For most salaried professionals in India, the Employee Provident Fund (EPF) is not just a salary deduction it is your long-term financial safety net. So when you log into the EPFO portal and don’t see updated interest, or hear that your account has become “inoperative,” it can instantly trigger panic.

Is my PF still earning interest?

Has my account stopped growing?

Is my money stuck?

This 2026 guide removes the confusion completely. You’ll learn how PF interest actually works, when it gets credited, and whether an inoperative PF account continues earning based on current EPFO rules. By the end of this page, you’ll know exactly where you stand.

Compliance Note: EPF interest credit and inoperative account treatment depend on rules notified by EPFO, annual government decisions, and account activity status. Actual credit visibility may differ from declaration timelines.

Contents

- Is My PF Still Earning Interest?

- How EPF Interest Works

- When Does EPF Interest Get Credited?

- Why EPF Interest May Not Be Visible Yet

- What Is an Inoperative PF Account?

- Does an Inoperative PF Account Earn Interest?

- EPF Interest Rate: What You Should Know

- EPF Interest Rate: What You Should Know

- Common Myths About EPF Interest & Inoperative Accounts

- Conclusion: Your Hard-Earned Money is Secure

- FAQs

1. Is My PF Still Earning Interest?

If your passbook hasn’t changed in months, it does NOT automatically mean your interest has stopped. In most cases, the issue is timing, not loss. Common anxieties usually fall into three categories:

- My PF interest hasn’t updated: You see the contributions from your employer, but the interest row is missing for the current financial year.

- I left my job, will interest stop? There is a widespread fear that the moment you stop contributing, the money becomes "dead" and stops growing.

- Is my PF account inactive now? Many fear that a few months of unemployment will lead to the EPFO "freezing" their hard-earned savings.

If your account has not received contributions for months, understand how old PF accounts and transfers work before taking action.

The Core Reassurance:

EPF interest and inactivity follow strictly defined rules. In the vast majority of cases, your fears stem from timing gaps in the EPFO’s massive digital infrastructure, not a loss of money. Your funds are managed under the statutory framework of the EPF Act, 1952, under the supervision of the Ministry of Labour and Employment.

2. How EPF Interest Works

To understand your passbook, you first need to understand the "Mental Model" of EPFO’s accounting. Many people assume PF interest works like a standard savings account where you see a tiny credit every month. That is not the case here.

- Declared Annually: The pf interest rate is not static. It is reviewed and declared by the government for every financial year (April to March).

- Calculated Monthly: While you see the credit once a year, the calculation happens on the monthly running balance.

- The Single Entry: The EPFO aggregates these monthly calculations and posts them as a single consolidated entry at the end of the financial year.

- Processing Delays: Even after the year ends, it takes time for the EPFO software to update millions of accounts. If you don't see the interest on April 1st, it doesn't mean it wasn't earned; it just hasn't been "pushed" to your digital view yet.

3. When Does EPF Interest Get Credited?

This is the most searched query for a reason. Everyone wants to know the epf interest credit date. However, unlike a salary date, there is no fixed day on the calendar. Instead, there is a three-step cycle:

- Declaration: The Ministry of Labour and Employment, in consultation with the Finance Ministry, declares the rate.

- Calculation: Once the rate is official, the EPFO back-end systems calculate the specific interest for every member based on their monthly contributions.

- Reflection: The interest finally reflects in your passbook. This happens in batches.

When epf interest will be credited depends heavily on your specific PF office and your employer's compliance. It is common for one person to see their interest in August while another sees it in December for the same financial year.

4. Why EPF Interest May Not Be Visible Yet

If the government has announced the rate but your passbook is silent, don't panic. Here is why the lag happens:

- Employer ECR Delays: If your employer is late in filing their Electronic Challan-cum-Return (ECR), it can stall the interest processing for that specific establishment.

- EPFO Backend Reconciliation: Processing data for over 6 crore members is a monumental task. The systems often prioritize active accounts or specific regions first.

- Passbook Sync Lag: Sometimes the main database is updated, but the "Member Passbook" portal (the interface you see) takes a few extra weeks to sync.

- Job Change / Transfer: If you are in the middle of transferring funds from an old UAN or member ID to a new one, the interest might be credited to the old ID first before moving over.

Reassurance: Once the annual interest rate is notified and applied, eligible balances earn interest even if the passbook reflection is delayed . You are not losing out on "interest-on-interest" because the value is backdated to the start of the fiscal year once credited.

If employer delays are frequent, you may also want to review common EPF portal login and compliance issues.

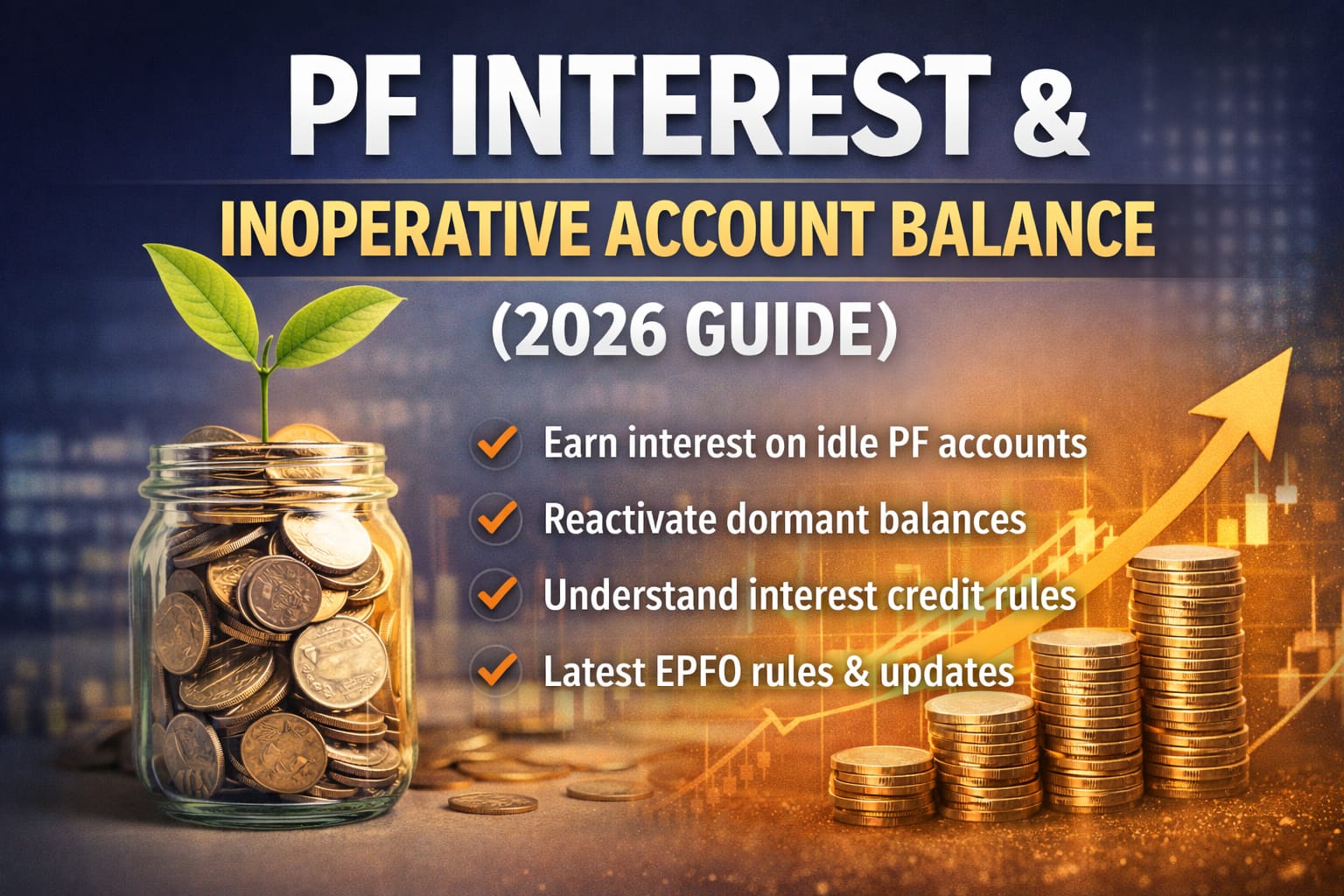

5. What Is an Inoperative PF Account?

The term "inoperative" sounds scary, like a bank account that has been shut down. Let’s clarify: Inoperative does not mean closed.

An inoperative pf account is a classification used by the EPFO for accounts that have not received a contribution for a prolonged period (typically 36 months) and where no withdrawal application has been made.

Crucially, the account still exists. The money is still yours. It is simply moved into a category where the EPFO monitors it differently to prevent fraud and encourage members to either withdraw or merge the balance with their current active account.

6. Does an Inoperative PF Account Earn Interest?

Short Answer: Yes, in most cases, EPF balances continue earning interest even if the account becomes inoperative until the member turns 58.

This is the "Central Confusion" of the EPF system. If you search online, you will find conflicting answers because the rules have changed over the years. Currently, the rule generally follows this logic:

- Active Interest: For most employees, even if you stop working, as per current EPFO policy, interest is generally credited on inoperative accounts until the member attains 58 years of age, subject to prevailing rules.

- The Cut-off: Once a member reaches 58 years of age, the account must be settled. If it is not settled, it becomes truly inoperative and stops earning interest after that point.

- Historical Context: Between 2011 and 2016, there was a period where interest was stopped on inactive accounts to encourage transfers. However, current policy is much more worker-friendly, ensuring your money grows even during career breaks.

The Bottom Line: Even in rare scenarios where interest might stop (post-retirement age), as per current EPFO policy, interest is generally credited on inoperative accounts until the member attains 58 years of age, subject to prevailing rules.

If you are nearing retirement age, review how to start your monthly pension correctly using Form 10D.

7. Old PF Accounts vs. Inoperative Accounts

Old PF accounts are not automatically inoperative. An account becomes inoperative only when there are no contributions for a prolonged period and no withdrawal claim is filed.

- Old PF Account: This is an account from a previous employer that you haven't transferred to your current UAN. It is "inactive" in terms of new contributions but is usually not inoperative. It continues to earn interest at the prevailing pf interest rate.

- Inoperative PF Account: This is an account that has been left untouched for years, often where the member has moved abroad or left the organized workforce entirely without settling the account.

Many people assume their "Old PF" has stopped earning money. In reality, as long as you haven't hit the retirement age, that old balance is likely still compounding year after year.

Online EPF Transfer Process: How to Fill Form 13

8. EPF Interest Rate: What You Should Know

The epf interest rate is historically competitive among fixed-income social security schemes in India. While we aren't looking at specific tables today, it is important to know how it is governed:

- Policy-Driven: The rate is determined based on the earnings of the EPFO's investments (mostly in government bonds and a small portion in ETFs/Equity).

- Uniform Application: The rate is applied uniformly to all members, regardless of whether you are a high-earner or a low-earner.

- Compounding: Because the interest is credited annually but calculated monthly, the "power of compounding" works heavily in your favor over a 20-30 year career.

Check the Free EPF Interest Calculator

9. Common Myths About EPF Interest & Inoperative Accounts

To build true assurance, we must deconstruct the myths that circulate in office breakrooms:

- Myth 1: "PF stops earning interest the day you resign."

- Myth 2: "Inoperative PF money goes to the Government."

- Myth 3: "Interest is credited monthly."

- Myth 4: "Inactive accounts face a penalty."

10. Conclusion: Your Hard-Earned Money is Secure

Navigating the complexities of the epf interest system can feel daunting, especially when digital passbooks don’t update as quickly as we’d like. However, the key takeaway is that the EPFO framework is designed to protect the worker. Whether you are currently employed, between jobs, or sitting on an inoperative pf account, your principal remains shielded by sovereign guarantee.

The pf interest rate continues to be one of the most competitive savings tools in India, and while the epf interest credit date remains a moving target each year, the "missing" entries are almost always a matter of administrative timing rather than financial loss.

By understanding that an inoperative pf account balance is not "lost" but merely "dormant," you can make informed decisions about your financial future. Whether that means consolidating your accounts or letting your retirement corpus grow undisturbed.

Stay patient with the portal, keep your KYC updated, and remember that your retirement nest egg is working for you, even when you aren't looking at the screen.

11. FAQs

When Does EPF Interest Get Credited?

There is no single fixed calendar date for EPF interest credit. Every financial year, the interest rate is first recommended by the Central Board of Trustees and then officially notified by the Government of India. Only after this formal notification does the interest calculation and batch crediting process begin.

In most cases, members start seeing the credited interest reflected in their passbooks a few months after the financial year ends (typically between June and September). However, the exact timing can vary depending on backend processing and system updates.

Even if the entry is not visible immediately in your passbook, interest is calculated internally on your monthly running balance and credited for the full financial year once processed.

Why Is My PF Interest Not Updated?

If your passbook does not show updated interest, it usually does not mean that interest has stopped accruing.

Common reasons include:

- Ongoing batch processing by the Employees' Provident Fund Organisation

- Delay in official interest rate notification

- Employer’s pending ECR (Electronic Challan-cum-Return) filing

- Temporary lag in the EPFO passbook portal synchronization

The EPFO credits interest in bulk after completing internal reconciliation. During this period, the passbook may not immediately display the updated figures.

Rest assured: interest continues to accrue in the background based on the declared annual rate. A delay in display does not mean a loss of interest.

Does PF Earn Interest After Leaving a Job?

Yes. Your EPF balance continues to earn interest even after you leave your job, provided:

- You have not withdrawn the funds

- You have not reached the retirement age of 58

- The account remains active in the EPFO system

Earlier rules had restrictions on interest credit for inactive accounts, but currently, EPF balances continue to earn interest until the member reaches 58 years of age.

This ensures that employees who switch jobs or take career breaks do not lose growth on their retirement savings.

What Happens If a PF Account Becomes Inoperative?

A PF account is marked as “inoperative” if there are no contributions for a prolonged period and no withdrawal claim has been filed.

When this happens:

- The account remains securely recorded in the EPFO database

- Funds are not forfeited

- Interest may continue as per prevailing rules

- Additional KYC verification may be required during withdrawal or transfer

Inoperative status mainly affects administrative processing — not ownership or safety of funds.

Is Money Safe in an Inoperative PF Account?

Absolutely. Your EPF balance is protected under statutory law and governed by the Employees' Provident Fund Organisation under the EPF & MP Act.

Even if the account is marked inoperative:

- The funds remain legally yours

- They are not confiscated

- They remain part of your retirement corpus

- Withdrawal or transfer can be processed after proper verification

The EPF system is a government-backed statutory framework, and member funds are safeguarded under regulatory oversight.

How Kustodian Helps You Reclaim Control

While the EPFO acts as the legal guardian of your funds, navigating their digital "maze" can still be overwhelming. This is where Kustodian steps in. Think of them as your personal advocate for resolving stuck EPF issues.

- Free EPF Audit: Kustodian offers an AI-powered scan that detects hidden issues—like KYC mismatches, incorrect exit dates, or service overlaps—before they lead to a claim rejection.

- Resolution, Not Just Advice: They don’t just tell you what’s wrong; they handle the heavy lifting—from filing Joint Declarations to coordinating with previous employers and following up with the EPFO office.

- Zero-Risk Success Guarantee: Operating on a success-based model, Kustodian ensures you only pay for results. If they can’t resolve your issue, you get a full refund.

Empathy-First Support: Born from a founder's personal struggle with the system, the platform is designed to turn a stressful 100-hour bureaucratic battle into a simple, 2-hour guided experience.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.