxable as “Salary Income.”

- Interest on Employer’s Contribution → Taxable as “Salary Income.”

- Interest on Employee’s Contribution → Taxable as “Income from Other Sources.”

Example: If you worked for 3 years and withdrew ₹3,00,000:

- ₹1,20,000 (your contributions) → Section 80C benefit reversed.

- ₹1,20,000 (employer contributions) → taxed as Salary Income.

- ₹60,000 (interest portion) → taxed separately as Salary/Other Sources.

2. Withdrawal After 5 Years of Continuous Service

If you withdraw after completing 5 years of continuous service, the entire withdrawal amount is tax-free , including both contributions and accumulated interest.

3. TDS (Tax Deducted at Source) Rules

To ensure compliance, EPFO applies TDS on withdrawals before 5 years:

| Condition | TDS Rate | Threshold |

| Withdrawal before 5 years, amount > ₹50,000, PAN provided | 10% | Applies to the entire taxable amount |

| Withdrawal before 5 years, amount > ₹50,000, No PAN provided | 30% | Applies to the entire taxable amount |

| Withdrawal ≤ ₹50,000 before 5 years | No TDS | N/A |

Note: Even if TDS is not deducted, you still need to declare and pay tax on the withdrawal in your ITR if it is taxable.

Key Takeaway

- Less than 5 years of service → withdrawal taxable (with TDS implications).

- 5 years or more of service → withdrawal fully exempt.

- Always ensure PAN is updated with EPFO to avoid higher TDS at 30%.

Planning to withdraw your PF? Here’s a detailed guide on the EPF withdrawal online process to help you complete it smoothly without delays

2 Latest Rules and Updates (2026)

Staying updated on the most recent EPF developments helps ensure you're not caught off guard, especially when it involves your hard-earned savings. Here’s a rundown of key updates for 2025:

1. EPF Interest Rate: Projected to remain at 8.25% for FY 2025–26

The Employees’ Provident Fund Organisation (EPFO) confirmed a steady interest rate of 8.25% for the financial year 2025–26, following approval by the Finance Ministry.

This decision, impacting over 70 million subscribers, maintains the stability of returns, providing continued assurance for retirees and salaried individuals alike.

This unchanged rate from FY 2023–24 further strengthens the reliability of EPF as a long-term, low-risk investment tool.

2. Budget 2026 Tax Landscape: EPF Still Plays a Key Role

The Union Budget 2026 brought notable tax reform that enhances EPF’s attractiveness:

- The tax rebate threshold under the New Tax Regime was raised substantially, allowing up to ₹12 lakh of tax-free income (inclusive of the ₹75,000 standard deduction for salaried individuals).

- EPF contributions (up to eligible limits) remain valuable even under the New Tax Regime, especially because employer contributions (upto 12%) and interest income continue to be exempt.

Together, these changes make EPF even more tax-efficient for middle-income earners choosing between tax regimes.

The EPFO has rolled out several other changes this year that go beyond taxation. To stay fully updated, check out our guide on All Major EPFO Rule Changes in 2025: What Employees Must Know.

Filing Form 15G for EPF Withdrawals - Step-by-Step Guide for Indian Employees

Form 15G helps eligible taxpayers avoid TDS (Tax Deducted at Source) on premature EPF withdrawals. If your annual income is below the taxable threshold, submitting this form ensures you receive your PF amount without the deduction of 10% TDS.

When Should You File Form 15G for EPF?

You can file Form 15G under the following conditions:

- Your total annual income is below ₹2.5 lakh (₹3 lakh for senior citizens below 60).

- You are withdrawing your EPF balance before completing 5 years of continuous service.

- You want to prevent 10% TDS on your withdrawal.

Note: If your income is taxable, filing Form 15G incorrectly may lead to penalties.

Step-by-Step Process to Submit Form 15G for EPF

Step 1: Download Form 15G from the EPFO Member Portal or the Income Tax Department website.

Step 2: Fill in personal details such as name, PAN, address, and estimated total income.

Step 3: Attach the filled Form 15G with your EPF withdrawal application.

Step 4: Once validated, EPFO processes your withdrawal without TDS deduction.

Key Points to Remember

- Form 15G must be submitted before withdrawal processing.

- False declarations can invite penalties under Section 277 of the IT Act.

- Form 15G is valid only for the financial year in which it is filed.

- If you make multiple withdrawals, you need to file a separate Form 15G for each withdrawal.

Alternative for Senior Citizens - Form 15H

If you are a senior citizen (60+ years) with an annual income below ₹5 lakh, you can use Form 15H instead of Form 15G. This form offers the same benefit of avoiding TDS on EPF withdrawals.

Pro Tip: Even if no TDS is deducted using Form 15G or 15H, you still need to declare your EPF withdrawal in ITR if it is taxable.

Filing Form 15G or 15H?

A small mistake can delay or reject your claim.

Book a free call with Kustodian’s documentation experts , we’ll help you file it right the first time.

EPF Taxation for NRIs and Legal Heirs

1. NRIs Withdrawing EPF

If you are an NRI withdrawing your EPF balance, the tax treatment changes compared to resident employees:

- TDS Deduction: EPFO deducts 30% TDS (plus applicable surcharge and cess) on the total withdrawal amount if PAN is not updated

- If PAN is updated, TDS is 10% on withdrawals exceeding ₹50,000 before 5 years of service.

- Double Taxation Avoidance Agreement (DTAA): NRIs can claim lower TDS rates or a refund later when filing ITR in India, depending on the DTAA with their resident country.

- After 5 years of continuous service, withdrawals are exempt even for NRIs.

Example: An NRI working in Dubai withdraws EPF after 7 years of service → no tax applies in India. But if withdrawn in 3 years → TDS applies as per the above rules.

2. Legal Heirs Claiming EPF After the Death of an Employee

When an EPF member passes away, the nominee/legal heir is entitled to:

- Employee’s EPF balance (contributions + interest)

- Employer’s contribution

- Employees’ Deposit Linked Insurance (EDLI) benefit, if eligible

Tax Treatment:

- Lump-sum EPF received by nominee/legal heir is fully tax-free under Section 10(12) of the Income Tax Act.

- The amount is treated as a capital receipt, not “income,” hence not taxable in the hands of the legal heir.

- EDLI insurance payout is also exempt from income tax [EPFO Rules].

Example: If an employee passes away with ₹15 lakh in EPF, the nominee (spouse/child/parent) receives the full balance without any tax liability.

Example Scenarios: Easy Breakdown

Understanding EPF tax rules becomes much simpler with concrete examples. Let’s break it down into common cases most employees face.

Case 1: Contribution Within Limit (Fully Exempt)

Employee contributes ₹2 lakh annually (well below the ₹2.5 lakh limit).

| Particulars | Amount | Tax Treatment |

| Employee Contribution | ₹2,00,000 | Exempt |

| Employer Contribution (12%) | ₹1,80,000 | Exempt (within 12% limit) |

| Interest Earned | ~₹32,000 | Exempt (since contribution ≤ ₹2.5 lakh) |

| Total Taxable | – | Nil |

In this case, everything remains tax-free.

Case 2: Contribution Above Limit (Interest Taxable)

Employee contributes ₹4 lakh annually → exceeds the threshold.

| Particularsthe | Amount | Tax Treatment |

| Employee Contribution | ₹4,00,000 | Exempt |

| Employer Contribution (12%) | ₹2,40,000 | Exempt (within 12% limit) |

| Interest Earned (assume 8.25%) | ~₹49,500 | Taxable on excess contribution (₹1.5 lakh excess over ₹2.5 lakh) → ~₹18,500 taxable |

| Total Taxable | ₹18,500 | Added to income, taxed as per slab |

Here, only the interest on excess contribution (₹1.5 lakh) becomes taxable.

Case 3: Withdrawal Before 5 Years (Taxable)

Employee withdraws after 4 years of service, with the following balances:

| Particulars | Amount | Tax Treatment |

| Employee’s Own Contribution | ₹3,00,000 | Exempt (already taxed income) |

| Employer Contribution | ₹3,00,000 | Taxable (added to income) |

| Interest Earned (Employee + Employer) | ~₹1,20,000 | Taxable |

| TDS Deduction | 10% (if PAN linked, withdrawal > ₹50,000) | Collected upfront |

| Total Taxable | ₹4,20,000 | Added to income, taxed as per the slab |

In this case, the employee withdraws before completing the service threshold and thus, both the employer’s contribution and interest become taxable.

Case 4: Tax Planning with VPF and Excess EPF Contributions

Let’s understand how excess contributions to EPF/VPF can impact your tax planning and what adjustments you can make to save tax.

Employee Profile

- Basic Salary: ₹80,000/month

- EPF Contribution (12%): ₹1,15,200 annually

- VPF Contribution (Voluntary): ₹1,50,000 annually

- Total Contribution: ₹2,65,200

Tax Implications

- Section 80C Limit: Maximum deduction allowed is ₹1.5 lakh.

- Contribution Threshold: EPF + VPF contributions above ₹2.5 lakh/year attract tax on the interest portion (rule effective FY 2021-22).

- Example Case:

Why This Matters

While EPF and VPF are excellent tax-saving + safe instruments, over-contributing can lead to interest taxation, reducing the overall post-tax return.

Tax Planning Tip

To optimise taxes, instead of contributing ₹1.5 lakh to VPF, reduce it by ₹15,200 so that your total contribution stays at ₹2.5 lakh. The saved ₹15,200 can be invested in:

- ELSS (Equity Linked Saving Scheme) – offers tax benefit + potential higher returns.

- PPF or Sukanya Samriddhi Yojana (if eligible).

- Tax-saving fixed deposits or NPS (for additional Section 80CCD(1B) benefit).

This way, you maximize deductions under Section 80C and avoid the tax on excess interest.

Pro Tip: Always review your annual EPF + VPF contributions in April itself to ensure you stay below the ₹2.5 lakh limit and align with your long-term investment goals.

FAQs

1. Is PF completely tax-free in India?

Not always. PF withdrawals are tax-free if you complete 5 years of continuous service. However, since FY 2021-22, if your combined EPF + VPF contributions exceed ₹2.5 lakh in a year, the interest earned on the excess portion becomes taxable. This taxable interest is added to your annual income and taxed as per your slab rate.

2. Is the employer’s contribution to EPF taxable?

Employer’s contribution is tax-free up to 12% of your basic salary + DA. Beyond that, it is taxed as a perquisite. Also, if the combined employer contributions to EPF + NPS + Superannuation Fund exceed ₹7.5 lakh in a financial year, the excess is taxable.

3. Do I need to pay tax if I withdraw EPF after 5 years?

No. If you withdraw EPF after 5 years of continuous service, the entire amount (employee contribution, employer contribution, and interest) is completely tax-free under Section 10(12) of the Income Tax Act.

4. What is the TDS on EPF withdrawal before 5 years?

- Withdrawal > ₹50,000 with service < 5 years → 10% TDS (if PAN linked).

- If PAN is not linked, → 30% TDS applies.

- You can later claim a refund or adjustment when filing ITR.

5. How is TDS on EPF withdrawal applied for NRIs?

For NRIs, TDS is deducted at 30% (plus surcharge and cess) if PAN is not linked, and 10% if PAN is linked. Ensuring your PAN is updated with EPFO helps reduce TDS on withdrawals.

6. What happens if I transfer EPF instead of withdrawing?

If you transfer EPF from one employer to another, no tax applies, regardless of service length. The 5-year clock of “continuous service” also continues. This is the safest option to avoid unnecessary tax deductions.

7. Is the EPF received by a nominee or legal heir taxable?

No. If an employee passes away, the EPF balance (employee + employer contributions + interest) is tax-free for nominees/legal heirs. The payout is treated as a capital receipt, not income. The EDLI insurance benefit is also fully exempt.

8. When should I file Form 15G for EPF withdrawal in India?

You should submit Form 15G if:

- Your total annual income is below ₹2.5 lakh (₹3 lakh for senior citizens).

- You’re withdrawing EPF before completing 5 years of service.

- You want to avoid 10% TDS being deducted on the withdrawal.

Important: Filing Form 15G is only valid if you genuinely meet the eligibility criteria. A false declaration can attract penalties.

Useful Links & Resources

Official EPF and Government Resources

- Employees' Provident Fund Organisation (EPFO)Official portal for EPF members where you can check passbooks, file claims, update KYC details, and access circulars.https://www.epfindia.gov.in

- Income Tax Department of IndiaProvides official tax rules, forms like Form 15G/15H, and income tax filing guidelines.https://www.incometax.gov.in

- Central Board of Direct TaxesThe authority responsible for implementing direct tax laws in India and issuing tax circulars.https://www.cbdt.gov.in

- Ministry of FinanceOfficial announcements related to Union Budget updates and financial policy changes affecting EPF.https://www.finmin.nic.in

Helpful EPF Guides for Employees

- EPF Withdrawal Online Process – Step-by-Step GuideLearn how to withdraw your PF balance online using the UAN portal.

- EPF Transfer Process When Changing JobsUnderstand how to transfer your EPF balance to a new employer without triggering taxes.

- Latest EPFO Rule Changes Employees Must KnowA summary of recent policy changes affecting EPF contributions, withdrawals, and compliance.

Tax Forms and Documents

- Form 15G / Form 15H DownloadUsed to prevent TDS deduction on EPF withdrawals if your income falls below the taxable limit.https://www.incometax.gov.in/forms

- EPF Member Passbook PortalCheck your EPF balance, contributions, and interest credited annually.https://passbook.epfindia.gov.in

Conclusion

EPF remains one of the safest and most rewarding retirement savings tools in India. But as we’ve seen, taxation rules can sometimes feel like a maze - thresholds, exemptions, TDS, and exceptions that change with every Budget or EPFO circular.

The good news? With the right understanding, you can make smarter decisions:

- Keep contributions within limits to enjoy maximum tax-free benefits.

- Avoid early withdrawals unless necessary.

- Stay updated with the latest EPFO notifications and Income Tax rules.

At Kustodian. life, we specialize in helping individuals, NRIs, and families navigate EPF-related complexities, whether it’s taxation, claim rejections, inheritance after a loved one’s passing, or simply ensuring you don’t lose out on your hard-earned money.

If you’re unsure about your EPF taxation or facing challenges with a claim, let us simplify it for you. Our team ensures accuracy, compliance, and peace of mind so you can focus on what truly matters.