The National Pension System (NPS) has long been a cornerstone of retirement planning in India, but for Non-Resident Indians (NRIs), it often feels like a puzzle spanning two different countries. As of 2026, the landscape for NRI investors has shifted significantly, offering more flexibility and a few new tax nuances than ever before.

Managing your NPS as an NRI isn't just about picking the right funds; it’s about navigating the intersection of Indian tax law, foreign reporting requirements, and the Double Taxation Avoidance Agreement (DTAA). With recent PFRDA reforms allowing for 80% lump-sum withdrawals and the introduction of Systematic Unit Redemption (SUR), the "how" and "when" of your exit strategy now define your actual take-home wealth.

This guide breaks down the essential 2026 rules to help you avoid the common trap of double taxation and ensure your retirement funds remain truly repatriable.

Contents

1. “I’m an NRI. Will My NPS Be Taxed Twice?”

2. Who Is Considered an NRI for NPS Tax Purposes?

3. Can NRIs Invest in NPS in 2026?

4. How NPS Is Taxed for NRIs: The Big Picture

5. Tax on Lump‑Sum NPS Withdrawal for NRIs

6. Tax on NPS Annuity (Pension) for NRIs

7. DTAA and NPS: How Double Taxation Is Avoided

8. SLW / SUR for NRIs: Managing Tax Timing

9. Repatriation, Bank Accounts & FEMA Reality

10. Special NRI Scenarios (2026)

12. When NRIs Should Get Expert Help

13. Frequently Asked Questions

1. “I’m an NRI. Will My NPS Be Taxed Twice?”

This is the most common and completely valid fear NRIs have when they move abroad or begin planning their NPS exit.

The anxiety usually begins the moment two tax systems seem to overlap. What was once a straightforward retirement account suddenly sits at the intersection of Indian tax law, foreign tax rules, DTAA clauses, and FEMA regulations. Online discussions often amplify the fear by focusing on worst‑case scenarios without explaining how taxation actually works.

In practice, the concern usually comes from a few recurring assumptions:

- India may tax the entire NPS corpus at exit.

- The country of residence may tax the same income again.

- DTAA rules appear unclear or too technical to apply correctly

- NPS proceeds may get stuck in India due to banking or repatriation limits

The reality is significantly calmer.

NPS is not designed to penalise NRIs.Most NRI tax issues arise due to timing mismatches, exit structuring errors, or reporting gaps, not because the law intends double taxation.

Whether your NPS is taxed once, twice, or efficiently exempted depends mainly on three controllable factors:

- Your residential status at the time of withdrawal

- The form in which you exit (lump sum, annuity, phased withdrawal)

- Correct and timely application of DTAA relief

When these are aligned properly, double taxation is usually avoidable.

"If you have an old EPF balance from your pre-NRI years, the tax rules and residential status requirements are quite different from NPS. Check our NRI EPF Withdrawal Guide: 2026 Rules to ensure your global income reporting is aligned."

2. Who Is Considered an NRI for NPS Tax Purposes?

Before discussing exemptions or DTAA benefits, it is essential to establish your tax identity.

Indian tax law does not rely on citizenship, passport, or visa category. Instead, it uses residential status under the Income‑tax Act, determined annually based on physical presence in India.

Broadly, individuals fall into one of the following categories:

| Status. | What it broadly means | Why it matters for NPS |

| Resident | Stayed in India beyond limits | Global income may be taxable in India |

| RNOR | Transitional resident status | Partial global income exposure |

| NRI | Stayed outside India | Only Indian source income is taxed. |

Two clarifications that resolve most confusion

- Your passport does not decide NPS tax. Residential status does.

- Residential status in the year of withdrawal matters more than status during contribution years.

Many subscribers contributed to NPS while residents, but will exit as NRIs. The tax treatment follows the exit‑year residential status, not the historical contribution period.

3. Can NRIs Invest in NPS in 2026?

Yes, NRIs can continue with NPS, subject to specific conditions.

If you opened your NPS account while you were a resident Indian, you are generally allowed to continue the account after becoming an NRI. There is no mandatory closure triggered by a change in residential status.

However, post‑NRI contributions must comply with FEMA and tax rules:

- Contributions must be routed through an NRO account.

- Direct remittance from overseas income is not permitted.

- Section 80CCD tax deductions are available only if you have taxable income in India.

From a practical standpoint, contribution stage issues are uncommon.

Most NRI-related NPS problems surface at exit, not during contribution.

4. How NPS Is Taxed for NRIs: The Big Picture

Instead of memorising tax sections, it helps to understand NPS through three payout streams. Each stream is taxed differently, even though all arise from the same account.

| Payout stream. | Nature of income | DTAA relevance |

| Lump‑sum withdrawal | Capital‑linked retirement benefit | Limited |

| Annuity (pension) | Recurring income | High |

| Phased withdrawals (SLW / SUR) | Income spread over years | Medium |

This framework is critical. Confusion usually occurs when one assumes that if the lump sum is exempt, the pension must also be exempt, which is factually incorrect.

5. Tax on Lump‑Sum NPS Withdrawal for NRIs

Lump‑sum taxation is the least controversial part of NPS.

Under Indian tax law:

- Up to 60% of the NPS corpus withdrawn as a lump sum is tax‑exempt.

- This exemption applies equally to residents and NRIs

- Any taxable portion may attract TDS in NRI cases.

Where NRIs Face Practical Friction

While the law itself is clear, execution creates challenges:

- Credits are routed to an NRO account, not NRE.

- Trustees or banks may deduct TDS conservatively.

- Refunds or DTAA relief require proper Indian return filing

The statute is generous; administration is where most issues arise.

"A common reason for NRI payout failure isn't the tax law, it's a technical mismatch in NRO bank records. Read our guide on Resolving Technical Rejections in Retirement Payouts to ensure your 'Penny-Drop' verification doesn't fail due to an outdated profile."

While the PFRDA now allows you to withdraw up to 80% of your corpus as a lump sum (as of the late 2025 amendment), the tax exemption has not yet been bridged.

- 60% of Corpus: Still 100% Tax-Free.

- Next 20%: Taxable at your slab rate if taken as a lump sum.

- Remaining 20%: Must be used to purchase an annuity (pension), which is taxable annually.

6. Tax on NPS Annuity (Pension) for NRIs

Annuity taxation is the most misunderstood area of NPS for NRIs.

When you purchase an annuity through NPS, the pension you receive is treated as income, not capital. This makes it taxable in the year of receipt.

In practice:

- Pension is credited to an NRO account.

- TDS may be deducted by the Annuity Service Provider

- The income must be reported in Indian tax returns.

An annuity is never tax-free, even if the lump sum withdrawal was fully exempt.

This recurring nature of pension income is precisely why DTAA becomes relevant.

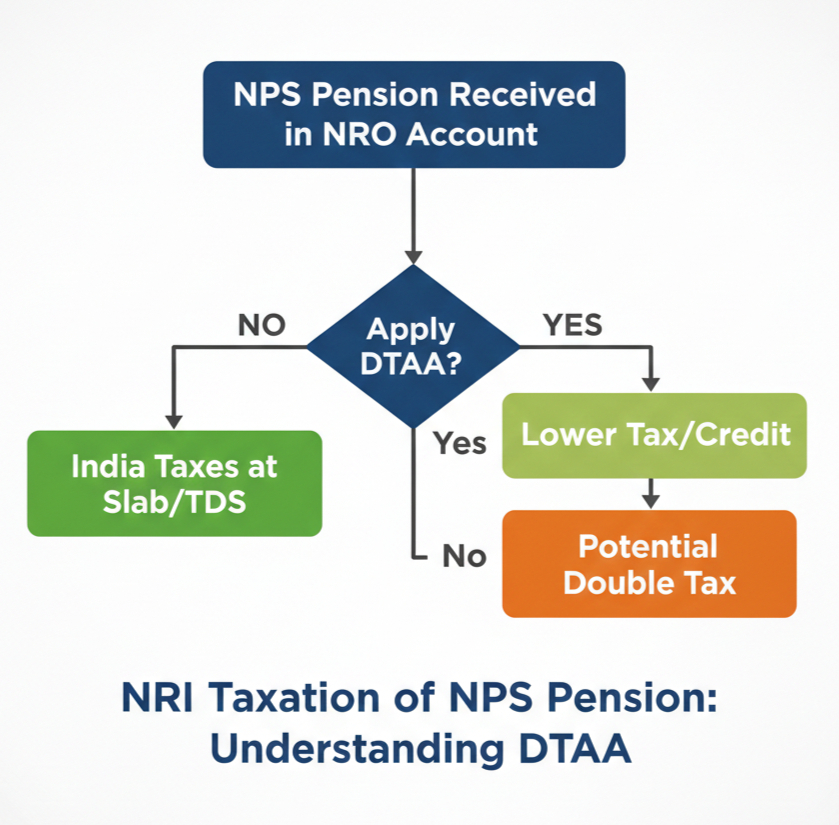

7. DTAA and NPS: How Double Taxation Is Avoided

DTAA exists to ensure the same income is not taxed twice by two jurisdictions.

For NRIs, DTAA matters because:

- NPS income may be taxable in India

- The same income may also be taxable or reportable abroad.

DTAA determines:

- Which country has the primary right to tax

- Whether relief is provided via exemption or tax credit

| DTAA method. | Practical meaning |

| Exemption method | Income taxed in only one country |

| Tax‑credit method | Tax paid in one country is credited in the other |

Treaty wording varies significantly:

- The US, UK, and Canada generally apply tax‑credit methods.

- Several Gulf countries result in minimal or no effective double taxation if documentation is correct.

- Most treaties (like India-USA or India-UK) address pensions under Article 18 or 20. For instance, under the India-USA DTAA, annuities from insurance companies are generally taxable only in the country of residence (USA), provided the correct Tax Residency Certificate (TRC) and Form 10F are submitted to the Indian deductor.

DTAA outcomes depend on treaty language, not assumptions or internet summaries.

| Component | Tax Treatment in India (NRIs) | DTAA Impact |

| Lump Sum (60%) | Fully Tax-Exempt | No impact (already exempt) |

| Annuity (Pension) | Taxable at Slab Rates | Claim Foreign Tax Credit abroad |

| TDS Rate | 31.2% (default) | Can be reduced with TRC + Form 10F |

| Small Corpus (<8L) | 100% Withdrawal allowed | 60% exempt / 40% taxable |

8. SLW / SUR for NRIs: Managing Tax Timing

Where enabled by CRA systems, phased withdrawal options such as SLW or SUR can help manage when tax arises.

These options may:

- Spread taxable income over multiple years.

- Reduce peak slab exposure in India.

- Improve utilisation of DTAA credits in the country of residence

However, they do not create new exemptions and apply only to eligible portions.

These strategies optimise timing, not taxability itself.

9. Repatriation, Bank Accounts & FEMA Reality

Tax compliance alone does not ensure smooth access to funds. FEMA regulations operate independently.

Key realities NRIs must plan for:

- NPS payouts are credited to an NRO account

- Repatriation is permitted but subject to limits and documentation.

- CA certificates and proof of tax compliance are commonly required

Most problems arise when NRIs assume automatic repatriation or expect NRE credits.

"Moving funds from an NRO account to your overseas bank requires a clean KYC profile. If your name or DOB differs between your PRAN and your bank account, follow our Joint Declaration & Profile Correction Guide to sync your records before you exit."

10. Special NRI Scenarios (2026)

Certain situations require additional care and sequencing:

- Renunciation of Indian citizenship

- OCI status

- Multiple country residency history

- Government‑to‑private or India‑to‑abroad employment transitions

These scenarios are manageable but rarely DIY‑friendly.

11. Common NRI Mistakes That Trigger Problems

Across cases, the same patterns repeat:

- Ignoring changes in residential status

- Failing to apply DTAA relief in returns

- Assuming pension income is tax‑free

- Not updating the bank account or KYC details.

- Missing FATCA or CRS declarations

Most NRI NPS issues are compliance gaps, not legal violations.

"A 'Frozen' account status is often just a missing digital compliance step. If your portal shows a block, see our checklist for Unblocking Frozen Retirement Accounts to learn about the latest 2026 digital-first updates."

12. When NRIs Can Get Expert Help

Professional help becomes valuable when:

- DTAA interpretation is unclear

- A high‑value NPS corpus is involved.

- Excess TDS is deducted from pension income.

- Repatriation is delayed or questioned.

- Exit, tax, and residency timelines overlap.

We manage the intersection of NPS, Indian tax law, DTAA, and FEMA compliance end‑to‑end.

A high-tech "Scan" graphic reinforcing the Kustodian NPS Diagnostic Scan.

13. Frequently Asked Questions

Is NPS taxable for NRIs?

NPS is partly taxable for NRIs. The tax treatment depends on what you receive and when. Up to 60% of the corpus withdrawn as a lump sum at retirement is exempt under Indian tax law. However, annuity (pension) income is always taxable in India as and when it is received. Residential status at the time of withdrawal and DTAA provisions then determine whether additional relief is available abroad.

Does DTAA apply to NPS pension income?

Yes, DTAA can apply to NPS pension income, but the manner of relief depends on the specific treaty. In many countries, such as the US, UK, or Canada, the pension may still be taxable locally, but tax paid in India can usually be claimed as a foreign tax credit. DTAA does not automatically make pension tax‑free; it prevents double taxation.

Is the lump‑sum withdrawal also covered by DTAA?

In most cases, DTAA has limited relevance for the exempt portion of the lump sum because Indian law already provides an exemption. If any part of the lump sum becomes taxable in India (for example, due to early exit or excess withdrawal), DTAA may help avoid double taxation depending on the Do treaty wording.

Do banks or annuity providers deduct TDS automatically for NRIs?

Often, yes. In practice, TDS is deducted conservatively on NRI payouts, especially on annuity income. This does not always reflect your final tax liability. Excess TDS can usually be reclaimed by filing an Indian tax return and, where applicable, applying DTAA relief.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and PFRDA processing.