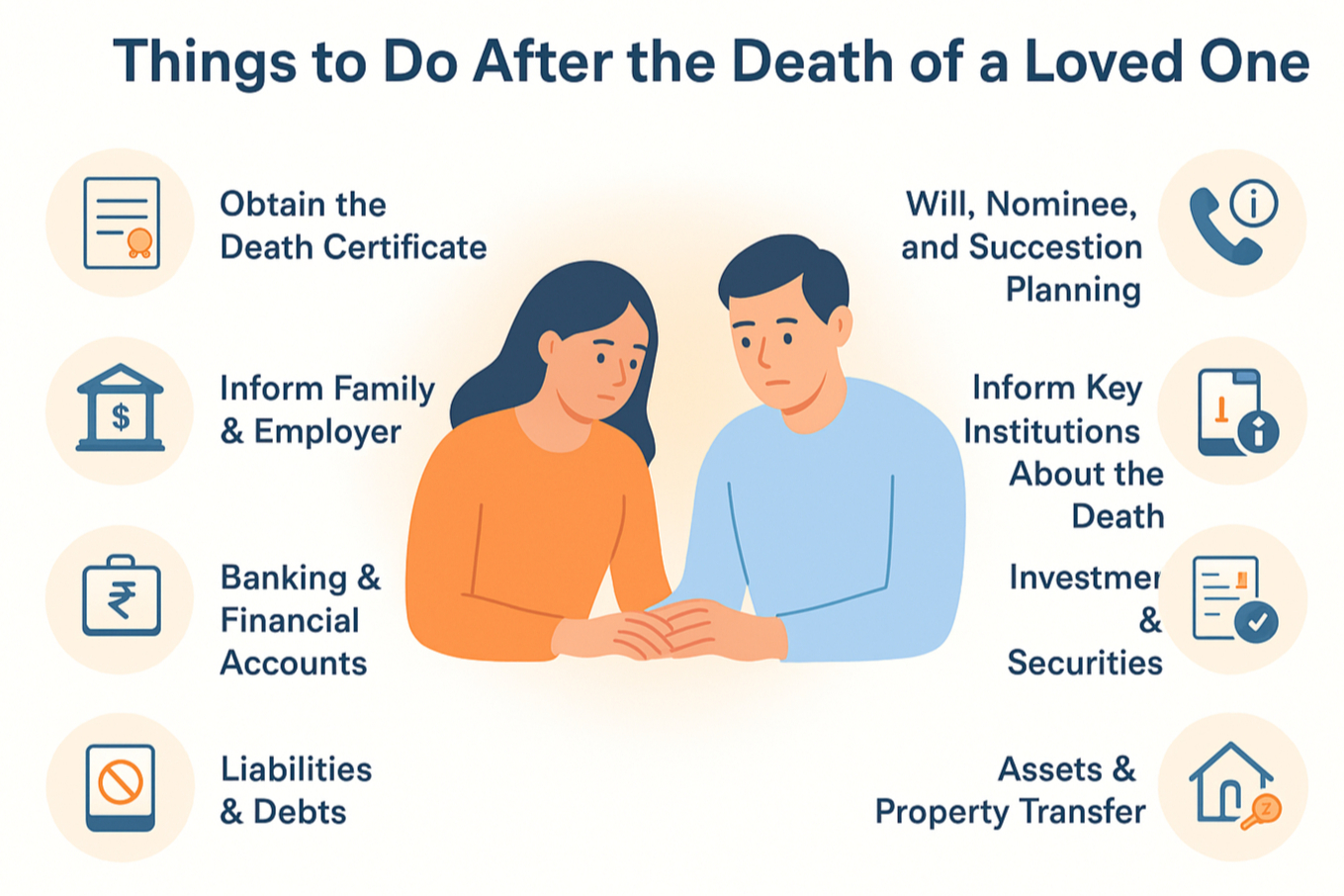

Managing Finances After a Loved One’s Death Doesn’t Have to Be Overwhelming. Follow Our Step-by-Step Guide for EPF, Insurance, Property, and Unclaimed Assets to Protect Your Family’s Future.

Table of Contents

- Introduction – Managing Finances After Death

- Obtain the Death Certificate (First Step)

- Will, Nominee, and Succession Planning

- Inform Key Institutions About the Death

- Banking and Financial Accounts

- Insurance Claims

- Investments and Securities

- Liabilities and Debts

- Essential Documents Checklist

- Conclusion – Securing Your Family’s Financial Future

Introduction - Managing Finances After Death

Losing a loved one is one of life’s most difficult moments. Amid the grief and emotional weight, families are often faced with another challenge: handling the financial and legal matters that follow. From closing bank accounts to transferring assets, there are several steps that need to be taken to secure the family’s future and prevent complications later.

While no one wants to think about paperwork during such times, taking timely financial actions ensures that the wishes of the deceased are respected and that the family is protected from unnecessary delays or disputes.

This guide walks you through the key financial steps to take after the death of a loved one in India, explained in a simple and practical way.

1. Obtain the Death Certificate (First Step)

The very first and most important document you need after the loss of a loved one is the death certificate. Without it, most financial or legal processes cannot even begin.

In India, as per the Registration of Births and Deaths Act, 1969, a death must be registered with the local municipal authority or panchayat within 21 days of its occurrence.

Once registered, you can apply for the official death certificate. Today, many states also provide the option to apply online through their municipal or state e-governance portals, which can save time and effort.

Why it matters:

- Required for insurance claims, bank account settlements, EPF withdrawals, property transfers, and even updating government records.

- Acts as the official proof of death for all institutions.

Confused about documentation or where to apply for a death certificate online?

Our experts can help you identify the right authority, prepare documents, and submit applications smoothly. Book a Free Consultation Call with Kustodian.Life

Documents Required to Apply for a Death Certificate

- Application form (available at the municipal office or online portal)

- Medical certificate of cause of death issued by a hospital/doctor

- Aadhaar card of the deceased (if available)

- Proof of birth of the deceased (if available)

- Proof of residence (ration card, Aadhaar, voter ID, etc.)

- Identity/address proof of the applicant (family member/legal heir)

- Copy of the cremation/burial receipt (in some states)

Pro Tip: Don’t just request one copy. Most banks, insurers, and authorities will ask for an original or attested copy. It’s best to obtain 10-15 certified copies at the start to avoid repeated trips later.

2. Will, Nominee, and Succession Planning

One of the most important steps after a loved one’s passing is understanding how their assets will be passed on. This can feel overwhelming, but knowing the rules helps avoid future disputes and ensures that the family is financially secure.

If a Registered Will Exists

- A will is a legal document that clearly states how the deceased wanted their assets to be distributed.

- The executor (the person appointed in the will) is responsible for carrying out these wishes.

- Assets mentioned in the will are transferred accordingly, and in case of conflicts, the will takes precedence over nominee declarations.

If There Is No Will

- In the absence of a will, succession laws apply:

- Assets are distributed among legal heirs as per these laws.

Nominee vs Legal Heir – A Common Confusion

- A nominee is simply a trustee or caretaker of assets, not the final owner.

- Ultimate ownership goes to legal heirs, unless the will specifically grants rights to the nominee.

- For example, if a father names his son as a nominee in a bank account, but leaves a will distributing assets equally among children, the bank will release funds to the nominee, but the son must later share with other heirs as per the will or law.

If There Is No Will or Nominee

- In such cases, heirs must apply for a Succession Certificate from the district court.

- This certificate allows the legal heirs to claim movable assets such as bank deposits, bonds, shares, and mutual funds.

- For immovable assets (like land, house, property), heirs may need a legal heir certificate or a probate process, depending on the state laws.

Release Deed – When an Heir Gives Up Rights

- Sometimes, one legal heir may voluntarily give up their share in an asset.

- In such cases, a Release Deed is drafted and registered with the sub-registrar, confirming that they have no claim over the asset.

- This is common when heirs want assets transferred to one member (for example, a widowed parent).

Business Owners – Special Note

- If the deceased was a businessperson, succession planning becomes critical.

- Check whether there was a succession plan or a partnership deed specifying how the business will continue.

- If not, heirs may need to decide on succession or appoint new partners/directors to ensure business continuity.

| Scenario. | Key Points | Documents / Legal Process |

| If a Registered Will Exists | - Will specifies asset distribution.- Executor carries out wishes.- Will overrides nominee declarations. | Registered Will, Executor’s authority, Probate (if required). |

| If No Will (Succession Laws Apply) | - Distribution as per personal laws:• Hindus, Sikhs, Buddhists, Jains → Hindu Succession Act, 1956.• Christians & Parsis → Indian Succession Act, 1925.• Muslims → Muslim Personal Law (Shariat).. | Legal heir certificate / Probate (as per state law). |

| Nominee vs Legal Heir | - Nominee = trustee, not final owner.- Ultimate ownership rests with legal heirs.- Nominee must hand over assets as per will/law. | Nominee details, Will (if available), Legal heir certificate (if required). |

| If No Will or Nominee | - Legal heirs must apply for succession rights.- Covers movable assets (bank deposits, bonds, shares, mutual funds).- Immovable assets (property, land) may require a probate/legal heir certificate. | Succession Certificate (district court), Legal Heir Certificate. |

| Release Deed | - Used when an heir voluntarily gives up a claim.- Registered with the sub-registrar.- Common for transferring full rights to one heir (e.g., widowed parent). | Release Deed (registered). |

| Business Owners | - If a succession plan/partnership deed exists, follow it.- If not, heirs must decide succession or appoint new partners/directors. | Succession Plan / Partnership Deed / Corporate legal process. |

Pro Tip: Keep copies of the will, succession certificate, and other related documents safely in one folder. Clear documentation avoids conflicts and ensures faster transfer of assets.

It’s also important to understand the difference between a nominee and a legal heir. Learn more about how nominees and successors are treated under Indian law in this guide.

3. Inform Key Institutions About the Death

After obtaining the death certificate and reviewing succession documents, the next step is to officially inform all relevant institutions about the passing of your loved one. This prevents misuse of their identity, stops unwanted charges, and ensures a smooth transfer of benefits or closure of accounts.

Here are the key institutions you must notify:

1. Banks and Financial Institutions

- Inform the bank where the deceased held accounts by submitting the death certificate and a request for settlement.

- If there is a nominee or joint account holder, the claim process is straightforward.

- If not, legal heirs may need to provide a succession certificate or a legal heir certificate.

- Don’t forget to notify banks of locker accounts, recurring deposits, or loans in the deceased’s name.

2. Insurance Companies

- If the deceased had a life or health insurance policy, the insurer must be notified as early as possible.

- Submit the claim form, death certificate, and supporting documents to start the claim settlement.

- Remove the deceased’s name from family health insurance plans to avoid premium mismatches.

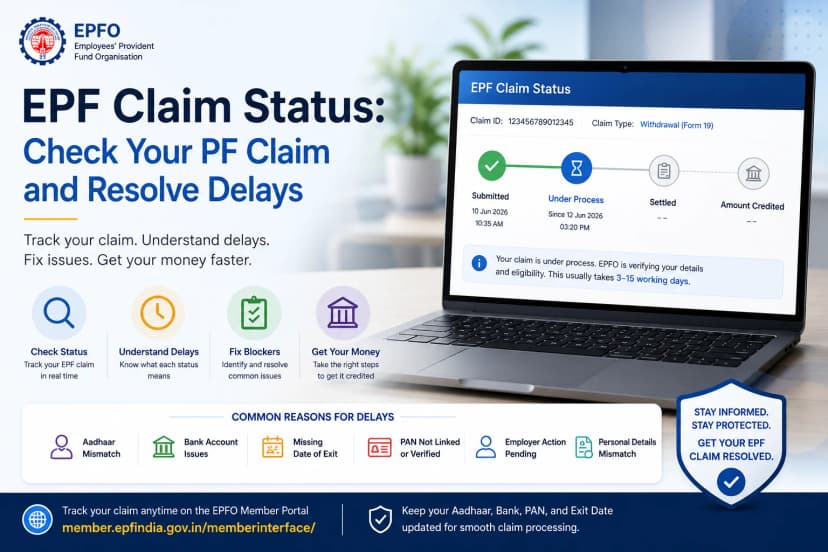

3. Employees’ Provident Fund Organisation (EPFO)

- If the deceased was a salaried employee, EPF, pension, and insurance benefits may be claimed.

- Common forms include:

- These must be filed with the employer or directly at the EPFO office, along with the death certificate and nominee/heir details.

| Form | Purpose | Who Can Apply | Supporting Documents |

| Form 20 | EPF (Provident Fund) Settlement | Nominee / Legal Heir | Death Certificate, ID proof, and Bank details of the claimant |

| Form 10D | Monthly Pension (EPS) | Eligible Spouse / Children | Death Certificate, Marriage Certificate (for spouse), Birth Certificate (for children) |

| Form 5IF | EDLI (Employees’ Deposit Linked Insurance) Claim | Nominee / Legal Heir | Death Certificate, Employer’s certification, ID & Bank details of claimant |

If you need help claiming EPF after a loved one’s death, this step-by-step guide walks you through EPF login, withdrawal, and settlement processes.

4. Income Tax Department

- The deceased’s final Income Tax Return (ITR) must be filed by their legal representative.

- After all tax liabilities are cleared, the PAN card should be surrendered to the department.

- This prevents future misuse or fraudulent activity in the name of the deceased.

5. UIDAI (Aadhaar)

- Aadhaar is not deactivated after death.

- However, to avoid misuse, it is advisable to lock the biometrics through the Aadhaar portal or app.

6. Voter ID and Passport

- Submit a cancellation request for the voter ID at the local election office.

- For the passport, send the death certificate and passport details to the regional passport office to ensure it cannot be misused.

7. Driving License

- Visit the local RTO (Regional Transport Office) to cancel the driving license of the deceased.

- This helps prevent identity theft or fraudulent use.

Pro Tip: Make a checklist of all institutions your loved one was associated with, such as banks, insurance, telecom services, utilities, and government IDs. Informing them early avoids unnecessary bills, fraud, or complications later.

4. Banking & Financial Accounts

One of the first financial matters that families need to address is the settlement of bank accounts and deposits. The process depends on whether a nominee, joint holder, or only legal heirs are involved.

- If a nominee is registered, → The nominee can claim the funds directly by submitting the death certificate, ID proof, and bank forms.

- If it’s a joint account, → The surviving account holder can continue operating the account. However, the bank may ask for updated KYC documents.

- If there is no nominee or joint holder, → Legal heirs must obtain and submit a Succession Certificate (from the district court) or a Legal Heir Certificate (issued by local authorities) to claim the funds.

Important Note: If the deceased had a salary, pension, or any pending income, it’s best to wait until all expected credits are deposited before closing the account. Closing it too early can lead to delays in receiving these payments.

Locker Access

If the deceased had a bank locker:

- RBI rules allow nominees or surviving joint holders to access the locker after proper verification.

- This access is conditional and usually requires the death certificate, ID proofs, and a bank declaration form.

- If no nominee exists, heirs will need a succession certificate to gain access.

5. Insurance Claims

Insurance is often the financial cushion families rely on after the loss of a loved one. Initiating claims early helps avoid delays and ensures funds are received smoothly.

- Life Insurance: Inform the insurer immediately and submit the claim form along with essential documents such as the death certificate, original policy bond, and proof of relationship/identity. Once verified, insurers are mandated to settle valid claims within a set timeframe (usually 30 days).

- Health Insurance: If the deceased was covered under a family floater plan, it’s important to remove their name from the policy to avoid premium miscalculations and future claim issues.

- Government-Linked Schemes: Many families forget that low-cost schemes like the Pradhan Mantri Suraksha Bima Yojana (PMSBY) and Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) are often auto-enrolled via the deceased’s bank account. Checking for these can bring additional financial support.

Pro Tip: Always keep a copy of the claim acknowledgement from the insurance company. It acts as proof in case of disputes or delays.

6. Investments & Securities

Investments, whether in mutual funds, stocks, or deposits, form a significant part of an individual’s financial legacy. Settling them properly ensures that nominees or legal heirs receive the rightful benefits without complications.

- Mutual Funds, Shares, Bonds: If a nominee is registered, they can directly claim the proceeds by submitting the death certificate and KYC documents. In the absence of a nominee, legal heirs must obtain a succession certificate or probate of a will from the court.

- Demat Accounts: For shares held in a demat account, the transfer is handled through CDSL/NSDL (the depositories). Nominees can apply for the transmission of securities by submitting the prescribed forms along with supporting documents.

- Recurring Deposits / SIPs: Any standing instructions for recurring deposits or SIPs need to be stopped or closed by notifying the concerned bank or Asset Management Company (AMC). This avoids unnecessary deductions.

- Unclaimed Investments: Sometimes dividends, matured bonds, or shares remain unclaimed. Families should check the IEPF (Investor Education and Protection Fund Authority) portal, where such investments are transferred after a certain period of inactivity.

Pro Tip: Track all investments of the deceased by checking Consolidated Account Statements (CAS) from depositories (NSDL/CDSL) and cross-verifying with banks for any linked SIPs or deposits.

7. Liabilities & Debts

Along with assets, families must also take care of the financial obligations of the deceased. Handling liabilities promptly prevents legal hassles and ensures a smooth settlement of the estate.

- Credit Cards: Inform the bank immediately to deactivate the card and stop further charges. Any outstanding dues must be cleared from the estate of the deceased, not from the heirs’ personal funds.

- Loans (Home, Car, Personal):

- Subscriptions & Bills: Cancel ongoing services such as phone bills, streaming services, utilities, or club memberships to avoid unnecessary charges.

- Income Tax Dues: The deceased’s legal representative must file the pending income tax return and clear any dues before distributing assets among heirs. This step is important to avoid penalties and future disputes.

Pro Tip: Create a checklist of the deceased’s liabilities (credit reports, loan accounts, utility bills) so nothing is overlooked. This helps close accounts systematically.

8. Assets & Property Transfer

Transferring assets of a deceased loved one can feel overwhelming, but following the right process ensures smooth ownership changes and avoids future disputes.

Families should gather all related documents early and proceed systematically.

- Collect Property-Related Documents: Begin with title deeds, sale agreements, tax receipts, vehicle RCs, and share certificates. These will be needed for legal and transfer procedures.

- Movable Assets (jewellery, investments, bank balances): Can be transferred to nominees or legal heirs using a will (if available) or through a succession certificate from the court.

- Immovable Assets (land, house, flat): Require mutation of property records in the local municipal office and registration with the sub-registrar. This ensures the heir’s name is reflected in government records for future sales or loans.

- Vehicle Transfer: Ownership transfer of cars, bikes, or commercial vehicles is done at the RTO. Legal heirs must provide a succession certificate or NOC from other heirs, along with the death certificate and RC.

- Unclaimed Assets: Families often overlook dormant assets. Check for:

Pro Tip: Keep a consolidated record of all properties and movable assets. This not only helps during inheritance but also reduces the chance of assets remaining unclaimed in the future.

When transferring assets and property, it’s important to plan carefully to avoid legal complications or disputes among heirs. To ensure you don’t make common mistakes, check out our guide on the 5 estate planning mistakes most Indians make.

Essential Documents Checklist

| Document. | Where to Obtain | Purpose / Use |

| Death Certificate | Municipal authority / Panchayat / Online state portal | Mandatory for all financial & legal claims (insurance, bank, EPF, property, tax, etc.) |

| Medical Certificate of Cause of Death | Hospital / Doctor | Required while applying for the death certificate |

| Will (if registered) | Registrar's office / Family records | Guides asset distribution as per the deceased’s wishes |

| Succession Certificate | District Court | Required to claim movable assets (bank deposits, bonds, shares, mutual funds) in the absence of a will |

| Legal Heir Certificate | Local Tehsildar / Municipality | Establishes relationship of heirs; used for property transfer, government benefits |

| Release Deed (if applicable) | Sub-Registrar Office | Used when a legal heir voluntarily gives up their share of the inheritance |

| Bank Documents (Passbook, Locker Agreement, FD receipts) | Concerned Bank | Required to claim deposits, operate/close accounts, or access lockers |

| Insurance Policy Documents | Insurance company / Agent | To claim life/health insurance and government schemes (PMJJBY, PMSBY) |

| EPF / Pension Forms (Form 20, 10D, 5IF) | Employer / EPFO Office | For the settlement of provident fund, pension, and EDLI insurance benefits |

| PAN Card (of deceased) | Income Tax Department | Needed for final ITR filing; later surrendered to prevent misuse |

| Aadhaar Card (of deceased) | UIDAI | Biometrics to be locked to avoid misuse (not deactivated officially) |

| Property Papers (Title deed, Tax receipts, Sale deed) | Registrar / Municipal Office / Family records | For mutation, the transfer of immovable property |

| Vehicle RC & Insurance | RTO / Insurer | Needed for the transfer of vehicle ownership |

| Passport & Voter ID | Passport Office / Election Office | Cancellation prevents identity misuse. |

| Loan / Credit Card Statements | Concerned Bank / NBFC | To settle outstanding dues from the estate or claim insurance cover, if available |

| Utility Bills & Subscriptions | Service providers | For closure/cancellation to avoid charges |

| Consolidated Account Statement (CAS) | NSDL/CDSL / AMC | Helps identify mutual funds, SIPs, and securities held by the deceased |

| IEPF Claim Forms | Investor Education and Protection Fund Authority | To recover unclaimed dividends, matured deposits, or shares |

To stay fully updated on all EPFO reforms, including PF and pension changes this year, check out our detailed guide on EPFO Rule Changes 2025: Complete Summary of New PF & Pension Reforms.

Conclusion

Losing a loved one is emotionally overwhelming, and dealing with financial and legal formalities during this time can feel like an additional burden. However, being aware of the key steps, from obtaining the death certificate to claiming insurance, settling bank accounts, transferring property, and checking for unclaimed assets, ensures that families can secure what rightfully belongs to them without unnecessary delays or disputes.

The most important thing is to stay organised, keep documents handy, and act promptly. Wherever possible, involve nominees, update KYC details, and maintain a family finance folder so that future processes become smoother.

At the end of the day, financial closure is not just about paperwork; it’s about safeguarding your family’s stability and honouring your loved one’s legacy. And if you ever feel lost, remember that expert guidance is available to simplify the journey and help you recover what is rightfully yours.

The Kustodian Bridge

At Kustodian.life, we help families reclaim unclaimed EPF, insurance, bank deposits, and other financial assets, while providing compassionate guidance on inheritance, succession, and estate planning.

Losing a loved one is never easy, and dealing with financial matters during such a time can feel overwhelming. From claiming funds to managing inheritance, every step comes with its own challenges. You don’t have to go through it alone; we’re here to support you with care and clarity.

Our team will guide you step by step, so you can manage claims and finances smoothly, while focusing on what truly matters: being there for your family.

Remember, thoughtful financial handling after a loss not only secures your family’s future but also honours the legacy of the one you’ve lost. We’re here to help you make that transition with clarity and care.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.