Discover all EPFO rule changes in 2026, auto PF transfers, faster withdrawals, digital claims, and updated pension reforms. Essential guide for every EPF account holder in India.

If you're a salaried employee in India or helping a loved one manage their EPF account, you’ll want to pay attention to what’s changed in 2026.

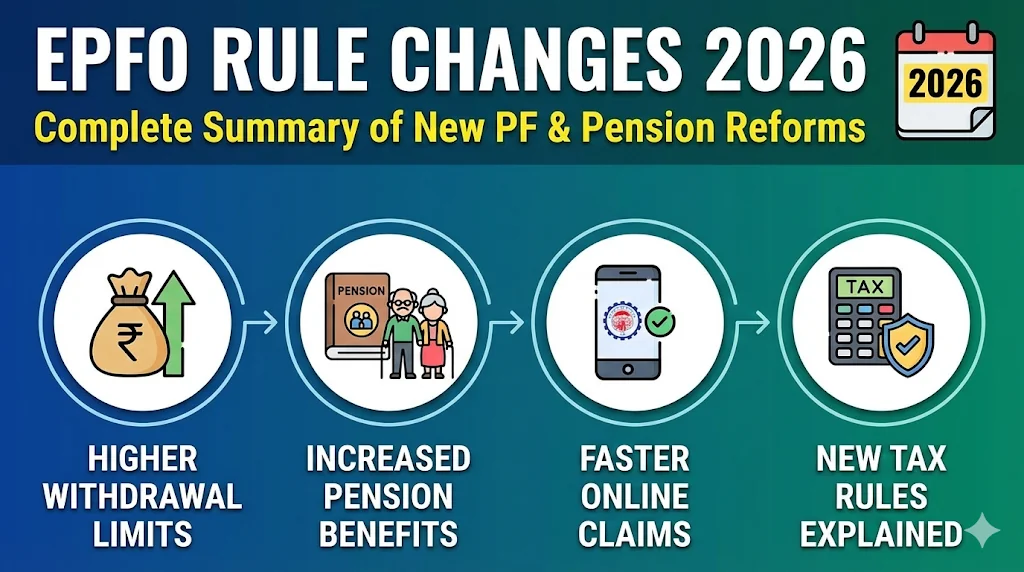

This year, the Employees’ Provident Fund Organisation (EPFO) has introduced a wave of new rules and digital reforms to simplify, accelerate, and make the EPF system more transparent for over 7 crore active members across the country.

Whether you're checking your EPF balance, withdrawing funds, transferring PF after a job change, or planning retirement, this blog gives you a clear, jargon-free summary of every major rule change.

Think of it as your 2026 cheat sheet for everything new in EPF, explained in simple terms.

Let’s dive in and see what’s changed and, more importantly, how it benefits you.

Table of Contents

- Key EPFO Rule Changes You Must Know in 2026

- 2026 EPFO Rule Changes – Summary Table

- Useful Links & Official Resources

- Conclusion: A New Era for EPF Members in 2026

Key EPFO Rule Changes You Must Know in 2026

1. PF Transfers When Changing Jobs Without Employer Approval

| Feature.. | Old Rule | New 2026 Rule |

| Transfer Process | Required employer sign-off and paperwork | Now automatic if Aadhar and UAN details match |

| Time Taken | Weeks, with delays if the employer was unresponsive | Happens instantly in most cases |

Impact: Faster portability, no dependency on past employers.

Want the step-by-step process? Read our 2026 on transferring PF without employer approval. Changing jobs and facing PF transfer issues?

Let Kustodian handle it for you, and we’ll ensure your PF transfer happens fast and error-free. Get Expert Help →

2. Profile & KYC Updates Now Fully Digital

- Old Process: Updates to name, Date of Birth (DOB), or gender require document upload and employer verification.

- New in 2026: If your UAN is Aadhaar-linked, you can update your personal details directly on the EPFO portal, without requiring any documents or employer involvement.

Impact: Less paperwork, faster resolution for errors like name mismatch or DOB errors.

Note: UANs created before October 2017 may still require manual approval.

3. Digital Joint Declaration Replaces Paperwork

Joint Declarations used for correcting details like name, gender, or date of birth (DOB) in EPF records can now be submitted entirely online for members whose UAN is Aadhaar-verified. Earlier, employees had to fill a physical Joint Declaration form, get it signed by their employer, and submit it to the EPFO office, which often caused delays and multiple follow-ups.

With the updated digital process, members can now request corrections directly through the EPFO Unified Member Portal. Once the request is submitted, the employer can review and approve it online, after which EPFO verifies the details using the member’s Aadhaar records. This significantly reduces paperwork, speeds up processing time, and minimizes the chances of rejection due to document mismatches.

However, it’s important that the details in your Aadhaar, PAN, and UAN records match, as Aadhaar has become the primary identity verification source for EPFO services. If there is a mismatch with Aadhaar, the correction may still require additional documentation or employer verification.

Impact: Smoother corrections, especially useful for younger employees and gig workers.

Need to correct your name, date of birth, or gender on EPF?

We’ll fix it digitally, no employer follow-up required.

4. Centralised Pension Payment System (CPPS)

Centralised Pension Payment System (CPPS): The CPPS is now fully operational across all 122 regional offices. Pensioners can change their bank or city without moving their Pension Payment Order (PPO).

Payment is now disbursed via a single national gateway, ensuring credit on the 1st of every month regardless of location.

Impact: Pensioners no longer need to visit physical offices when shifting cities; their pension follows them to any bank in India automatically.

| Feature | Old Rule | New Rule |

| Payment Channel | State-wise EPFO offices and PPOs | Centralized via NPCI |

| Bank Accounts | Limited to the home branch | Any bank account across India |

| Delay Risk | High due to regional dependencies | Almost eliminated |

Impact: Pensioners can receive payments on time in any bank account across India.

5. Housing Advance Made More Accessible

| Rule | Old | New |

| Eligibility | 5 years EPF membership | Reduces to 3 years |

| Limit | 90% corpus for home purchase/construction | Remains the same |

| Frequency | Once in a lifetime | No change |

Impact: First-time homebuyers can use EPF for down payments or EMIs more easily.

If you’re unsure whether your Aadhaar, name, or DOB is correctly updated as per 2026 rules, a Free EPF Audit can help verify everything before you apply for any claim.

Read more about this rule in our blog: EPF Rule Change 2026 – First-Time Homebuyers Can Now Withdraw 90% of EPF Corpus After 3 Years.

6. EDLI Insurance Coverage Now Stronger

| Feature | Old Rule | New Rule |

| Insurance Cap | ₹2.5-₹6 lakh | Increased to ₹7 lakh |

| Minimum balance required | Yes | No minimum balance required |

| Service gap limit | Not defined | Gaps under 60 days allowed. |

| Claim window | Unclear | Allowed up to 6 months from the last salary credit |

Impact: Better financial safety for families, especially for low-income workers. Not sure if your EPF account is linked to EDLI?

Our team can check your eligibility and help your family get full coverage.

Talk to an EPF Expert!

7. Higher Pension Rules for Exempted Establishments

- EPFO is auditing exempted private trusts that offer higher pensions under the “Pension on Higher Wages (PoHW)” scheme.

- All trusts must now follow uniform, transparent recovery and pension payment rules..

Impact: Improved compliance and more clarity for high earners.

8. Cheque Upload & Passbook Image No Longer Needed

A bank passbook or cancelled cheque is not required for claim submissions if your bank account is NPCI-verified and UAN-linked.

Impact: Fewer technical rejections and faster claim processing.

9. Partial Withdrawal Rule Updates

Members can now apply digitally for partial EPF withdrawals for marriage, education, or medical emergencies, using a simplified process on the EPFO app or website.

EPFO has replaced 13+ complex withdrawal reasons with 3 Simple Categories: Essential Needs (Medical/Education), Housing, and Special Circumstances. This has reduced rejection rates by 40%.

Withdrawal ceilings are no longer fixed; they’re automatically adjusted each year in line with national wage inflation, so members retain their purchasing power over time.

Impact: Members enjoy faster, easier emergency access to their EPF funds, without outdated withdrawal limits eroding the actual benefit.

10. Inclusion of Gig & Contract Workers

Mandatory EPF participation now covers most gig workers, app-based platform workers, part-time, and fixed-term contract staff, helping extend social security to India’s growing informal workforce.

Exclusions now only apply if workers are already enrolled in another statutory (government-backed) pension plan, preventing double coverage but maximizing reach.

Impact: Millions of new workers get EPF coverage and social security benefits, reducing vulnerability among non-traditional employees.

11. Self-Declaration of Wages

- When joining a new employer, employees can directly and digitally state their actual wage level, which forms the basis for PF deductions and contributions.

- Employers must either verify or contest this declaration within 15 days; if they take no action, the declaration becomes automatically approved, ending disputes and delays.

Impact: Employment transitions and EPF onboarding are smoother, empowering employees and eliminating paperwork bottlenecks.

12. Auto-Settlement of Dormant Accounts

- EPFO’s systems now proactively flag accounts dormant for 3 years, sending reminders to the member, nominee, and legal heir via SMS/email and app notifications.

- If unclaimed for a further 12 months, funds are shifted to a "central unclaimed pool" but remain fully reclaimable upon proper verification, and nothing is forfeited.

Impact: Prevents loss of dormant EPF balances, enhances transparency, and helps families recover forgotten sums.

Start with a Free EPF Audit

. Our team traces inactive accounts, checks service history, and confirms whether your forgotten PF is still recoverable.

13. Tax & TDS Clarification

- Tax Deducted at Source (TDS) is now charged only on withdrawals exceeding ₹50,000 made before five years of service, exceptions are allowed for specific hardships such as medical or educational emergencies.

- Interest earned on annual EPF contributions above ₹2.5 lakh is taxable, but the EPFO portal now provides an automated tool to calculate your tax in advance.

Impact: Members face fewer tax surprises and can comply more easily with tax rules, while the process is much clearer and fairer.

14. EPS (Pension) Nominee Flexibility

- Members can now assign multiple nominees for their EPS (pension) benefits, not just one, by allocating specific shares among different family members digitally.

- All nominee information is securely stored and instantly integrated into pension disbursal calculations, making claims simpler for families.

Impact: Family financial planning is more flexible, and future pension claims are processed smoothly and accurately.

15. Cross-Border Digital Access for NRIs

- NRIs can manage every aspect of their EPF/EPS accounts online, from updating details to filing claims, checking balances, and even transferring pension payments directly to NRE/NRO accounts.

- EPFO now recognizes select international social security agreements, enabling members to aggregate service and avoid double contributions under specific treaties.

Impact: NRIs gain full, remote control of their EPF accounts, making pension planning and withdrawals seamless across orders.

16. Employment Linked Incentive (ELI) Scheme for Job Creation

EPFO has introduced the ELI Scheme, effective August 1, 2026, under the Union Budget 2026. The scheme offers wage incentives and employer bonuses to boost job creation and formal sector employment.

- Part A (Employees): First-time EPFO-registered workers earning up to ₹1 lakh per month receive one month's EPF wage (up to ₹15,000) in two instalments, after 6 months and 12 months, conditional on completing a financial literacy course.

- For those who joined the workforce in 2026, you are now eligible for the 2nd installment of the ₹15,000 incentive.

- Part B (Employers): Businesses hiring additional staff (minimum 2–5, depending on size) get up to ₹3,000 per employee per month, for two years (extended to four for manufacturing firms)

Impact: Encourages formal employment, enhances social security, and provides EPF-linked income benefits to both fresh employees and employers. To understand how the ELI Scheme works in detail, including eligibility, benefits, and the application process, read our guide on the ELI Scheme here.

2026 EPFO Rule Changes – Summary Table

| Rule Change | What Changed | Impact |

| PF Transfers | No employer sign-off needed; transfers happen automatically if Aadhaar & UAN match. | Faster job transitions, no employer dependency |

| Digital KYC & Profile Updates | Aadhaar-linked users can update their name, DOB, and gender without documents or an employer. | Quicker fixes for demographic errors |

| Online Joint Declarations | Name/gender/DOB corrections are now fully digital for Aadhaar-verified users. | No paperwork or offline visits needed. |

| Centralized Pension Payments | NPCI-managed; allows pension credit to any bank account in India. | Timely, location-independent pension disbursal. |

| Housing Advance Eased | EPF housing advance eligibility reduced from 5 to 3 years. | More members can use PF for housing needs sooner |

| EDLI Insurance Boost | Coverage raised to ₹7 lakh, no balance requirement, gaps up to 60 days allowed. | More families get death benefit support, especially low-income workers. |

| Higher Pension for Exempted Trusts | Uniform audit and payout rules for private PF trusts offering higher pensions. | Standardized compliance, benefits for high earners. |

| No Cheque or Passbook Needed | NPCI-verified UAN-linked accounts don’t need bank proof uploads | Fewer rejections, quicker claims. |

| Partial Withdrawal Simplification | Online withdrawals are allowed for more cases; ceilings adjusted for inflation. | Easier emergency withdrawals, no outdated limits. |

| EPF for Gig & Platform Workers | Coverage extended to gig, part-time, and contract workers. | The social security net expands for the informal workforce. |

| Self-Wage Declaration at New Job | Employees declare salary directly; auto-approved if the employer doesn’t act within 15 days. | Less conflict, faster onboarding to PF. |

| Auto-Settlement of Dormant Accounts | Dormant accounts flagged and notified; transferred to reclaimable pool after 12 months. | No EPF money is lost; better access for heirs. |

| Tax & TDS Clarifications | Clear rules: TDS only on large early withdrawals; interest on ₹2.5L+ taxable; online tax calculator added. | Fewer surprises, easier tax compliance. |

| EPS Nomination Flexibility | Members can assign multiple EPS nominees with specific shares. | Smarter family planning and smoother future claims |

| NRI Cross-Border Access | NRIs can manage EPF/EPS fully online; pension transferable to NRE/NRO; treaty benefits apply. | Seamless EPF access and planning for global workers. |

| Employment Linked Incentive (ELI) Scheme | Financial incentives delivered via EPF-linked DBT to new employees and employers; requires UAN + Aadhaar linking | Formal job growth, EPF coverage expanded, financial uplift for freshers, and businesses |

Useful Links & Official Resources

Official EPFO Portals

- EPFO Official Website – Access official notifications, circulars, schemes, and policy updates from the Employees’ Provident Fund Organisation.https://www.epfindia.gov.in

- EPFO Unified Member Portal – Log in with your UAN to file PF withdrawal claims, update KYC, transfer PF when changing jobs, and manage your EPF account online.https://unifiedportal-mem.epfindia.gov.in/memberinterface/

- EPF Passbook Portal – Check your EPF balance, monthly contributions, and employer deposits.https://passbook.epfindia.gov.in

- EPFO Claim Status Portal – Track the status of your EPF withdrawal or transfer request.https://passbook.epfindia.gov.in/MemberPassBook/Login

Government Apps & Digital Services

- UMANG App – A government mobile app that allows you to access EPFO services such as PF withdrawal, claim tracking, pension services, and KYC updates directly from your smartphone.https://umang.gov.in

- Jeevan Pramaan (Digital Life Certificate) – Pensioners can submit their life certificate online without visiting EPFO offices or banks.https://jeevanpramaan.gov.in

EPFO Forms & Member Services

- EPFO Forms Download Page – Download important EPFO forms such as Form 19, 10C, 31, 10D, 13, 20, and 5IF.https://www.epfindia.gov.in/site_en/Forms.php

- UAN Activation Portal – Activate your Universal Account Number (UAN) to start managing your EPF account online.https://unifiedportal-mem.epfindia.gov.in/memberinterface/no-auth/registration

Frequently Asked Questions (FAQs)

1. What are the biggest EPFO rule changes introduced in 2026?

The major EPFO changes in 2026 focus on digitization, faster claims, and improved accessibility. Key updates include automatic PF transfers when changing jobs, digital profile and KYC updates, online joint declarations, simplified PF withdrawals, expanded EPF coverage for gig workers, and a centralized pension payment system (CPPS) for pensioners.

2. Is employer approval still required for PF transfer in 2026?

No. Under the new EPFO system, PF transfers happen automatically when you change jobs if your UAN is active and Aadhaar details match. This eliminates the need for employer approval in most cases and significantly speeds up the transfer process.

3. Can EPF details like name or date of birth be corrected online?

Yes. If your UAN is linked with Aadhaar, you can update details like name, gender, and date of birth directly through the EPFO portal without uploading documents or getting employer verification in many cases.

4. What is the Centralised Pension Payment System (CPPS)?

The Centralised Pension Payment System (CPPS) is a new EPFO system that allows pension payments to be processed through a single national gateway via NPCI. Pensioners can now receive their pension in any bank account across India without transferring their Pension Payment Order (PPO).

5. Has the EPF housing withdrawal rule changed in 2026?

Yes. The eligibility period for withdrawing EPF for housing purposes has been reduced from 5 years to 3 years of EPF membership. Members can still withdraw up to 90% of their EPF corpus for purchasing or constructing a house.

6. What is the maximum insurance coverage under the EDLI scheme in 2026?

Under the updated Employees’ Deposit Linked Insurance (EDLI) scheme, the maximum insurance benefit has been increased to ₹7 lakh for the nominee or legal heir of an EPF member in case of death while in service.

7. Can gig workers and contract workers now join EPF?

Yes. EPFO has expanded its coverage to include gig workers, platform workers, part-time employees, and fixed-term contract workers, allowing more people in the informal workforce to receive social security benefits.

8. Are cancelled cheques or passbook copies still required for EPF claims?

In most cases, no. If your bank account is NPCI-verified and linked with your UAN, EPFO no longer requires a cancelled cheque or passbook image when submitting claims.

9. What happens to dormant EPF accounts in 2026?

EPFO now proactively identifies dormant accounts after three years of inactivity. Members and nominees receive notifications, and the funds are moved to a central reclaimable pool if unclaimed, ensuring the money is never lost.

10. Are EPF withdrawals taxable in 2026?

EPF withdrawals remain tax-free after 5 years of continuous service. However, withdrawals before five years may attract TDS if the amount exceeds ₹50,000, except in certain cases like medical emergencies or other permitted exemptions.

11. Can NRIs manage their EPF accounts online?

Yes. NRIs can now fully manage their EPF accounts online, including updating details, filing claims, checking balances, and transferring pension payments to NRE or NRO bank accounts, depending on eligibility.

12. What is the Employment Linked Incentive (ELI) Scheme?

The Employment Linked Incentive (ELI) Scheme introduced in 2026 provides financial incentives to encourage job creation. Eligible new employees can receive up to ₹15,000 as a wage incentive, while employers hiring additional staff may receive up to ₹3,000 per employee per month for a limited period.

Conclusion: A New Era for EPF Members in 2026

The EPFO rule changes in 2026 reflect a strong push toward digitization, transparency, and member convenience. Whether it’s automatic PF transfers, faster emergency withdrawals, Aadhaar-based updates, or better pension planning, these reforms make managing your EPF easier than ever.

For salaried professionals, gig workers, retirees, and even NRIs, the new rules remove much of the red tape that previously made EPF processes confusing or delayed. And with the EPFO’s digital-first approach, most updates can now be handled online without employer dependency.

If you or your family have an EPF account, now’s the perfect time to review your details, update nominations, and ensure your KYC is completed. These simple steps can help you make the most of the new benefits introduced this year.

Want to make the most of these EPF rule changes?

Let our experts simplify the process and ensure your account is fully compliant.

Talk to Us!

Stay updated, stay informed, and take control of your EPF with confidence in 2026 !

Secure Your Future with Kustodian

At Kustodian.life, we’re committed to making EPF simpler, smarter, and stress-free for both employees and employers. Whether you’re trying to understand how the latest rule changes apply to you, need help with UAN activation, or want expert support with EPF claims and compliance, our team is here to guide you every step of the way.

- Need clarity on your eligibility?

- Worried about documentation or KYC mismatches?

- Want to make the most of these new benefits?

If you’d like step-by-step support to resolve your EPF issues and ensure faster claim approval, we’re here to guide you.

Let’s help you make sense of the 2026 EPFO reforms, whether it’s understanding PF transfers, pension hikes, EDLI updates, or instant withdrawals. With these updates in place, securing your financial future has never been easier.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.