2025 introduced faster EPF withdrawals, auto-settlement up to ₹5 lakh, centralised pension payments, and major backend clean-ups. In 2026, EPFO is expected to move toward ATM-based withdrawals, UPI integration, unified social security dashboards, and expanded coverage under the Social Security Code.

If you have logged into your EPF portal recently, you might have noticed things feel... different.

Introduction

For decades, dealing with the Employees' Provident Fund (EPFO) felt like wrestling with a giant, sleepy elephant. Paperwork got lost, transfer claims vanished into the void, and "technical rejection" was a phrase that haunted our dreams. If you changed jobs, you practically had to beg your previous HR for data. If you needed money for an emergency, you prepared yourself for a 20-day wait.

But 2025 was a turning point.

It wasn’t just about new rules; it was about the system finally coming to life. We moved from manual approvals to AI-based clearances, and from "wait 20 days" to "settled in 3 days."

As we stand on the edge of 2026, the landscape is shifting again from digitisation to integration. The government is preparing to roll out the massive Social Security Code, which promises to unify your entire financial life.

Whether you are an employee trying to withdraw funds, a job-switcher facing transfer errors, or a pensioner looking for stability, this is your definitive guide to what was done in 2025 and the massive changes coming your way in 2026.

Contents

- Quick Reference: 2025 vs. 2026 At a GlanceThe 2025 Report Card (What Actually Changed?)

- Part 2: How to Use the New 2025 Features (Step-by-Step)

- Part 3: 2026 and Beyond (Integration & The Future)

- FAQs

- Conclusion: The Elephant is Dancing

Quick Reference: 2025 vs. 2026 At a Glance

| Feature | The Old Way (Pre-2025) | The 2025 Reality | The 2026 Future (Projected) |

| Unemployment Withdrawal | 100% after 2 months' wait | 75% after 1 month (Immediate relief) | Instant ATM Withdrawal (Projected) |

| Full Final Settlement | Allowed after 2 months | 12-Month Wait (Mandatory) | Integrated with "One Nation, One Passbook" |

| Pension (EPS) Withdrawal | Allowed after 2 months | Locked for 36 Months | Unified Pension Interface |

| Claim Speed | 15–20 Days | < 3 Days (Auto-Mode) | Real-Time via UPI (EPFO 3.0) |

| Service History | Hard to find (RTI) | Downloadable Annexure K | Auto-Credit of Service Years |

| Medical Claims | Upload bills | AI Pre-Screening (No bills < ₹1L) | ABHA Health ID Integration |

| Claim Limit (Auto) | ₹1 Lakh | ₹5 Lakhs | Dynamic Limits based on Service |

| Ecosystem | Siloed (EPF only) | Employee Enrollment Campaign | Merged (EPF + NPS + ESIC) |

The 2025 Report Card (What Actually Changed?)

2025 was the year of "The Cleanup." The EPFO focused heavily on fixing the backend pipes that caused so much user frustration. Here are the 7 major shifts that defined the year.

This section explains *what changed* at a system level. For form-specific instructions or claim-filing steps, we link to dedicated guides at the relevant points below.

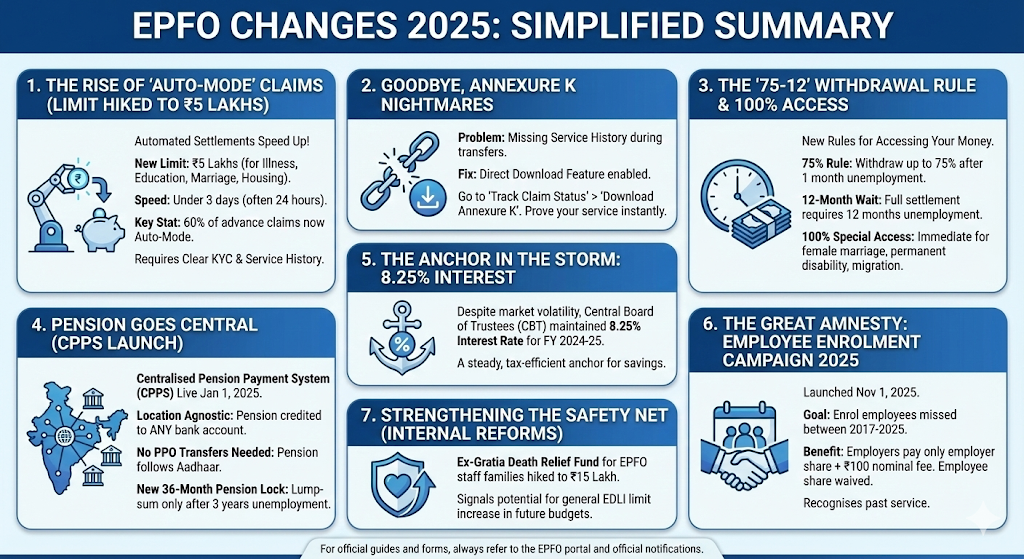

1. The Rise of "Auto-Mode" Claims (Limit Hiked to ₹5 Lakhs)

The biggest win of 2025 was the massive expansion of automated claim settlements.

In the past, every single claim, whether for ₹5,000 or ₹5 Lakhs, had to be opened, read, and approved by a human PF officer. This bottleneck caused delays, especially during holidays or strike periods.

What Changed in 2025:

The EPFO introduced an AI-based pre-screening mechanism. Now, if your KYC is clean (Aadhaar validated) and your request falls under specific categories, a computer approves it instantly.

- The New Limit: The limit for auto-settlement was hiked from ₹1 Lakh to ₹5 Lakhs for illness, education, marriage, and housing.

- The Speed: Claims that used to take 10–15 days are now often settling in less than 3 days (sometimes even 24 hours).

- The Stat: By mid-2025, nearly 60% of all advance claims were being settled by the auto-mode system.

Pro Tip: To trigger auto-mode, ensure your bank cheque image is clear, and your Service History has no gaps. AI rejects claims if the "Cancelled Cheque" doesn't have the name printed or if there is a "Service Gap" of more than 180 days.

To understand which claim types qualify for auto-settlement and how to file them correctly, see our EPF Form 31 (PF Advance) and EPF Form 19 (Final Settlement) guides.

2. Goodbye, Annexure K Nightmares

💨How to Download Annexure K (Service History) Without HR

For years, "Annexure K" was the villain in the story of job switching.

When you transfer your PF from Company A to Company B, the money usually moves.

But your Service History (the record of how many years you worked) serves as the "Annexure K." Often, this document wouldn't transfer. You would see the money in your new passbook, but your "Pension Service" would show zero.

Fix:

In late 2025, the EPFO finally enabled a Direct Download feature.

- You no longer have to file an RTI or beg your previous employer to send this document.

- You can now go to Online Services > Track Claim Status and find a "Download Annexure K" button for completed transfers.

- This puts the power back in your hands to prove your service history for pension eligibility.If your service years are still missing or pension eligibility looks incorrect, our Fixing EPS Errors guide explains how to correct Annexure K, DOJ/DOE, and pension service gaps.

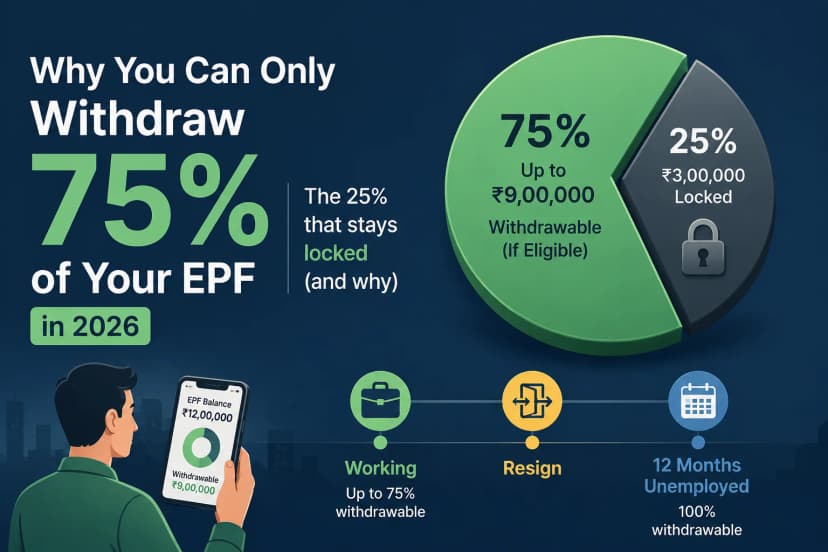

3. The "75-12" Withdrawal Rule & 100% Access

In 2025, the government changed how you can access your money.

- The 75% Rule (Immediate Relief): If you lose your job, you can now withdraw up to 75% of your total fund (Employee + Employer Share) after just 1 month of unemployment. File your 75% withdrawal claim here.

- The 2-Month Wait (Full Settlement): To withdraw the remaining 25% (Full Final Settlement), you must now wait for 2 months of unemployment. This prevents people from emptying their retirement savings during short career breaks.

4. Pension Goes Central (CPPS Launch)

For our retired friends and parents, the Centralised Pension Payment System (CPPS) went live on January 1, 2025.

The Old Problem:

Pensioners were tethered to specific bank branches. If a pensioner moved from Delhi to Chennai to live with their children, they had to physically transfer their PPO (Pension Payment Order) from one bank branch to another. It was a bureaucratic nightmare.

The 2025 Solution:

The new CPPS system uses the National Payments Corporation of India (NPCI) rails.

- Location Agnostic: Pension can now be credited to any bank account in India.

- No Transfers Needed: You can move cities, change banks, or change branches without notifying the EPFO. Your pension follows your Aadhaar, not your branch code.

The "36-Month" Pension Lock

While the EPF withdrawal timeline was extended to 12 months, the EPS (Pension) withdrawal rules were tightened even further. To encourage long-term pension continuity, you can now withdraw your lump-sum pension corpus only after 36 months of unemployment (previously 2 months). If you join a new job within 3 years, your pension service continues automatically.

5. The Anchor in the Storm: 8.25% Interest

Despite global market volatility and inflation fluctuations, the Central Board of Trustees (CBT) maintained the interest rate at 8.25% for FY 2024-25.

While this might seem like a small detail, in a financial world where fixed deposit rates fluctuate wildly, the EPF remained a steady, tax-efficient anchor for millions of salaried Indians.

6. The Great Amnesty: Employee Enrolment Campaign 2025

Launched on Nov 1, 2025, this campaign is a massive "Come Clean" scheme for employers.

- The Goal: To enrol employees who were previously left out of the PF net between 2017 and 2025.

- The Benefit: Employers can enrol missing staff by paying only the employer’s share (employee share is waived) and a nominal damage fee of ₹100. This is a golden window for workers to get their past service recognised legally.

7. Strengthening the Safety Net (Internal Reforms)

The EPFO also strengthened its own internal welfare. The Ex-Gratia Death Relief Fund for families of deceased EPFO employees was hiked from ₹8.8 Lakh to ₹15 Lakh. While this specific hike is for staff, it signals a broader intent to adjust social security benefits against inflation, sparking hope for a similar hike in the general EDLI limits (currently ₹7 Lakhs) in the 2026 budget.

Part 2: How to Use the New 2025 Features (Step-by-Step)

Reading about changes is good; using them is better. Here is how to navigate the new system.

How to Download Annexure K (The "Missing Link")

If you have transferred PF recently, do this immediately to save a copy of your service history.

- Log in to the Unified Member Portal.

- Go to Online Services > Track Claim Status.

- Look for your Transfer Claim (Form 13) in the list.

- If the status is "Settled," you will see a Download Annexure K icon next to it.

- Save this PDF. It is your only proof of pensionable service if the digital data gets corrupted later.

How to Ensure Your Claim Hits "Auto-Mode"

Don't let your emergency fund get stuck in the "Manual Review" pile.

- Bank KYC: Ensure your bank account is seeded with Aadhaar, and the IFSC code is correct.

- Cheque Clarity: When uploading your cheque/passbook image, ensure your Name and Account Number are printed and clearly visible. AI cannot read handwritten names.

- Select the Right Para: For the fastest approval, select "Illness" (Para 68J). It has the highest auto-approval rate and doesn't require uploading medical bills for lower amounts.For a complete claim-filing walkthrough with screenshots, see our EPF Withdrawal Process step-by-step guide.

Part 3: 2026 and Beyond (Integration & The Future)

If 2025 was about fixing the plumbing, 2026 is about building a whole new house.

As we look deeper into 2026, the boundaries between different social security nets are blurring. The government is pushing for the full implementation of the "Social Security Code."

What does this mean for you?

We are moving toward a system where your EPF, EPS (Pension), and potentially your health insurance benefits (ESIC) are viewable under a single digital umbrella.

1. EPFO 3.0: The "ATM" Experience

The most futuristic change coming in 2026 is the EPFO 3.0 Tech Overhaul.

- ATM Withdrawals: The government is testing special "EPF Cards" that will allow you to withdraw small emergency amounts (e.g., up to ₹1 Lakh) directly from an ATM, just like a debit card.

- UPI Integration: Soon, you might be able to liquidate a portion of your PF directly to your bank account via UPI apps, bypassing the portal entirely for small claims.

2. The "Super-App" Integration

Imagine logging into one app and seeing your PF balance, your Pension history, your Health Insurance (ESIC) validity, and your National Pension System (NPS) returns all in one dashboard.

- NPS Integration: Discussions are ongoing about allowing a one-time transfer from EPF to NPS for those who want market-linked returns. This would be a game-changer for aggressive investors who find the 8.25% EPF rate too conservative.

For current medical advance rules and eligibility, refer to our EPF Form 31 (PF Advance) guide.

3. The Wage Ceiling Debate (₹15,000 > ₹25,000?)

The rumour mill for 2026 is loud regarding the Wage Ceiling Hike.

Currently, EPF is mandatory only for salaries up to ₹15,000 (Basic + DA). This limit hasn't changed since 2014.

- The Proposal: There is a strong push to raise this limit to ₹21,000 or ₹25,000.

- The Impact: If this happens in 2026, millions of employees who were previously "excluded" or "optional" will fall under the mandatory EPF net. While this reduces your in-hand salary slightly (due to the 12% deduction), it massively boosts your long-term forced savings and pension safety net.

4. Social Security for the Gig Economy

2026 might be the year the Gig Worker finally gets a seat at the table.

Under the new Social Security Code, platforms (like Zomato, Swiggy, Uber) may be required to contribute a percentage of their revenue into a social security fund. This could open up a "Mini-EPF" structure for freelancers and gig workers who currently have zero protection.

Useful Links & Official Resources

EPFO Official Portals

- EPFO Unified Member Portal (UAN Login)https://unifiedportal-mem.epfindia.gov.in/memberinterface/Log in using your UAN to apply for withdrawals, track claims, download Annexure K, update KYC details, and view service history.

- EPFO Official Websitehttps://www.epfindia.gov.inThe primary source for EPF circulars, scheme rules, interest rate announcements, and official policy updates.

- EPFO Passbook Portalhttps://passbook.epfindia.gov.inCheck your PF contributions, employer deposits, and updated balance before initiating transfers or withdrawals.

- UMANG App – EPFO Serviceshttps://web.umang.gov.inAccess EPF services through a mobile interface including passbook viewing, claim submission, and claim tracking.

Pension and Scheme Documents

- Employees’ Pension Scheme (EPS-95) Guidelineshttps://www.epfindia.gov.in/site_docs/PDFs/Schemes/EPS95_update.pdfOfficial documentation explaining pension eligibility, service calculation rules, and withdrawal provisions.

- EPF Claim Forms (Form 19, 31, 10C, 13, 10D)https://www.epfindia.gov.in/site_en/Forms.phpDownload official claim forms for PF withdrawal, pension claims, advances, and account transfers.

EPF Claim Tracking & Support

- EPFO Grievance Portal (EPFiGMS)https://epfigms.gov.inRaise complaints for delayed claims, missing service records, employer approval issues, or incorrect EPF data.

- EPFO Regional Office Directoryhttps://www.epfindia.gov.in/site_en/Contact_us.phpFind the nearest EPFO office for offline claim submissions or assistance.

Identity & Verification Services

- Aadhaar Services Portal (UIDAI)https://uidai.gov.inVerify or update Aadhaar details used for EPF KYC authentication.

- Income Tax Department – PAN Serviceshttps://www.incometax.gov.inVerify PAN and manage tax compliance related to PF withdrawals and interest income.

FAQs

1. Can I withdraw 75% of my EPF balance after 1 month of unemployment in 2026?

Yes. Under the revised EPF withdrawal rules, members can withdraw up to 75% of their total EPF balance after completing 1 month of unemployment. The remaining balance can be withdrawn after 2 months of unemployment, subject to eligibility conditions and proper KYC verification.

2. What is the new auto-settlement limit for EPF claims?

In 2025, the EPFO increased the auto-settlement limit for eligible advance claims from ₹1 lakh to ₹5 lakhs. If your KYC details are verified and your claim falls under eligible categories such as illness, marriage, education, or housing, it may be processed in auto-mode within a few days.

3. What is the Centralised Pension Payment System (CPPS)?

The Centralised Pension Payment System (CPPS), launched in 2025, allows EPS pensioners to receive their pension in any bank account across India without transferring their Pension Payment Order between bank branches. Pension is credited based on Aadhaar-linked banking details, making the system location-independent.

4. How can I download Annexure K after a PF transfer?

After your PF transfer (Form 13) is marked as “Settled,” log in to the EPFO Unified Member Portal. Go to “Online Services” → “Track Claim Status,” and download Annexure K from the completed transfer record. This document contains your service history and is important for pension eligibility verification.

5. Is EPF ATM withdrawal or UPI integration available in 2026?

As of 2026, ATM-based EPF withdrawals and UPI integration are proposed or under pilot discussion but have not been fully implemented nationwide. Members should continue using the EPFO portal for official withdrawal processes unless formal rollout notifications are issued.

6. Has the EPF wage ceiling been increased above ₹15,000?

As of 2026, the statutory wage ceiling for mandatory EPF coverage remains ₹15,000 per month (Basic + DA). While proposals to increase it to ₹21,000 or ₹25,000 have been discussed, no official notification has been issued yet.

Conclusion: The Elephant is Dancing

The era of rushing to the PF office with bulky files, chasing signatures, or slipping a bribe to get work done is fading away.2025 proved that the EPFO can be efficient.2026 is shaping up to prove that it can also be fully unified.

The EPFO is transforming from a slow, opaque “black box” into a transparent, digital-first financial partner. But this new convenience comes with one clear expectation: compliance. The system is faster than ever, but it is also far more precise. It rewards those whose records are accurate and up to date and automatically flags anyone with incomplete KYC, mismatched data, or irregular service history.

Your role is simple: Keep your KYC updated. Maintain a clean, accurate employment record. Avoid discrepancies. Do that, and the digital ecosystem will work smoothly in your favour.

Here’s to smarter systems, smoother processes, and wiser savings.

Happy saving!

Disclaimer: This guide is for educational purposes and based on the rules applicable in 2026. EPF rules are subject to change by the government. For specific legal or financial advice, consult a professional.