EPFO announces major EPF rule latest updates 2025 - new EPF withdrawal rules, Vishwas Scheme to reduce penalties, doorstep DLC for pensioners, and EPFO 3.0 digital reforms. Here’s what it means for you.

Introduction - EPF Latest Rule Updates

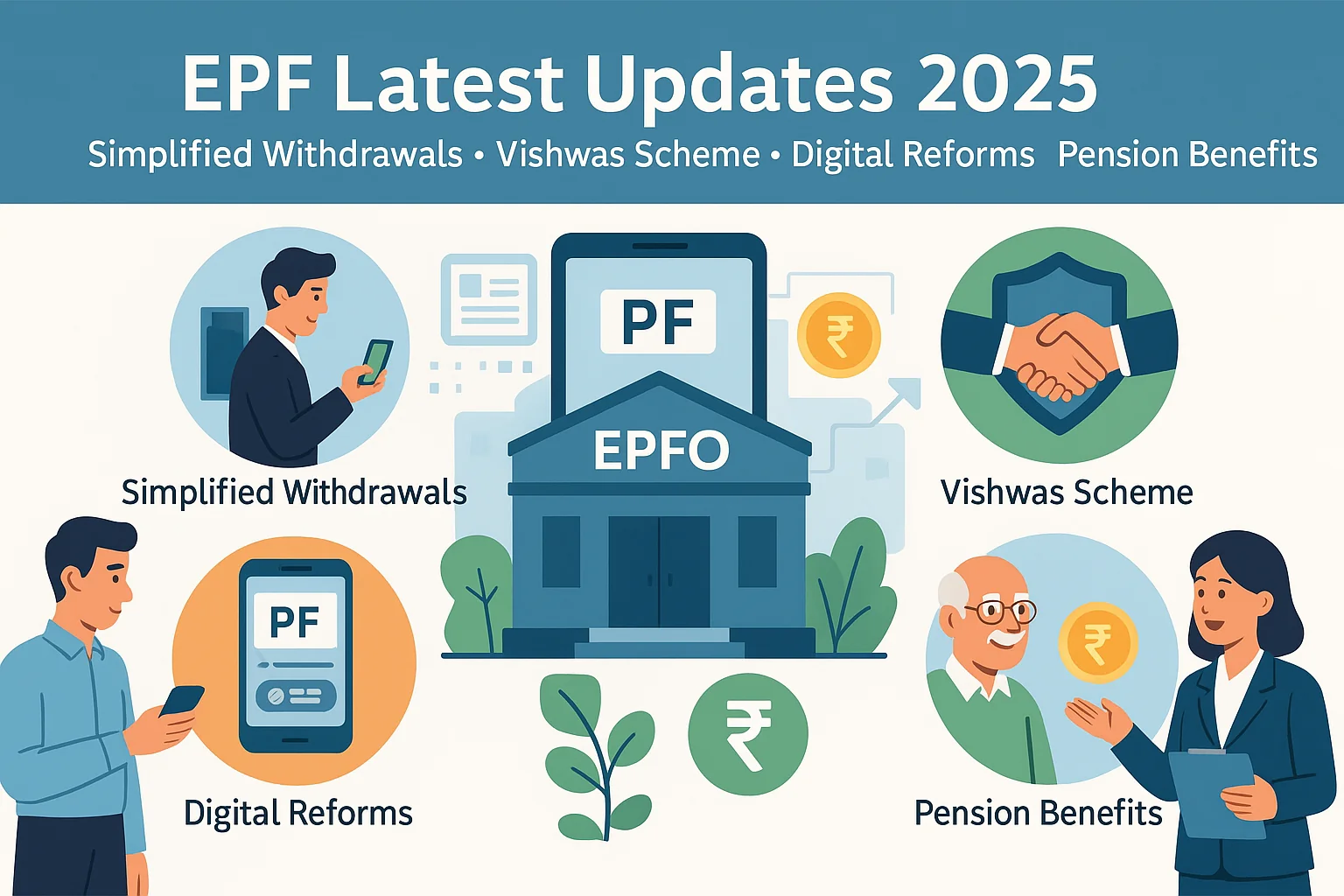

The Employees’ Provident Fund Organisation (EPFO) has announced a series of major reforms in October 2025, marking one of its biggest overhauls in recent years. Chaired by Dr. Mansukh Mandaviya, the Central Board of Trustees (CBT) approved several member-centric initiatives designed to make EPF services faster, simpler, and more transparent.

These include:

- Simplified and liberalized EPF withdrawal rules to make access to funds easier during key life events.

- The “Vishwas Scheme” to reduce long-pending litigations by rationalising penal damages.

- Doorstep Digital Life Certificate (DLC) services for EPS-95 pensioners through India Post Payments Bank (IPPB).

- And a sweeping digital transformation under “EPFO 3.0”, introducing modernized systems, upgraded user management, and faster claim processing.

If you’re an EPF member, pensioner, HR professional, or a family member managing claims after a loved one’s passing, these EPF latest updates 2025 will directly impact how you withdraw money, verify pensions, settle disputes, and track your retirement savings.

In this guide, we’ll break down every change, explain what it means for you, and share Kustodian’s expert insights to help you navigate these reforms with clarity and confidence.

These sweeping changes build on our earlier complete summary of new PF & pension reforms and give you the deeper policy context behind each update.”

EPF Partial Withdrawal Rules Simplified: Easier Access, Higher Limits, and Better Retirement Security

What changed

- EPFO merged 13 complex partial-withdrawal provisions into one streamlined rule grouped into three categories: Essential Needs (illness, education, marriage), Housing Needs, and Special Circumstances.

- Members can now withdraw up to 100% of their eligible PF balance (employee + employer share) for allowed cases.

- Withdrawal limits liberalized: education withdrawals up to 10 times, marriage up to 5 times (previously total 3 combined).

- Minimum service requirement reduced uniformly to 12 months for all partial withdrawals.

- Under Special Circumstances, members no longer need to give reasons (removes cause-based rejections).

- 25% of contributions must be earmarked as Minimum Balance, members must keep 25% in account at all times.

- Goal: Zero documentation and 100% auto settlement for partial withdrawals.

- Period for premature final settlement changed from 2 months to 12 months; final pension withdrawal window changed from 2 months to 36 months.

Impact

- Members get faster, hassle-free access to funds for emergencies or life events, with minimal documentation and a simple 12-month service eligibility.

- 25% minimum balance safeguards retirement corpus while allowing larger early withdrawals, supporting both short-term needs and long-term growth with compounding interest.

- Pension prospects remain protected, ensuring eligibility and retirement value despite more flexible partial withdrawals.

- Zero-documentation auto-settlement cuts claim processing time, reduces errors, and minimizes grievances.

- Employers and HR have reduced verification burden, but must ensure accurate payroll and ECR entries under the new rules.

| Aspect | Old System | New Simplified System (2025) |

| Process | Required multiple documents and employer verification for each withdrawal reason | Simplified, member-centric online process via unified portal |

| Eligibility | Limited to specific pre-defined purposes (e.g. marriage, education, housing) | Broader eligibility — members can withdraw for additional purposes with fewer conditions |

| Withdrawal Approval Time | Often delayed due to manual checks and paper submissions | Faster processing through digital validation and automation |

| Member Convenience | Fragmented and time-consuming | Seamless, single-window experience aimed at ease of access |

| Security of Retirement Corpus | Rigid rules aimed at limiting access | Balanced approach — ensures both liquidity and long-term savings |

Under the new rules, withdrawal is simpler, check our step-by-step EPF withdrawal online process 2025 guide to walk through the updated application flow.

‘Vishwas Scheme’ Launched to Reduce Litigation through Rationalised Penal Damages

What changed

- Vishwas Scheme reduces penal damages for belated remittances to a flat 1% per month, with a graded rate for short defaults: 0.25% for defaults up to 2 months, 0.50% for defaults up to 4 months.

- Scheme covers ongoing and pre-adjudication cases under Section 14B; cases will stand abated on compliance.

- Scheme period: 6 months, extendable by another 6 months.

- As of May 2025, outstanding penal damages were ₹2,406 crores, with over 6,000 cases pending and around 21,000 potential litigation cases in EPFO’s e-proceedings portal.

Impact

- Employers face lower and predictable penalty exposure, with graded, capped rates reducing litigation incentives and encouraging timely regularization of dues.

- Members benefit from faster recovery of pending dues, as employers may prefer compliance over prolonged legal battles, enabling quicker reinvestment and returns.

- The scheme can significantly reduce litigation backlog, lowering administrative costs for EPFO and streamlining dispute resolution.

| Aspect | Earlier Framework | Under Vishwas Scheme (2025) |

| Penalty Structure | High, flat-rate penal damages applied uniformly | Rationalised penalties based on degree of default |

| Employer Incentives | Limited incentive for voluntary compliance | Encourages timely correction by reducing punitive burden |

| Litigation Burden | High volume of disputes and court cases | Simplified and transparent dispute resolution |

| Objective | Recovery-focused | Trust and compliance-focused approach (“Vishwas” = Faith) |

| Expected Impact | Reactive system | Proactive, partnership-based EPFO–Employer relationship |

EPFO-IPPB to Partner to Provide Doorstep Digital Life Certificate (DLC) Services to EPS Pensioners

What changed

- EPFO will sign an MoU with India Post Payments Bank (IPPB) to deliver doorstep Digital Life Certificate (DLC) services.

- Cost: ₹50 per certificate, fully borne by EPFO, free to pensioner.

- Target: Pensioners (especially in rural/remote areas) can submit life certificates from home via IPPB’s postal network, improving CPPS accuracy and enabling quicker pension/family pension processing.

Impact

- Pensioners gain greater convenience and continuity, with no travel or reliance on local offices, especially beneficial for the elderly or those in remote areas.

- Family pensions can be initiated faster, with fewer delays when DLC is completed from home.

- Data accuracy improves, reducing errors under CPPS and lowering the risk of rejected payments or delays from missing life certificates.

| Aspect | Before Partnership | After EPFO–IPPB Integration |

| DLC Submission Mode | Required pensioners to visit banks or CSCs | IPPB postmen will collect DLCs at home |

| Accessibility | Limited for senior citizens and differently-abled pensioners | 100% doorstep availability across India |

| Process Time | Manual verification and submission delays | Real-time digital upload to EPFO servers |

| Reach | Urban and semi-urban concentrated | Expanded to even remote and rural areas |

| Convenience | Moderate | Exceptional — pensioners no longer need to travel |

To understand how EPF (Employee Provident Fund) and EPS (Employee Pension Scheme) rules differ, especially around full withdrawal, see our detailed EPF Pension EPS guide 2025.

EPFO 3.0: CBT Approves Major Digital Transformation to Modernize Provident Fund Services for Members

What changed

- EPFO 3.0: A member-centric digital transformation using a hybrid design - Core Banking Solution + cloud-native, API-first microservices for account management, ERP, compliance and unified customer experience.

- Phased implementation planned for secure, scalable migration enabling faster automated claims, instant withdrawals, multilingual self-service, and payroll-linked contributions.

Impact

- Members benefit from faster, reliable, multilingual self-service, with quicker automated claims and accurate contribution updates.

- Employers and payroll vendors gain closer payroll-EPFO integration, with improved real-time checks and fewer rejections.

- Service reliability and scalability improve via cloud/API infrastructure, supporting 30+ crore members and faster feature rollouts.

Re-Engineered EPFO Modules and Upgraded Digital Systems for Faster, Transparent Operations

What changed

- Return filing module (ECR): Simplified four-step process - upload ECR, validate/approve, generate challan, make payments. Automated validations and real-time checks introduced.

- User management module: Better security, intuitive UI, facility to create new EPFO offices via system (district-level office formation) and improved mapping of establishments.

- e-Office upgraded from v6 to v7: Better workflow automation, document handling for service cases (pension on higher wages, profile corrections).

- SPARROW implemented for paperless APAR management.

Impact

- Employers benefit from a simpler ECR process with built-in corrections, reducing repeated submissions, rejections, and administrative burden.

- Members enjoy more accurate and timely PF and pension credits, minimizing missing or mismatched entries and speeding up grievance resolution.

- Internal efficiency improves through better office formation and modernized workflows, accelerating service delivery and case processing.

Practical checklist - what members, pensioners and employers should do now

For EPF members (employees)

- Verify UAN details and passbook entries today.

- Track employer ECR uploads monthly - raise a grievance early if entries mismatch.

- Plan partial withdrawals responsibly - remember the 25% minimum balance to preserve retirement corpus.

- If you have pending dues cases under 14B, check if those can be regularized under Vishwas.

For EPS-95 pensioners

- Maintain updated contact and address for IPPB/EPFO outreach.

- Expect DLC doorstep options; prepare ID/documents as requested when service starts.

For employers & HR teams

- Audit ECR processes - adopt the new four-step workflow practices to minimise rejections.

- Review outstanding penal damage exposures and evaluate Vishwas compliance to close long-running liabilities.

- Keep employee data accurate to enable automated settlements.

Before initiating any withdrawal, validate your EPF data, see our EPF balance check 2025 guide for a clear walkthrough to check your balance via UAN, passbook, and UMANG app.

Kustodian’s Expert Analysis

The October 2025 EPFO reforms bring unprecedented convenience for members, but also introduce nuances that require careful attention. Here’s what you need to know:

- Partial Withdrawals:

Simplified partial withdrawal rules are expected to trigger a surge in requests, as members access new categories like education, housing, and special needs. While 100% of the eligible balance can now be withdrawn, the 25% minimum balance safeguards a retirement cushion.

However, easing partial withdrawals while extending conditions for full withdrawals could create challenges. Since demographic and EPS eligibility checks apply only to full withdrawals, the longer waiting period after leaving an employer may make accessing full support more difficult.

2. Impact of Extended Full Withdrawal Timelines:

The extension of full EPF withdrawal timelines from 2 months to 12 months is a double-edged sword:

- On the positive side, it may encourage members to retain their UAN, continue contributions, and reduce unnecessary PF account closures.

- However, differentiating timelines for full EPF and full EPS withdrawals could create confusion for members.

- For those moving abroad, the longer waiting period may make full withdrawals cumbersome and time-consuming.

- Aspiring entrepreneurs or members planning startups may face delays in accessing PF capital, potentially impacting initiatives like the Startup India mission.

- Finally, adding more conditions for full withdrawals, while easing partial withdrawals could increase friction due to demographic checks and EPS eligibility requirements, making careful planning essential for members after leaving their employer.

3. Data Accuracy Is Critical:

Auto-settlement and instant withdrawals hinge on accurate member and employer data. Mismatches in UAN details, passbook entries, or ECR filings can still block automated settlements. Members should verify their personal records, and employers must ensure clean, validated ECR uploads.

4. Vishwas Scheme – Practical Litigation Relief:

The scheme’s 1% per month penal damages reduces the incentive for litigation, offering a pragmatic path to resolve long-pending disputes. Employers should assess open 14B exposures and compare compliance costs versus ongoing litigation. Members with pending dues should track case eligibility and timelines carefully.

5. Doorstep Digital Life Certificate (DLC):

EPFO-IPPB doorstep DLC services eliminate a major barrier for pensioners, particularly in rural areas. With EPFO bearing the ₹50 service cost, pensioners can submit life certificates from home, reducing the risk of pension discontinuity.

6. EPFO 3.0 and Digital Modules:

The hybrid Core Banking + API-first system enables faster claims, instant withdrawals, and multilingual self-service. The re-engineered return filing and user management modules reduce errors and friction, but successful implementation depends on data hygiene, demographic accuracy, and clean ECR/Payroll integration.

In Kustodian’s view, these reforms are transformative, but nuanced. While partial withdrawals have become more flexible, the extended full withdrawal timeline introduces new challenges, particularly for international movers, entrepreneurs, and members with complex EPS eligibility. Proactive monitoring of passbooks, UAN, and case status remains crucial to fully benefit from these change

Frequently Asked Questions (FAQs)

1) Has the minimum service requirement for EPF partial withdrawals changed?

Yes. The minimum service requirement is now reduced to 12 months for all partial withdrawals. Earlier, this varied across categories, now it’s uniform and member-friendly, allowing faster access to funds when needed.

2) What are the new simplified partial withdrawal categories under EPFO?

The revised rules merge older, confusing categories into three simplified heads

- Essential Needs (e.g., medical emergencies, education, marriage)

- Housing (purchase, construction, or loan repayment)

- Special Circumstances (natural calamity, disability, unemployment, etc.)This simplification ensures faster claim approvals and fewer rejections.

3) What is the 25% Minimum Balance retention rule in EPF withdrawals?

Even though 100% of the eligible balance can be considered for withdrawal, EPFO will now retain at least 25% of the total PF corpus in your account. This ensures continued membership, compounding of interest (currently 8.25%), and future security.

4) What is the Vishwas Scheme and who benefits from it?

The Vishwas Scheme 2025 is a one-time litigation resolution and penalty reduction initiative for employers. It lowers penal damages under Section 14B to 1% per month, with even lower slabs for short delays. This helps employers settle old dues amicably and allows employees’ PF contributions to be credited faster.

5) What is EPFO 3.0 and how will it benefit members?

EPFO 3.0 is a comprehensive digital modernization initiative that integrates core banking, AI-powered claim processing, and multilingual self-service portals. Members can expect:

- Real-time claim tracking

- Faster withdrawals and transfers

- Improved payroll integration for employers

- Enhanced grievance redressal implementation will be phased, with early rollouts expected in 2026.

6) Will EPFO 3.0 make PF withdrawals instant like a bank transfer?

Yes, that’s the long-term goal. Under EPFO 3.0’s hybrid Core Banking + Cloud API architecture, verified claims will be processed instantly or within 24 hours, compared to the current 3–10 day window.

7) What is the new doorstep Digital Life Certificate (DLC) service for pensioners?EPFO, in partnership with India Post Payments Bank (IPPB), will now offer doorstep DLC verification for all pensioners. A postman will visit, verify identity biometrically, and upload the certificate digitally.

8) Who will benefit the most from these EPFO 2025 reforms?

- Employees: Simplified withdrawals, faster claim settlements

- Employers: Reduced penalties and litigation via Vishwas Scheme

- Pensioners: Free doorstep DLC services

- Families of deceased members: Easier documentation and faster claim processing under EPFO 3.0

Conclusion

The reforms approved by the Central Board of Trustees mark a major leap forward in how India’s workforce engages with the EPF system. With simpler withdrawal rules, faster digital verification, doorstep pension services, and reduced litigation through the Vishwas Scheme, the focus has clearly shifted toward empowering members, retirees, and families with transparency and convenience.

Whether you’re managing your own EPF, assisting an elderly parent with their pension, or helping a family navigate claims after a loss - understanding these changes today can save you weeks or even months of delays later.

At Kustodian.life, our mission is to simplify your EPF, Pension, and inheritance processes, so you can focus on what truly matters.

Schedule a quick call with our experts to get guidance on your EPF withdrawals, claim status, or any of the new 2025 rule changes. Let’s make sure your hard-earned savings are always within your reach.