Planning for retirement can feel overwhelming. Between rising expenses, family responsibilities, and long-term financial goals, you want assurance that your savings are growing safely. That’s where the Employees’ Provident Fund (EPF) becomes a trusted companion in your journey.

If you’ve been searching for epf interest rate for the last 10 years, EPF interest rate history, or wondering how to calculate PF interest on balance, you’re not alone. Let’s break it down in a simple, reassuring way so you can understand how your EPF balance grows over time.

What Is EPF and Why Does the Interest Rate Matter?

The Employees’ Provident Fund (EPF) is a retirement savings scheme managed by the Employees' Provident Fund Organisation (EPFO) in India. Both employees and employers contribute a portion of their salaries to this fund every month.

The interest rate declared annually plays a crucial role because:

- It determines how much your savings grow.

- It compounds over time.

- It significantly impacts your retirement corpus.

Even a small change in interest rate can make a noticeable difference over the long term.

The Great EPF Reset: Everything Changed in 2025 & What to Expect in 2026

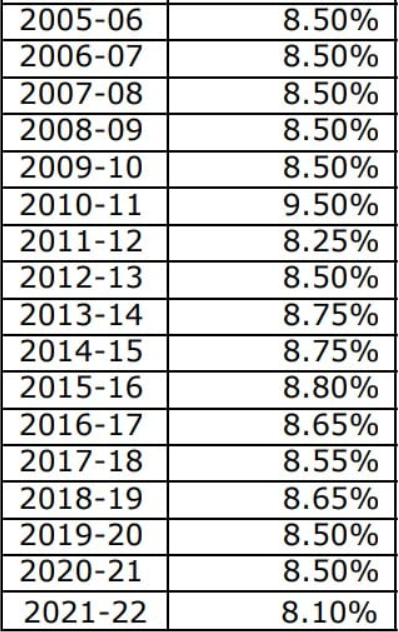

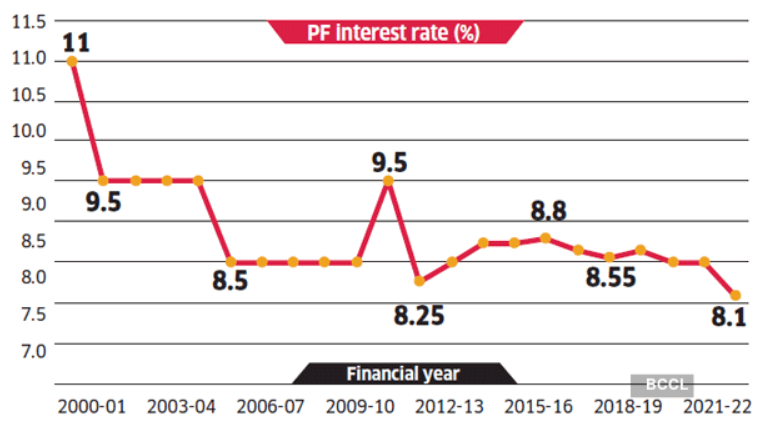

EPF Interest Rate History: Last 10 Years

Understanding the EPF interest rate history helps you see trends and make better financial decisions. Here’s a look at the epf interest rate last 10 years:

| Financial Year | EPF Interest Rate |

| 2014–15 | 8.75% |

| 2015–16 | 8.80% |

| 2016–17 | 8.65% |

| 2017–18 | 8.55% |

| 2018–19 | 8.65% |

| 2019–20 | 8.50% |

| 2020–21 | 8.50% |

| 2021–22 | 8.10% |

| 2022–23 | 8.15% |

| 2023–24 | 8.25% |

What Does This Tell Us?

- EPF rates have largely stayed between 8% and 9%.

- There has been a gradual decline compared to earlier decades.

- Despite fluctuations, EPF remains one of the more stable fixed-income retirement options.

If you’ve been worried about falling rates, remember this: EPF is designed for long-term stability, not short-term speculation.

How Balance Growth Happens in EPF

Your Employee Provident Fund (EPF) isn't just a static savings account; it’s a dynamic retirement engine. Here is a breakdown of how that balance actually builds up:

Monthly Inflow: Every month, a portion of your basic salary (typically 12%) is deducted, and your employer matches a significant part of it. This ensures a consistent increase in the principal amount.

Annual Interest: The EPFO (Employees' Provident Fund Organisation) declares an annual interest rate. While the interest is calculated monthly on your closing balance, it is officially credited once a year on March 31st.

The Power of Compounding: Because the interest earned in one year becomes part of the principal for the next, your money grows exponentially. The longer you leave it untouched, the faster the "snowball effect" takes over.

Interest is calculated on the monthly running balance but credited at the end of the financial year. Over 20–30 years, this compounding effect becomes powerful. What feels like a modest contribution today can grow into a meaningful retirement fund.

PF Balance Using UMANG & Bank Apps (2026): Step-by-Step Guide Without EPFO Login

How to Calculate PF Interest on Balance

Many people ask how to calculate pf interest on the balance. It is a simple process, but an important one to know more about how much you will get at the end of your work life. Here’s a simple explanation:

Step 1: Know the Interest Rate

Assume the current EPF interest rate is 8.25%.

Step 2: Understand the Formula

EPF interest is calculated monthly but credited annually.

Monthly interest calculation formula:

Monthly Interest = (EPF Balance × Interest Rate) ÷ 12

Where:

- Interest Rate = Annual Rate ÷ 100

Calculate your EPF Interest for free

Example Calculation

Let’s say:

- Opening EPF balance = ₹5,00,000

- Annual interest rate = 8.25%

Annual interest = ₹5,00,000 × 8.25% = ₹41,250

If you’re contributing monthly, each month’s new contribution also earns interest from that month onward. Because of this structure, manually calculating interest can be slightly complex. Using an EPF calculator simplifies things, but understanding the concept helps you stay financially aware and empowered.

PF Balance vs Withdrawable Amount: What You Can Actually Take Out (2026 Guide)

How a Small Rate Change Impacts Your Retirement

Let’s look at a simple emotional truth: retirement planning isn’t just about numbers. It’s about peace of mind. If you contribute ₹15,000 per month for 25 years:

- At 8.10%, your corpus will be lower.

- At 8.50%, the final amount increases significantly due to compounding.

Even a 0.25% change over decades can translate into lakhs of rupees difference.

That’s why keeping track of the EPF interest rate history matters - not for anxiety, but for awareness.

Is EPF Still a Good Retirement Option?

Despite fluctuations in the EPF interest rate over the last 10 years, EPF remains:

Sovereign Safety: The Government-Backed Guarantee

As a statutory scheme under the Ministry of Labour and Employment, the EPF offers a level of security that is rare in the financial world. Because it is government-backed, the safety of your principal amount is virtually guaranteed, protecting your retirement nest egg from the risks associated with private financial institutions or market-driven volatility.

Reliable Returns: Stability in an Uncertain Market

While equity markets and mutual funds may see wild swings, the EPF remains relatively stable. The interest rate is declared annually by the EPFO, providing a predictable growth trajectory. Even when rates fluctuate slightly over a decade, they typically remain higher than standard bank savings accounts or fixed deposits, offering a dependable shield against inflation.

Optimised Gains: A Tax-Efficient Savings Vehicle

The EPF is designed to be highly tax-efficient, traditionally falling under the "Exempt-Exempt-Exempt" (EEE) category. Subject to prevailing rules - such as the five-year continuous service requirement - your contributions, the interest accrued, and the final maturity amount can all be exempt from tax. This ensures that a larger portion of your hard-earned money stays in your pocket during your retirement years.

Wealth Multiplier: The Magic of Compounding

The true engine behind the EPF's growth is its compounding-based nature. By reinvesting interest on a monthly running balance and crediting it annually, the fund turns small, disciplined monthly contributions into a massive corpus over time. The longer the money stays in the fund, the more the interest itself begins to earn interest, creating an exponential growth curve that rewards long-term patience. If you’re feeling uncertain about market-linked investments, EPF offers a layer of safety and predictability in your retirement planning.

Conclusion

Your EPF is more than just a salary deduction - it’s a long-term promise to your future self. Looking at the EPF interest rate history and understanding how to calculate pf interest on balance empowers you to take control of your retirement planning. While rates may fluctuate slightly over the years, the power of steady contributions and compounding remains strong.

If you stay consistent and informed, your EPF can quietly grow into a financial cushion that supports your dreams - whether that’s a peaceful retirement, supporting your children, or simply living stress-free. Remember, financial planning isn’t about perfection. It’s about progress.

Frequently Asked Questions (FAQs)

1. What is the EPF interest rate for the last 10 years?

The EPF interest rate for the last 10 years has generally remained stable, fluctuating within a narrow range of 8.10% to 8.80%. This stability is one of the key reasons why the Employees’ Provident Fund remains a popular long-term retirement savings option in India.

Below is a quick overview of EPF interest rates announced by the Employees' Provident Fund Organisation for recent years:

| Financial Year | EPF Interest Rate |

| 2024–25 | 8.25% |

| 2023–24 | 8.25% |

| 2022–23 | 8.15% |

| 2021–22 | 8.10% |

| 2020–21 | 8.50% |

| 2019–20 | 8.50% |

| 2018–19 | 8.65% |

| 2017–18 | 8.55% |

| 2016–17 | 8.65% |

| 2015–16 | 8.80% |

Even though the rate has seen minor variations, it has consistently remained above 8%, which is relatively attractive compared with many traditional fixed-income options.

Because EPF also benefits from tax advantages under Section 80C and tax-free interest (subject to limits), it continues to be considered a reliable retirement corpus builder.

2. How is EPF interest calculated?

EPF interest is calculated every month on the running balance of your provident fund account, but the accumulated interest is credited only once at the end of the financial year.

The basic formula used to calculate PF interest is:

(EPF Balance × Annual Interest Rate) ÷ 12

This gives the monthly interest amount on your balance.

However, in practice, the calculation considers the monthly closing balance of your EPF account. This means:

- Contributions made during the month start earning interest from the next month.

- Withdrawals made during the month stop earning interest from the same month.

For example:

If your EPF balance is ₹2,00,000 and the interest rate is 8.25%, the approximate monthly interest would be:

₹2,00,000 × 8.25% ÷ 12≈ ₹1,375 per month

Over a year, this interest accumulates and is credited to your EPF passbook.

3. Is EPF interest compounded?

Yes, EPF interest is effectively compounded annually.

Although the interest calculation happens monthly, the total interest accumulated over the year is credited at the end of the financial year (usually after the rate is approved by the government).

Once the interest is credited:

- It becomes part of your principal balance.

- The next year’s interest is calculated on the new, higher balance.

This process creates a compounding effect, helping the retirement corpus grow steadily over time.

For long-term employees who contribute for 20–30 years, this annual compounding can significantly increase the final retirement savings.

4. Why has the EPF interest rate reduced in recent years?

The EPF interest rate is influenced by several macroeconomic factors. Over the past decade, there has been a gradual moderation in rates due to broader changes in financial markets.

Key reasons include:

1. Lower government bond yields- EPFO invests a large portion of EPF funds in government securities and bonds. When bond yields fall, the returns generated by these investments also decline.

2. Market investment returns- A portion of EPF funds is also invested in equities and ETFs, which can influence overall returns depending on market performance.

3. Economic policy environment- Interest rates across the economy such as bank deposit rates have declined compared to a decade ago, which affects the rates offered by long-term savings schemes.

Despite this decline, EPF still offers higher and more stable returns than many fixed deposits, along with tax advantages.

5. Can the EPF interest rate change every year?

Yes. The EPF interest rate is reviewed and announced every financial year. The process usually follows these steps:

- The Central Board of Trustees (CBT) of the Employees' Provident Fund Organisation recommends the interest rate.

- The recommendation is sent to the Ministry of Finance for approval.

- After approval, the rate is officially notified and credited to members’ accounts.

Because the rate depends on investment earnings and economic conditions, it may increase, decrease, or remain the same each year. This annual review ensures that EPF interest rates remain aligned with the returns generated by EPFO’s investment portfolio.

How Kustodian Can Help You

Managing your financial future shouldn't feel like a second job. By bringing clarity to your retirement savings, Kustodian transforms a complex statutory requirement into a clear, actionable wealth strategy.

Effortless Oversight: Track Your EPF Balance and Contributions

Visibility is the first step toward financial security. Kustodian allows you to track your EPF balance and monthly contributions with zero friction, eliminating the need to navigate cumbersome government portals. By centralising your data, you can verify that both your portion and your employer’s contributions are being deposited correctly and on time, ensuring your nest egg is growing exactly as it should.

Strategic Insights: Monitor Trends Using EPF Interest Rate History

Context is key to understanding performance. Kustodian provides a comprehensive view of the EPF interest rate history, allowing you to see how your savings have performed against the backdrop of changing economic cycles. This historical perspective helps you understand the stability of the fund and how the Ministry of Labour’s annual declarations impact your long-term wealth compared to other asset classes.

Precision Tools: Instantly Calculate PF Interest on Balance

Wait no longer for your annual statement to see where you stand. Our platform allows you to instantly calculate PF interest on your current monthly running balance. By applying the latest declared rates to your specific numbers, Kustodian gives you a real-time look at your accrued earnings, helping you visualise the "hidden" growth that happens between official annual credits.

Future Forecasting: Project Your Retirement Corpus

Planning for the "finish line" requires more than just looking at today’s balance. Kustodian uses the EPF interest rate trends from the last 10 years to help you project your total retirement corpus. By adjusting for salary hikes and potential contribution changes, you can see a realistic map of your financial future, allowing you to decide if you need to supplement your EPF with VPF (Voluntary Provident Fund) or other investments to reach your goals.

With clear insights and simple tools, Kustodian helps you stay informed, confident, and in control of your retirement journey.

Disclaimer: This article is based on the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952 and official EPFO guidelines. Policies may change as per Government notifications.