EPF Guide for Indian Employees: Login, Withdrawals, Transfers, Grievance & More (2026)

Introduction: Why EPF Matters

If you’re a salaried employee in India, understanding your Employees’ Provident Fund (EPF) and Provident Fund (PF) is crucial for financial security. EPF isn’t just a deduction it’s your financial lifeline. Yet, most of us stare at that "PF" line on our payslips, confused by jargon and paperwork. This guide cuts through the noise, helping you turn EPF from a mystery into a powerful tool for retirement security, emergency funds, and tax savings.

This comprehensive guide will walk you through every aspect of EPF and PF from your first job to withdrawals, transfers, and beyond. Real-life stories, step-by-step instructions, and practical tips will make your EPF journey smooth and stress-free.

What’s Inside?

- Chapter 1: What is EPF? The Guide to Your Retirement in India

- Chapter 2: The Basics: Understanding EPF, PF, and UAN

- Chapter 3: Getting Started: UAN Creation and Activation

- Chapter 4: EPFO Login, EPF Member Login, and Passbook Portal Guide

- Chapter 5. Checking Your PF Balance: All the Ways to Track Your PF

- Chapter 6. EPF Passbook: How to Download and Understand Your EPF Passbook

- Chapter 7. Transfer and Claim Your PF Money: EPF Withdrawal & Online Claims

- Chapter 8. PF Claim Status: Tracking and Troubleshooting

- Chapter 9. KYC, Bank Updates, and Profile Management in EPF

- Chapter 10. Grievances: When Things Go Wrong

- Chapter 11. PF Real-Life Stories and FAQs

- Chapter 12. Conclusion: Your PF/EPF Journey- What’s Next?

Chapter 1: What is EPF or PF? The Guide to Your Retirement in India

India has more than 29 crore PF accounts, yet only a fraction of us truly understand how it works or how to benefit from it. This blog walks you through everything from your first salary deduction to withdrawing funds in a human, jargon-free way.

What is EPF?

The Employees’ Provident Fund (EPF) is a government-backed savings scheme for employees in India. It’s managed by the Employees’ Provident Fund Organisation (EPFO), a statutory body under the Ministry of Labour and Employment.

How does it work? Each month, you and your employer contribute a portion of your salary (typically ₹1800 or 12% of Basic + DA) to your EPF account. This money grows over time with tax-free interest.

Why Should You Care about EPF?

- Automatic Basic + DA Savings: Ensures consistent savings.

- Good Returns: Historically offers 8-8.25% interest.

- Low Risk: Government-backed, providing security.

- Tax Benefits: Contributions, interest, and withdrawals (after 5 years) are tax-free.

- Emergency Fund: Allows withdrawals for specific needs (medical, marriage, home).

- Retirement Security: Provides financial stability after your working years.

Confused about how your employer’s PF share is split?

Talk to a Kustodian.Life expert to understand your EPF and EPS contributions clearly.

Chapter 2: The Basics: Understanding EPF, PF, and UAN

Your EPF contribution is typically 12% of your basic salary plus Dearness Allowance (DA). While part of your Cost to Company (CTC), this amount is deducted and doesn't come to you as in-hand salary. In effect, an equivalent amount is also contributed by your employer.

EPF isn't just one thing; it has three parts:

| Component | Employee Contribution | Employer Contribution | Purpose |

| EPF | 12% of Basic + DA | 3.67% | Retirement savings |

| EPS | - | 8.33% | Pension after 58 |

| EDLI | - | 0.5% | Life insurance |

Understanding Each Component

- EPF (Provident Fund): The main retirement savings account.

- EPS (Pension Scheme): Provides a monthly pension after age 58, subject to eligibility.

- EDLI (Insurance): Offers life insurance cover (up to ₹7 lakhs) to your nominee if something happens to you while in service.

What is a UAN?

The Universal Account Number (UAN) is a unique 12-digit ID for every EPF member. It's like a central hub linking all your EPF accounts from different jobs. Think of it this way: the UAN acts as an umbrella, and each job's EPF account has its own Member ID under that umbrella. When you switch jobs, your new employer links the new Member ID to your existing UAN. If you already have a UAN, you must provide it to your new employer so they can link your new Member ID to it.

Key Points About UAN:

- Permanent: It stays the same throughout your career.

- Centralized: Links all your EPF accounts.

- Essential: Needed for all online EPF services (balance, withdrawal, transfer).

- Post-2014 Compulsory: If you worked before 2014, you might need to get one.

How does the Employees Provident Fund Organisation (EPFO) work?

Established in 1952, the Employees' Provident Fund Organisation (EPFO) is a government body managing mandatory provident fund, pension, and insurance schemes for India's organized sector. It's a major social security organization.

A Quick History: Starting with an ordinance in 1951 and the EPF Act in 1952, the EPFO initially covered factories but now includes over 180 industries. Key developments include the EPS in 1995 and the UAN in 2014.

Inside the EPFO: A tripartite Central Board of Trustees oversees the schemes. Led by the Central Provident Fund Commissioner, the EPFO operates through regional and sub-regional offices. Its functions include enforcing the EPF Act, managing accounts, settling claims, investing funds, and ensuring compliance. Currently, there's a strong focus on digital services and grievance handling.

If you notice missing contributions or discrepancies in your passbook, Kustodian.Life can perform a free EPF audit to track and fix issues for you.

Chapter 3: Getting Started: UAN Creation and Activation

Before you can do anything with your EPF online, you'll need your Provident Fund (PF) number. Your employer provides this; check your payslips or ask HR/Finance. Keep this number handy.

If You Don’t Have a UAN

- New Employees: Your employer is responsible for generating your UAN when you join. This is done through the EPFO Employer Portal and is mandatory before your first PF contribution.

- If you haven’t received your UAN:

Check Your UAN Status (If You Suspect You Have One):

- Go to the EPFO Member e-SEWA portal: https://unifiedportal-mem.epfindia.gov.in/memberinterface/

- Click on "Know Your UAN Status."

- Fill in the required details: your state, EPFO office area, and your PF number. Your PF number is typically structured like [Region Code]/[Office Code]/[Establishment Code]/[Extension (if any)]/[PF Number]. For example: KN/BN/364734/000/35772. Leave the "Ext" field blank if your PF number doesn't have one.

- Click "Check Status."

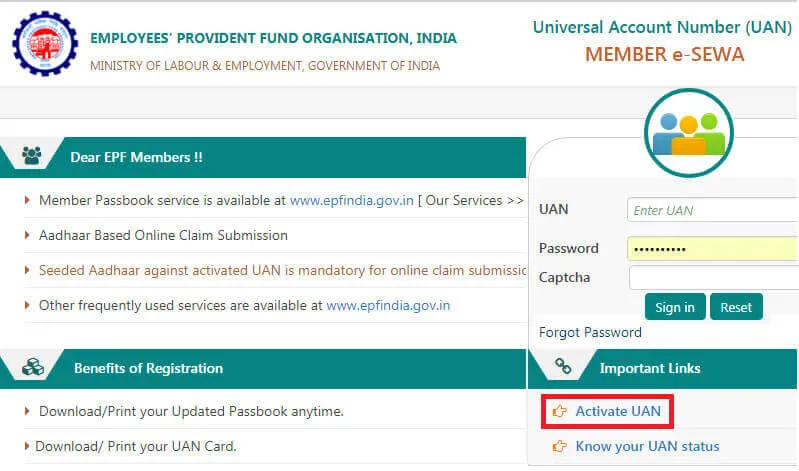

How to activate your UAN for the first time (portal, SMS, UMANG app)

Once you have your UAN, you need to activate it on the EPFO portal to access your account online.

- Go to the UAN Member portal: https://unifiedportal-mem.epfindia.gov.in/memberinterface/

- Click "Activate UAN."

- Enter your UAN, registered mobile number, and PF account details (from Step 1 if you checked status, or as provided by your employer).

- Click "Get Authorization Pin." You'll receive an OTP.

- Enter the OTP and click "Submit." Your UAN is now active.

- You'll be prompted to fill in your Name, Father's Name, and Date of Birth (ensure they match official records) and create a password.

- Update Your KYC Details (Highly Recommended): After activation, log in to the EPFO portal using your UAN and new password and update your KYC information. This includes linking your Aadhaar, PAN, bank details, and other documents. Updated KYC ensures smooth online transactions in the future. Look for the "Edit Your KYC" link after logging in.

If you are still facing issues with UAN activation, read the common problems and solutions here

UMANG APP Integration

In 2026, the traditional "Paper-based" or even "OTP-only" era of EPF is evolving. The EPFO Face Auth system, integrated into the UMANG App is now the gold standard for secure, self-service UAN management.

Read how to activate or generate UAN through the UMANG App.

Chapter 4: EPFO Login: EPF Member login and Passbook Portal Guide

It's important to know there are two main EPFO portals:

- Member Portal: For taking actions like raising claims and submitting joint declarations.

- Passbook Portal: Primarily for viewing and analyzing your passbook and understanding claim rejection reasons.

Logging into the EPFO Member Portal (for Claims and Declarations)

- Go to: https://unifiedportal-mem.epfindia.gov.in/memberinterface/

- Enter your UAN.

- Enter your password.

- Enter the OTP received on your registered mobile number.

- Click "Sign In".

Once logged in, you can access various online EPF services.

Logging into the EPFO Passbook Portal (for Passbook Analysis)

- Go to: https://passbook.epfindia.gov.in/MemberPassBook/Login

- Enter your UAN.

- Enter the same password you use for the Member Portal.

- Type the captcha code.

- Click "Login".

After logging in, you can view and download your EPF passbook for all linked Member IDs.

Resetting your password if you’re locked out

If you can't access your account, you can only reset your password through the EPFO Member Portal. This new password will also work for the Passbook Portal, but it might take up to 24 hours to be effective there.

Steps to Reset Your Password:

- Go to the EPFO Member Portal: https://unifiedportal-mem.epfindia.gov.in/memberinterface/

- Click "Forgot Password".

- Enter your UAN and follow the on-screen instructions.

- Verify your identity using the Aadhaar OTP.

- Set your new password after successful verification.

If you are still facing issues with log in to the EPFO portal, read the common problems and solutions here.

Chapter 5. Checking Your PF Balance: All the Ways to Track Your PF

How to check your PF/EPF balance: portal, SMS, missed call, UMANG app

Staying updated on your Provident Fund (PF) balance is crucial for your financial planning. The EPFO provides several convenient methods to do this. Ensure your UAN is activated and your mobile number is registered for most of these services.

Methods to Check Your PF Balance:

| Method | How to Use | Key Points |

| EPFO Passbook Portal | 1. Visit passbook.epfindia.gov.in2. Login with UAN, password, captcha3. Select Member ID to view | Official portal for detailed transaction history |

| UMANG App | 1. Download the app2. Register with your mobile3. Find EPFO services4. Enter UAN, verify OTP | Convenient smartphone solution |

| SMS Service | Send SMS to 7738299899:EPFOHO UAN <LAN> | Available in multiple languages |

| Missed Call Service | Give a missed call to 9966044425 | Quick method, no internet needed |

How to check the PF balance for trust or Exempted Establishments

Standard EPFO online services won't work for these. Here's how to check:

- Internal Portal: Check if your company has an internal online portal for HR/payroll information, including PF balance. Contact HR for login details.

- HR Department: Reach out to your HR or Finance department directly for your PF balance and transaction statement.

- Pay slips: Some exempted establishments might include PF details on your monthly pay slips.

Key Differences for Exempted Establishments VS EPFO-managed Pension:

- PF is managed by the company's trust, not directly by EPFO.

- No direct access via standard EPFO online services.

- Rely on internal company systems and HR communication.

- UAN is still applicable, but won't grant access on standard EPFO portals.

How often is your PF balance updated, and interest credited?

- PF Balance Updates: Generally updated monthly after employer contributions.

- Interest Calculation: Calculated monthly on the running balance.

- Interest Crediting: Credited annually at the end of the financial year (around March 31st). Delays in actual crediting can occur due to the process involved. It might take some time for the interest to reflect in your passbook.

Chapter 6. EPF Passbook: How to Download and Understand Your EPF Passbook

Why Check Your Passbook? Like Anuj, who spotted missing employer contributions and resolved it promptly, regular passbook reviews are crucial for ensuring your EPF is on track.

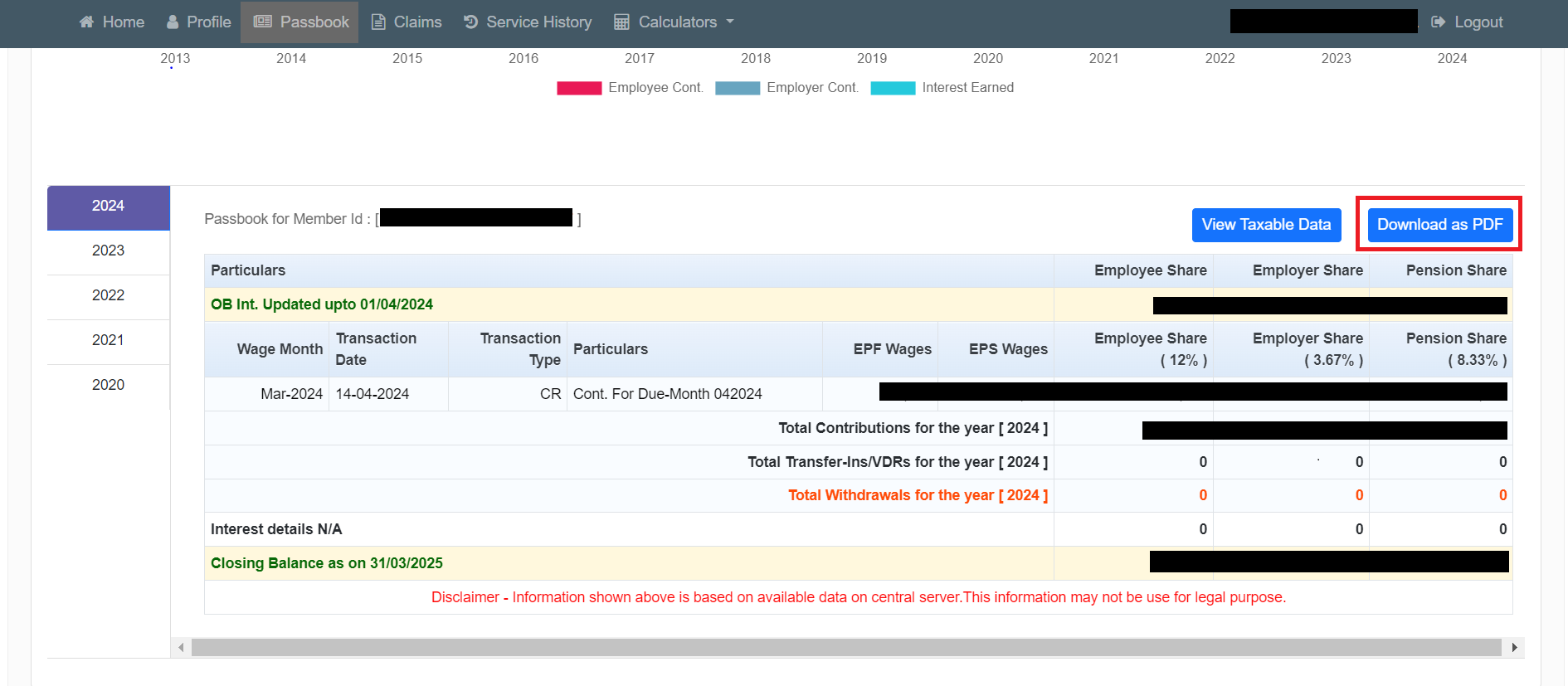

How to Get Your EPF Passbook:

- Go to the EPFO Passbook Portal.

- Enter your UAN and password (same as the Member Portal).

- Select the relevant employer/Member ID.

- You can now view the passbook entries and choose to download

Understanding the PF Passbook Entries:

| Entry Type | What It Means |

| Employee Share | Your monthly 12% contribution to the EPF. |

| Employer Share | The 3.67% of the employer's contribution that goes to your EPF account. |

| Pension Contribution | 8.33% of the employer's contribution is directed to the EPS (Pension Scheme). |

| Interest | The annual interest credited to your PF account by the EPFO. |

| Date | The date the specific transaction or credit occurred. |

| Transfer | Indicates funds transferred into or out of this specific Member ID. |

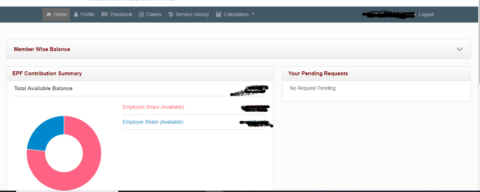

Summary Section (Often at the end):

| Term | Description |

| Opening Balance | Funds carried forward from the previous accounting period |

| Total Employee Contribution | The cumulative amount deducted from your salary towards PF |

| Total Employer Contribution | Combined employer payments (excluding EPS contributions) |

| Total Interest Received | Accrued interest on PF balance from government-set rates |

| Total Withdrawal | The sum of all authorized withdrawals from your account |

| Closing Balance | Final account balance as of the passbook generation date |

Key Things to Check For:

- Consistency: Ensure regular monthly contributions from both you and your employer.

- Accuracy: Verify the correct spelling of your name and other personal details.

- Employer Details: Confirm that the employer information is accurate for each entry.

If you are still facing issues with the EPFO passbook portal, read the common problems and solutions here

Still not seeing your latest contributions in your passbook?

Let Kustodian.Life track and fix missing PF updates for you.

Chapter 7. Transfer and Claim Your PF Money: EPF Withdrawal & Online Claims

Knowing how and when to move or access your PF money is key to your financial planning. Here's a concise guide:

When Can You Transfer Your PF?

You can transfer your PF balance whenever you change jobs. The primary goal of transferring is to consolidate all your PF accumulations under a single UAN, allowing for continuous interest accrual and easier management. It is generally recommended to transfer your PF instead of withdrawing it upon changing jobs, especially if you plan to continue working. Transferring also helps in avoiding tax implications that might arise from premature withdrawals (before 5 years of continuous service).

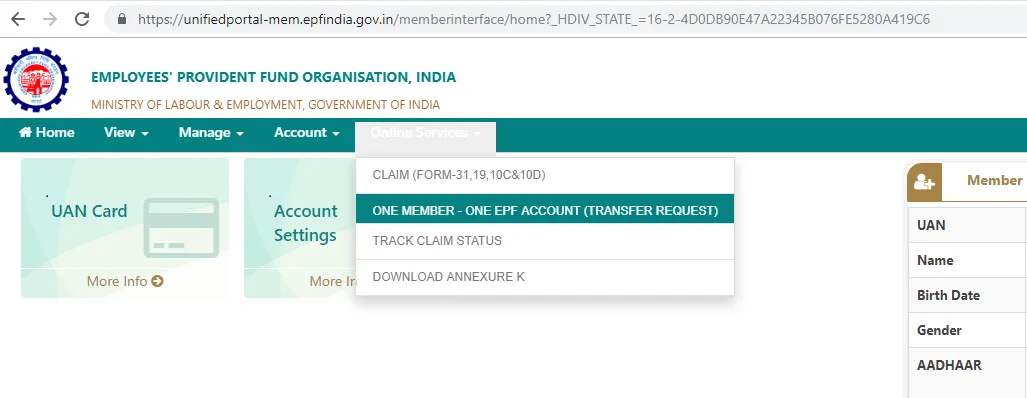

How to Transfer Your PF Online:

The online transfer process has been streamlined by the EPFO. Here's a general step-by-step guide:

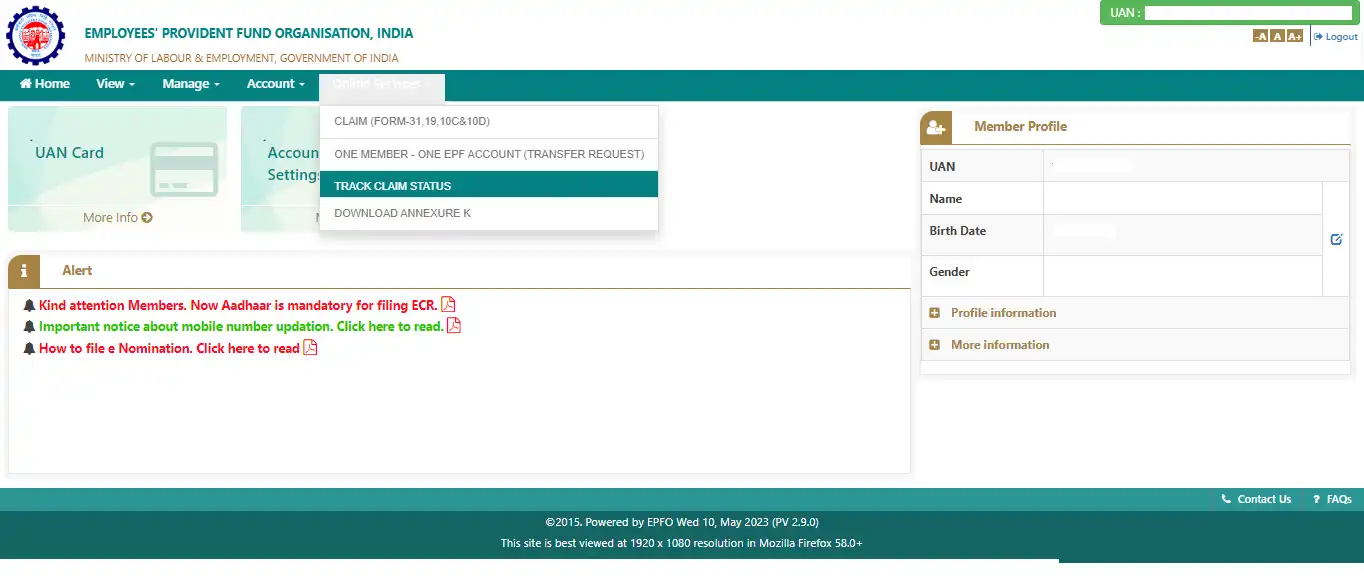

- Log in to the Member Portal: Visit https://unifiedportal-mem.epfindia.gov.in/memberinterface/ and log in using your UAN and password.

- Go to "Online Services" and select "One Member – One EPF Account (Transfer Request)."

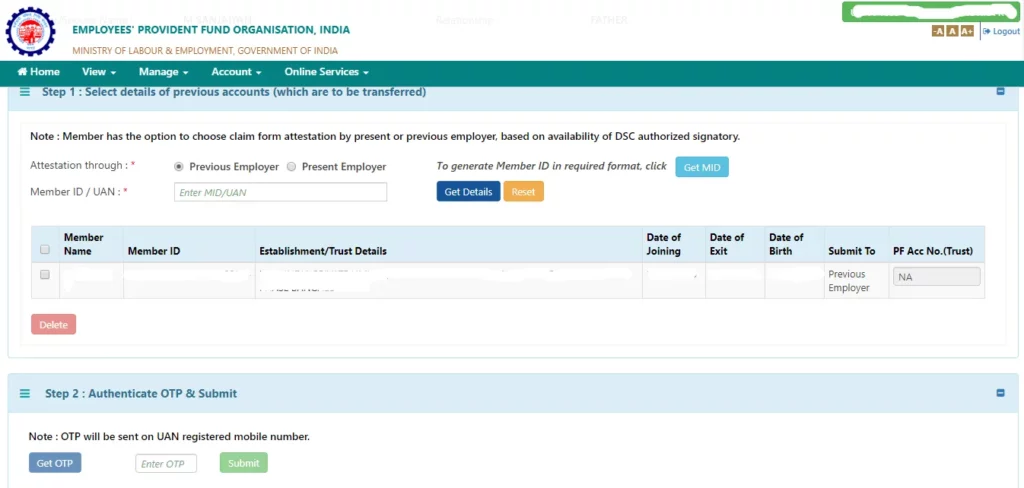

- Verify your details.

- Get details of your previous employment.

- Choose employer for attestation: You will have the option to choose either your previous or current employer.

- Submit with OTP.

- Note the Claim Reference Number to track status under "Track Claim Status."

You can track the status of your PF transfer online through the "Track Claim Status" option under the "Online Services" tab on the member portal.

Recently changed jobs and your PF isn’t showing up yet?

Kustodian.Life can help you transfer it seamlessly no employer follow-ups needed.

When can you withdraw your PF?

Generally, you cannot withdraw your PF while you are still employed. However, partial withdrawals are allowed under specific circumstances, and full withdrawal is permitted upon retirement or under certain conditions of unemployment.

Partial and Full Withdrawal of EPF

| Category | ||||

Note: Some people might consider this a loan against EPF, but there is no provision of the same.

Step-by-step: Filing an online claim

If you meet the eligibility criteria for withdrawal, you can file your claim online through the EPFO Member e-SEWA Portal:

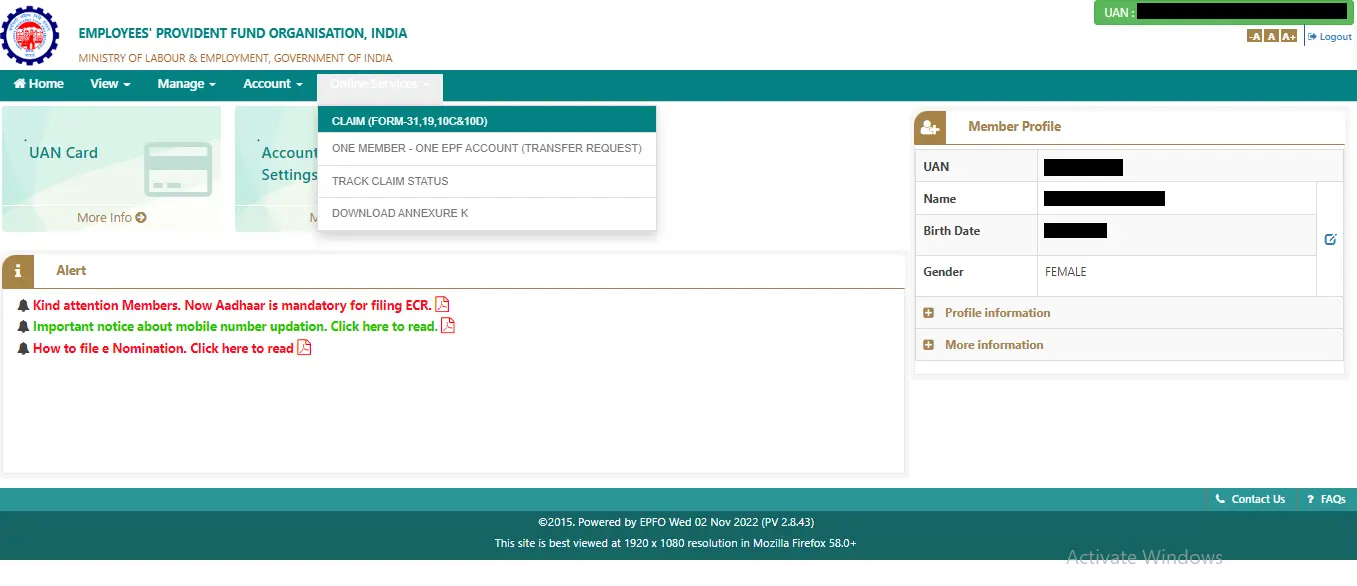

- Log in to the Member Portal: Visit https://unifiedportal-mem.epfindia.gov.in/memberinterface/ and log in using your UAN and password.

- Go to "Online Services" and select "Claim (Form-31, 19, 10C & 10D)."

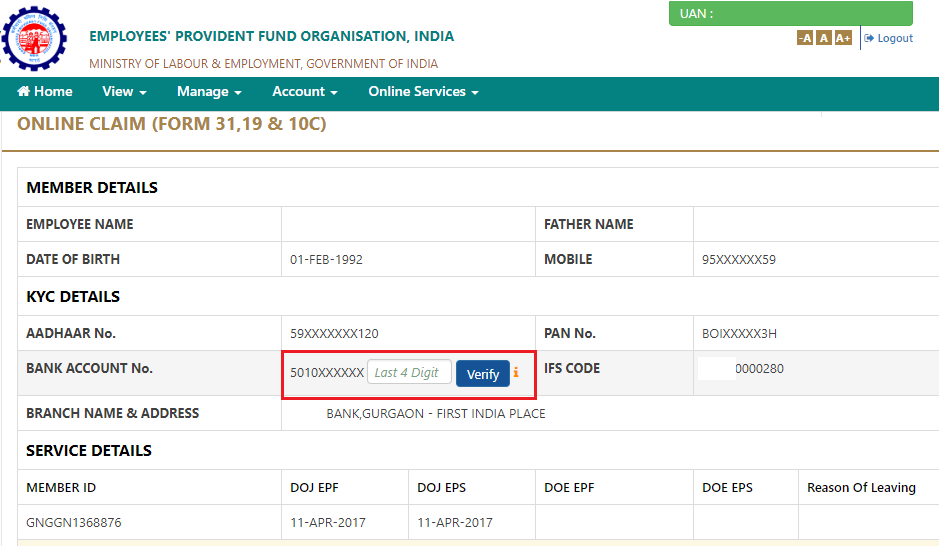

- Verify bank details and "Proceed for Online Claim."

- Select the claim type (e.g., PF Advance (Form-31), Full PF Settlement (Form-19)).

- Provide required details (purpose, amount, address, documents if needed).

- Read the undertaking and tick the declaration.

- Get Aadhaar OTP, enter it, and submit.

- Track claim status under "Track Claim Status." The amount credited to your bank account after processing.

Documents needed, forms (Form 19, 10C, 31), and eligibility

Key Forms for PF Withdrawal:

- Form 19 (Final Settlement): Full PF withdrawal upon retirement/resignation/termination (typically after 2 months of unemployment).

- Form 10C (Pension Withdrawal/Scheme Certificate): Withdraw EPS if less than 10 years service and under 58, OR get a Scheme Certificate to combine service later.

- Form 31 (PF Advance): Partial withdrawal for specific reasons while employed (eligibility and amount vary by reason).

Note: For trusts or exempted employers, the process is guided by the particular company; get in touch with HR.

If you are still facing issues with the EPF claims, read the common problems and solutions here.

Chapter 8. Claim Status: Tracking and Troubleshooting

Pavan's Pro Tip: A rejected claim due to incorrect Aadhaar details taught Pavan the importance of verifying all information before applying. Updating his KYC led to quick approval on his second attempt.

How to check your claim status online, via SMS, and UMANG

| Method | Steps | Key Notes |

| EPFO Member Portal | 1. Visit EPFO Member Portal2. Log in with UAN & password3. Click Online Services > Track Claim Status | Directly displays rejections and status |

| EPFO Passbook Portal | 1. Visit EPFO Passbook2. Log in with UAN & password3. Go to the claims section | Critical for spotting the rejection reason comments |

| SMS Service | 1. Send EPFOHO UAN <LAN> to 7738299899(e.g., EPFOHO 123456789000 ENG) | Generic status updates (e.g., "Claim rejected"); lack detailed reasons. |

| UMANG App | 1. Open the UMANG app > Search EPFO2. Select Employee Centric Services > Track Claim3. Enter UAN > Verify via OTP | Shows basic statuses; technical glitches may obscure rejection details. |

| Toll-Free Call | 1. Dial 14470 (24/7) or 1800118005 (9:15 AM–5:45 PM)2. Provide UAN/PF number | Limited to confirming rejection, agents cannot disclose specific reasons. |

Additional Insights:

- Missed Call Service: Give a missed call to 011-22901406 from a registered number for SMS updates.

- Offline Verification: Visit EPFO offices with UAN and ID proof for complex cases.

- Processing Time: Claims typically settle within 15–30 days if documents are valid.

What different claim statuses mean (under process, settled, rejected)

| EPF Claim Status | |

| The claim has been processed and accepted by EPFO | |

| Your claim could be rejected by your previous or current employer due to various reasons, such as:• Mismatch in details• Signature mismatch• In case you don’t submit the signed claim printout within 15 days of making an online claim |

What if the PF claim gets rejected?

A rejected claim can be frustrating, but it's essential to understand the reason and take corrective action:

- Check the Reason: The EPFO usually specifies the rejection reason on the online portal or via SMS/UMANG (the online portal often has more details). Understand why it was rejected.

- Fix the Issue: Correct the discrepancy based on the rejection reason. This might involve updating your KYC, correcting signatures, or resubmitting documents.

- Re-apply: Once corrected, resubmit your claim online via the member portal. For offline claims, submit a fresh, corrected form.

- Seek Help If Needed:

Note: Reach out to us at Kustodian.life, and we can guide and take you through the process and troubles

If you are still facing issues with the EPF claims, read the common problems and solutions here.

If your claim is “Rejected” or “Under Process” for too long

Reach out to Kustodian.Life to identify the issue and speed up your withdrawal.

If you’re stuck with PF delays, rejections, or missing contributions, book your free EPF audit with Kustodian.Life today and let our experts review your account end-to-end.

Chapter 9. KYC, Bank Updates, and Profile Management

Accurate KYC, bank details, and a well-managed profile on the EPFO portal are vital for smooth claim processing and withdrawals.

Why KYC is crucial for smooth PF claims

KYC is a mandatory process for verifying your identity and address. For EPFO, accurate and updated KYC details are essential for:

- Faster Processing: Verified KYC builds trust, allowing quicker claim approvals without manual checks.

- Direct Fund Transfers: Correct bank details ensure seamless credit of withdrawn amounts.

- Online Claim Convenience: Complete KYC enables paperless online claims via Aadhaar OTP.

- Fraud Prevention: Helps EPFO ensure benefits reach the right person and prevents misuse.

- Regulatory Compliance: KYC is a mandatory requirement for EPFO.

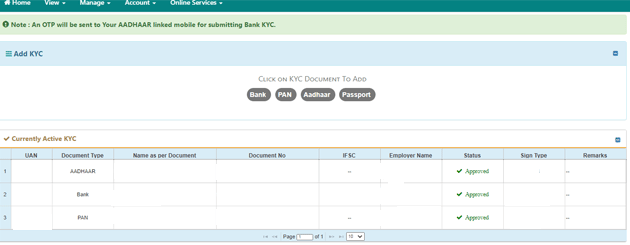

How to update Aadhaar, PAN, and bank details in EPFO

You can update your KYC details online through the EPFO Member e-SEWA Portal:

- Log in to the EPFO Member Portal.

- Click on the "Manage" tab.

- Select "KYC" from the dropdown.

- Update Details:

KYC Status:

| KYC Field | Status | Action if Not Verified |

| Aadhaar | Pending / Verified | Ensure the correct number is entered; employer approval is needed if pending. |

| PAN | Available / Verified / Mismatch? | Verify PAN details; correct if mismatched. Employer approval might be needed. |

| Bank | Verified (IFSC + correct account no) / Pending | Ensure the correct IFSC and account number are entered. Employer approval is needed if pending. |

Pro Tip: Keep your mobile number & email updated for OTPs and alerts.

If you are still facing issues with the EPF KYC, read the common problems and solutions here.

Chapter 10. Grievances: When Things Go Wrong

Even with efficient systems, PF issues can occur. Knowing how to file a grievance and escalate unresolved matters is key.

How to File a Grievance with EPFO:

You can file a grievance with the EPFO through both online and offline methods:

| Method | How To |

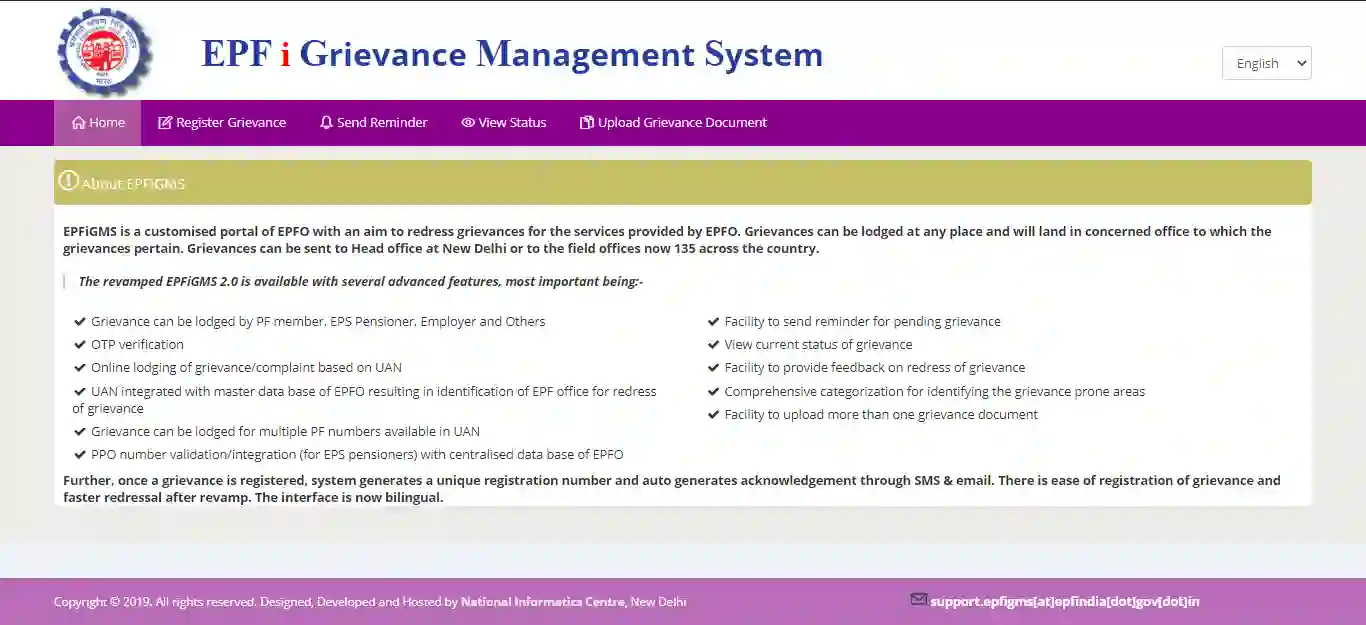

| Online EPFO Grievance Portal | 1. Visit https://epfigms.gov.in/2. Register your complaint with clear details and optional attachments. |

| By Phone | Call 1800 118 005 (all India) or 14470 (multilingual, 7 AM - 9 PM) |

| Via WhatsApp | Message EPFO WhatsApp help at 011-22901406 |

| Social Media | Tag @socialepfo on Twitter for quick replies |

| Offline (Written) | Submit a written complaint with your UAN, PF account number, contact details, and issue specifics with supporting documents to your nearest EPFO office |

Detailed Online Filing steps(EPFiGMS Portal):

This is the preferred and most efficient method.

- Visit the EPF i-Grievance Management System (EPFiGMS) Portal: Go to https://epfigms.gov.in/.

- Click "Register Grievance".

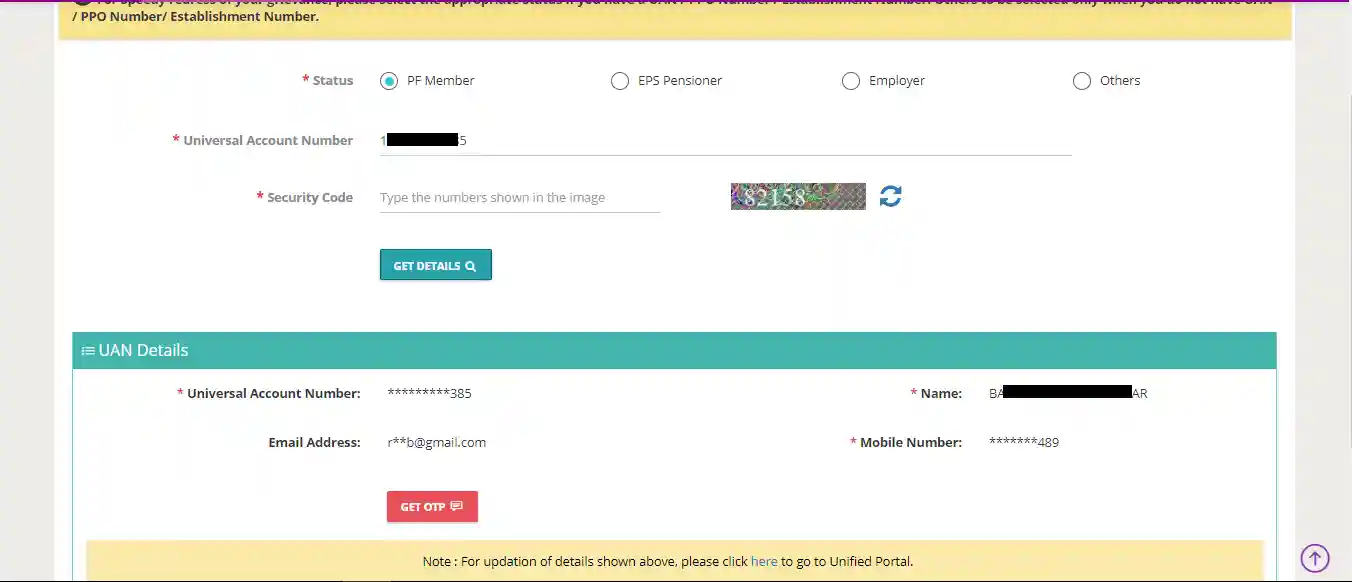

- Select your status (PF Member, Pensioner, or Employer).

- For PF members, enter UAN and security code, click "Get Details" (select "No" if no claim ID).

- Authenticate with the OTP sent to your registered mobile.

- Fill in your personal information.

- Select the relevant PF account number, grievance category, and sub-category (e.g., PF Withdrawal, Transfer, Passbook).

- Clearly describe your issue with relevant dates, amounts, and reference numbers.

- Optionally, attach supporting documents.

- Click "Submit". Note the grievance registration number received via SMS and email for tracking.

Pro Tip: Be aware that EPFO response times might not always be immediate due to workload.

If you are still facing issues with the EPF grievance, read more here.

Name or date mismatch delaying your PF claim?

Kustodian.Life can correct it quickly and get your PF released faster.

Chapter 11. PF Real-Life Stories and FAQs

Real user stories: What went wrong, how it was fixed

Aisha's Activation Agony: Finally Unlocking Her UAN

Lesson: Activate your UAN as soon as you receive it from your employer to avoid delays in accessing online services.

Vikram's Father's Name: A Painstaking Path to Withdrawal

Lesson: Ensure the accuracy of your personal details, including your parents' names, right from the start of your employment.

Sunita's Salary Surprise: Decoding the EPS Deduction

Lesson: Understand the specific rules governing EPF and EPS contributions, including the wage ceiling for EPS, to accurately interpret your passbook.

Most common PF/EPF questions answered simply

1. What is the current rate of interest on EPF deposits?

The EPF interest rate for 2024-25 is 8.15% per annum. This rate is reviewed and may change every financial year.

2. Is the interest earned on EPF taxable?

Interest is tax-free up to ₹2.5 lakh of your contribution per year (₹5 lakh if there is no employer contribution). If you contribute more, interest on the excess is taxable and reported separately by EPFO.

Edge Case: If you have both taxable and non-taxable accounts, interest is split and taxed accordingly.

3. What is the Employees' Deposit Linked Insurance Scheme (EDLIS) and how does it benefit me?

EDLIS is a group life insurance for EPF members. On the member’s death during service, nominees get up to ₹7 lakh. Employer pays 0.5% of basic + DA as premium.

4. Who is eligible for the Employees' Pension Scheme (EPS)?

All EPF members with a basic salary ≤ ₹15,000/month at joining are eligible. You must complete at least 10 years of service to get a pension at 58 years.

5. Can I withdraw my EPS contribution fully?

You can only withdraw EPS if you have less than 10 years of service and are not taking up further employment. Otherwise, you get a pension after 58 years.

Edge Case: If you leave before 10 years and later rejoin, your earlier service can be added if you take a Scheme Certificate.

6. What happens to my PF if my company shuts down?

You can still claim your PF. If employer attestation isn’t possible, you can get your claim attested by your bank manager or submit supporting documents directly to EPFO.

7. Can a nominee claim PF and EPS benefits in case of the member's death? What is the process?

Yes. Nominee/legal heir submits Forms 20 (PF), 10D (EPS), and 5IF (EDLIS) with required documents. If no nominee is registered, legal heirs must provide succession proof, which can cause delays.

8. How can I update my nominee details in EPFO records?

Log in to the Member e-SEWA Portal, go to "Manage" → "e-Nomination", and add/update details. No employer digital signature is required.

9. What are the tax rules on PF withdrawals before completing 5 years of service?

Withdrawals before 5 years are taxable. TDS at 10% if PAN is given, 30% if not. No TDS if the withdrawal is less than ₹50,000.

Edge Case: If you lose your job due to ill health, business closure, or employer shutdown, withdrawal may still be tax-free.

10. What happens to my PF if I move abroad (out of India) for employment?

Your PF continues to earn interest. You can keep the account active or withdraw as per NRI rules. Apply online if UAN and KYC are active, or submit a physical claim with NRE/NRO account details.

11. What is an inoperative PF account, and how can I reactivate it?

If no contributions are made for 36 months, the account becomes inoperative. Submit KYC and a reactivation request to EPFO.

Edge Case: In some cases, Interest continues to be credited even if the account is inoperative.

12. Are there any charges for withdrawing or transferring my PF online?

No, EPFO does not charge for online PF withdrawals or transfers.

13. How to link Aadhaar with EPF?

Log in to the Member e-SEWA Portal, go to "Manage" → "KYC", and update Aadhaar details.

Edge Case: If your name or date of birth does not match between Aadhaar and EPF, you must correct the discrepancies before linking.

Note: Reach out to us at Kustodian.life, in case you have more questions.

For more FAQ, read here

Chapter 12. Conclusion: Your PF/EPF Journey- What's Next?

Congratulations on navigating the intricacies of your Provident Fund! This journey through understanding your contributions, accessing your balance, transferring funds, claiming withdrawals, managing your KYC, and addressing grievances equips you to take control of a significant aspect of your financial future.

Still having trouble with your EPF account? Read our in-depth Troubleshooting Masterclass for practical fixes.

Recap: Why Your Active PF Engagement Matters

Your PF/EPF is a vital asset, offering:

- Retirement Security: Building a significant nest egg for your future.

- Long-Term Growth: Harnessing the power of compounding.

- Contingency Support: Providing access to funds for emergencies.

- Peace of Mind: Securing your financial future reduces worry.

Tips for Maximizing Your PF Retirement Savings:

- Transfer First: Always transfer PF when changing jobs to grow your corpus and avoid tax on premature withdrawals.

- Keep KYC Updated: Accurate KYC ensures smooth transactions and prevents claim rejections.

- Nominate Carefully: Update beneficiaries to ensure easy access to funds for your loved ones.

- Review Regularly: Monitor your passbook and claim status to stay informed and address issues promptly.

- Know Your Schemes: Understand EPF, EPS, and EDLIS benefits to make informed decisions.

Where to Get Help (Official Links, Trusted Advisors):

For any queries, assistance, or official information regarding your PF/EPF, rely on these trusted sources:

- EPFiGMS Portal (Grievances): https://epfigms.gov.in/

- EPFO WhatsApp Helpline: Check the official EPFO website for regional numbers.

- EPFO Toll-Free: 14470 and 1800 118 005.

- EPFO Social Media: Follow @socialepfo (Twitter) and /socialepfo (Facebook).

- Employer HR/Finance: Your first point of contact for many PF queries.

Note: Reach out to us at Kustodian.life, and we can guide and take you through the process and troubles

Final Thought:

Treat your PF account with the same attention you give your salary. Active engagement is key to securing your financial future with EPF as a reliable partner. Thank you for reading “Your Complete Journey Through EPF & PF: From Joining to Withdrawal” by Kustodian.life.

Share your PF experiences or questions below to help others!

If you’re stuck with PF delays, rejections, or missing contributions,

Book your free consultation with Kustodian.Life today and let our experts handle it end-to-end.

Disclaimer: While every effort has been made to ensure accuracy, EPF rules and regulations are subject to change. Please refer to official EPFO circulars for the latest updates.