EPF Withdrawal for NRIs via EPFO Online Portal (2026 Guide)

- Buragadda Praneet

- Mar 23

- 7 min read

For most Non-Resident Indians (NRIs), the Employees’ Provident Fund (EPF) is often the last remaining financial tie to India. By 2026, the EPFO (Employees' Provident Fund Organisation) will have transitioned almost entirely to the current EPFO digital claim processing framework, which processes most claims electronically.

While this makes the process lightning-fast for residents, it creates a "digital wall" for NRIs who have outdated KYC or non-functional Indian SIM cards. This guide helps you determine whether you can scale that wall online or need to take the traditional embassy-attested route. We don’t just provide steps; we provide the 2026 logic required to get your money into your NRO account without a single trip to India.

Contents

1: Can You Actually File EPF Withdrawals For NRIs Online?

1: Can You Actually File EPF Withdrawals For NRIs Online?

The Mandatory Checklist (The 'Golden Five')

Before you spend hours trying to remember your password, you must meet these five criteria. If even one is missing, the online portal is a dead end.

UAN Activation: Your Universal Account Number must be active. If you haven't logged in for 5+ years, your account may be "locked" and require a manual unlock from your last employer.

Aadhaar-UAN Linkage (Verified): In the 'Manage' tab, your Aadhaar must show a green checkmark.

ActivAadhaar-linked mobile number: You must be able to receive an OTP. In 2026, most international telecom providers support Indian SMS via roaming, but "DND" (Do Not Disturb) filters often block government short-codes.

Approved NRO Bank KYC: Your bank account must be an NRO (Non-Resident Ordinary) account. EPFO systems allow credit only to Indian bank accounts. In practice, NRIs must use an NRO account, as NRE accounts typically do not accept such domestic income credits.

Service History Alignment: Your "Date of Joining" and "Date of Exit" must be updated by your employer. If the "Date of Exit" is blank, the system will assume you are still working and reject a "Full Settlement" claim.

To understand the logic behind these instant rejections, read our deep-dive into the 2026 EPFO Digital Reforms."

2: The 2026 Process – Step-by-Step Execution

Phase 1: The Pre-Audit

Log in to the EPFO Member e-Sewa Portal. Do not go straight to the claim section.

Check 'Service History': Ensure there is no overlap in dates between two different employers. Overlaps are the #1 cause of "Technical Rejections" in 2026.

Verify Bank IFSC: Following the massive Indian bank mergers of the early 2020s, many old IFSC codes are invalid. Ensure your KYC reflects the current, post-merger IFSC.

"Service overlaps usually happen when you have multiple UANs that haven't been merged correctly. Use our Step-by-Step Guide to Merging Multiple UANs to unify your service history before you file."

Phase 2: Filing the Claim

Navigate: Go to 'Online Services' → 'Claim (Form-31, 19, 10C & 10D)'.

Bank Verification: Enter the last 4 digits of your NRO account. The system will run a real-time check against the NPCI (National Payments Corporation of India) database.

The "Purpose" Selection: For NRIs, you will typically see Form 19 (PF Withdrawal) and Form 10C (Pension Withdrawal).

Note: In 2026, if you have more than 10 years of service, you cannot withdraw the Pension via Form 10C; you must apply for a Scheme Certificate.

Phase 3: The Aadhaar OTP Gateway

Once you click "Get Aadhaar OTP," the 2026 system gives you a 10-minute window.

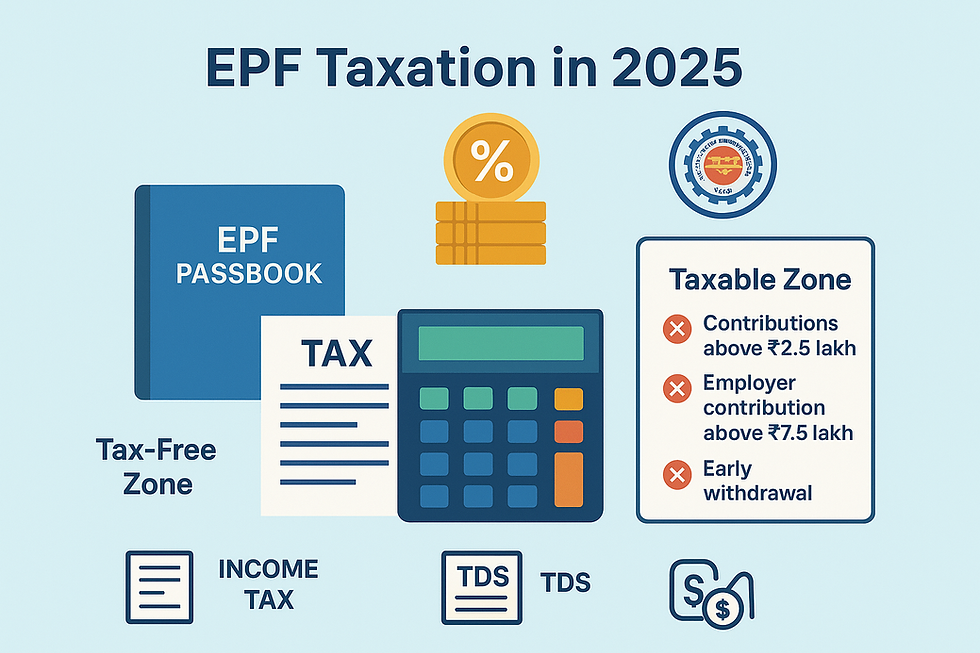

3: Tax Implications (The NRI Lens)

1. The 5-Year Benchmark & Section 195

Your assessment of the 5-year threshold is correct, but the NRI-specific TDS rate has a specific hierarchy.

Service > 5 Years: Fully exempt. Principal and interest (accrued during service) remain tax-free in India under Section 10(12).

Service < 5 Years: The "30% + Surcharge + Cess" (~34.6%) you mentioned is the default for NRIs under Section 195.

The Section 192A Conflict: Strictly speaking, Section 192A (the EPF-specific TDS rule) prescribes 10% if a PAN is provided. However, although Section 195 applies to payments to NRIs in general, EPF withdrawals are governed by Section 192A. If PAN is furnished, TDS is deducted at 10% for premature withdrawals.

Service Length | Resident Status | TDS Rate (with PAN) | Actual Liability |

5+ Years | Resident / NRI | 0% | Exempt |

< 5 Years | Resident | 10% | Slab Rate |

< 5 Years | NRI | 10 % | 34.6%* |

Correction: The "Pro Tip" is vital. By submitting Form 10F and a TRC, you can indeed invoke DTAA to bring the rate down to 10%–15% (depending on your country of residence), effectively bypassing the 31.2%+ rate.

2. Post-Resignation Interest: The 2026 Audit

You are correct that interest earned after your last working day is a major focus of the Under the current EPFO digital claim processing framework.

The Rule: The exemption under Section 10(12) only applies to the "accumulated balance" due to the employee at the time of cessation of employment. Any interest earned thereafter is "Income from Other Sources."

The "Idle" Account: While the account remains "active" (earning interest) until age 58, the tax-free status of that interest ends when you stop being an employee.

Automatic Deduction: As per CBDT clarification, interest earned after cessation of employment may be taxable. However, TDS deduction practices may not always separately segment this component.

3. Form 15G/15H: The Legal Trap

Your warning here is 100% accurate and critical.

Resident Only: These forms explicitly require you to declare you are a "Resident."

Penalty: This is considered a "false statement" under Section 277, which can lead to a demand notice and a penalty of 200% of the tax sought to be evaded.

4. Recourse: The ITR Route

If you missed the DTAA filing and were taxed at the higher rate:

ITR-2 is Mandatory: NRIs cannot file ITR-1. You must file ITR-2 (or ITR-3 if you have business income).

"Invoking DTAA is no longer a manual process; as of 2026, where required, Form 10F must be filed electronically on the Income Tax portal. See our NRI EPF Taxation Guide for a walkthrough on how to avoid the 31.2% TDS trap."

4: Troubleshooting the "Middle-Tier" Failures

1. The "Employer is No Longer Functional" Issue

If your KYC is not approved and your old company has shut down, the online route dies. You must transition to the "Attestation Route," where a Bank Manager or Gazetted Officer certifies your identity.

2. Name Mismatch (The 'Middle Name' Crisis)

If your Aadhaar says "Rajesh Kumar Sharma" but your EPF records say "Rajesh Sharma," the 2026 AI bot will reject the claim instantly.

The Fix: You must file a Joint Declaration Form (now available digitally on the portal for some establishments) to align the names before filing the withdrawal.

3. The "Pending with Employer" Loop

If your bank KYC is stuck as "Pending," the EPFO cannot pay you. Even if you are abroad, you must contact your HR in India. In 2026, employers have a statutory timeline to approve these, but many smaller firms ignore the alerts.

5: Online vs. Offline – When to Switch Lanes?

Stop trying the online method if:

You have tried and failed OTP 3+ times.

Your mobile number linked to Aadhaar is an old Indian number you no longer possess. (Changing this requires a biometric update in person in India, or a complicated virtual update if you have a valid Indian passport).

Your EPF account is from the "Pre-UAN" era (pre-2014) and has never been linked to a UAN.

The Offline (Embassy) Route: This involves downloading the Composite Claim Form (Non-Aadhaar), filling it out, and getting it attested by the Indian Embassy in your country of residence. This is then couriered to the specific EPFO office in India. While slower (30–60 days), it bypasses all digital OTP/KYC hurdles.

"If you are opting for the Embassy route, ensure you are using the 'Non-Aadhaar' Composite Form. For a downloadable checklist of the exact documents needed for consulate attestation, visit our NRI Withdrawal Hub."

Conclusion: Strategy Over Speed

The 2026 EPFO portal is a powerful tool, but it is not a "fix-all." For an NRI, the goal shouldn't be to file the claim as quickly as possible; it should be to file it once.

If your digital records are clean, they are typically processed within 3–10 working days, subject to verification. If they aren't, every "Retry" button you click adds weeks of technical locks to your profile. Audit your KYC, check your roaming.

How We Can Help

EPFO Stress? Consider it handled. Living in a different time zone makes dealing with the EPFO nearly impossible. Kustodian Life acts as your local advocate to resolve:

Stuck Claims: We breathe life into stalled applications.

Jurisdictional Hurdles: We navigate the red tape across different regions.

End-to-End Resolution: No more midnight calls or chasing paperwork.

"Don’t wait for a rejection letter to find out your KYC is flawed. Use our Free EPF Audit to scan 50+ parameters of your account from name mismatches to service overlaps and get a report in under 2 minutes."

6: Frequently Asked Questions

Q: Can I withdraw EPF into my foreign (e.g., US/UK/UAE) bank account?

A: No. Payments are only made to NRO or Resident accounts in India. You can then repatriate those funds via your bank’s NRO-to-NRE/Foreign account transfer process (Form 15CA/CB required).

Q: How does the EPFO know I am an NRI?

A: They don't unless you select "Settlement Abroad" as your reason for exit or provide an NRO bank account. However, your tax liability is determined by your residential status, not what you tell the EPFO.

Q: Can an NRI withdraw their EPF balance without visiting India?

A: Yes. In 2026, the EPFO system will allow for 100% online withdrawals via the UAN Member e-Sewa portal. As long as your UAN is activated, linked to Aadhaar, and you can receive OTPs on your registered mobile, you can process the entire claim from abroad.

Q: Can I receive my EPF proceeds in a foreign bank account or NRE account?

A: No. Under Indian FEMA and EPFO regulations, proceeds can only be credited to a Non-Resident Ordinary (NRO) bank account or a Resident account. EPFO credits are made only to Indian bank accounts. In practice, NRIs must use an NRO account. Direct credit to foreign or NRE accounts is not supported under the current system

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary by individual record.

Comments