NRI EPF Eligibility, FEMA Rules & Withdrawal Timing (2026 Guide)

- Muslehuddin Mohd

- Feb 9

- 9 min read

Updated: Mar 15

For most Indian professionals moving overseas, the EPF corpus represents a significant portion of their retirement savings. However, once your residency status changes to Non-Resident Indian (NRI) under Indian tax law and FEMA regulations, the way you interact with this account shifts.

While you are no longer permitted to make fresh contributions to your EPF, your existing balance continues to earn interest. The challenge and the opportunity lie in understanding the 2026 guidelines regarding:

Eligibility: Who can keep their account, and who must settle it.

FEMA Compliance: Why your bank account type (NRO vs. NRE) matters more than ever for legal repatriation.

Withdrawal Strategy: How to time your exit to minimise tax hits and maximize the power of your accumulated interest.

This guide breaks down the essential compliance steps to ensure your hard-earned savings transition as smoothly as you do.

Contents

1. “I’ve Become an NRI, What Happens to My EPF Now?”

For many professionals, EPF is the first long-term financial asset they ever built. Month after month, deductions happened quietly, balances grew in the background, and EPF became something you rarely thought about. That calm usually breaks the moment you move abroad.

Once you become an NRI, anxiety sets in quickly. People worry that EPF may suddenly become illegal, frozen, or non‑compliant. Some rush to withdraw without understanding the consequences, while others delay for years out of fear.

The most common questions we hear are:

Do I have to withdraw my EPF immediately after becoming an NRI?

Is it illegal to keep EPF once I start working abroad?

Will EPF stop earning interest once I leave India?

Can FEMA block my EPF money or repatriation later?

Here is the fundamental truth that resolves most of this panic:

Becoming an NRI does not make your EPF invalid. It only changes how and when you can withdraw, not your ownership of the money.

There is no automatic closure, no penalty, and no forced withdrawal just because you moved abroad. Your EPF balance remains protected under Indian law.

2. Who Is Considered an NRI for EPF Purposes?

Before any EPF rule is applied, one concept must be clear: tax residential status.

EPF rules do not follow nationality, passport, or visa category. They follow residential status under the Income‑Tax Act, which is determined every financial year based on your physical presence in India.

Status | What it broadly means | Why it matters for EPF |

Resident | Stayed in India beyond limits | Normal EPF rules apply |

RNOR | Transitional status (often on return) | Mixed tax and withdrawal treatment |

NRI | Stayed outside India | NRI‑specific withdrawal and FEMA routing |

Two clarifications remove most confusion:

EPF withdrawal eligibility follows employment exit rules, not citizenship or passport status.

Taxation and FEMA routing of EPF follow your residential status under the Income-Tax Act and FEMA at the time of withdrawal.

This is important because many people worked in India for years as residents, accumulated EPF, and became NRIs much later. EPF law recognises and allows this transition.

Calculating your exact residential status is the first step in avoiding 30% TDS. For a detailed breakdown of how tax residency impacts all your Indian retirement accounts, see our Comprehensive NRI PF & Retirement Tax Guide.

3. What Happens to EPF the Moment You Become an NRI?

Nothing dramatic happens automatically.

When you become an NRI:

Your EPF account does not close

Your accumulated balance remains fully protected

You are not required to withdraw immediately

The EPFO does not auto‑flag or penalise accounts merely because residential status changes.

Contributions after becoming an NRI

Contribution rules depend on employment, not location:

You may continue contributing only if you remain employed with an eligible Indian employer

You cannot contribute to EPF from foreign employment income

In practice, most NRIs stop contributing simply because their employment shifts abroad, not because EPF becomes invalid or restricted.

4. When Can an NRI Withdraw EPF?

Unlike resident Indians, EPF withdrawal rules are applied differently when Indian employment ends due to permanent relocation abroad.

In practice, EPFO permits immediate withdrawal when an employee exits Indian service for permanent settlement overseas or foreign employment. In such cases, the standard two-month waiting period applied to resident employees is generally not enforced.

Immediate Withdrawal: If you are leaving India to settle abroad permanently or for foreign employment, the 2-month waiting period is waived. You are eligible to apply for 100% of your EPF and EPS (pension) balance the moment your Indian employment ends.

The "Settling Abroad" Clause: On the EPFO portal, you must select "Settlement Abroad" as the reason for leaving. You will be required to upload a copy of your visa or residence permit as proof of your intent to relocate.

Reality Check: You don't withdraw because you are an NRI; you withdraw because you are terminating Indian service to settle overseas.

For NRIs, if the "Reason for Leaving" is marked as "Permanent Settlement Abroad," the 2-month waiting period is waived. They can file the claim on Day 1 after the employer updates the Exit Date

Plain framing: You withdraw EPF because employment ended and not because you became an NRI.

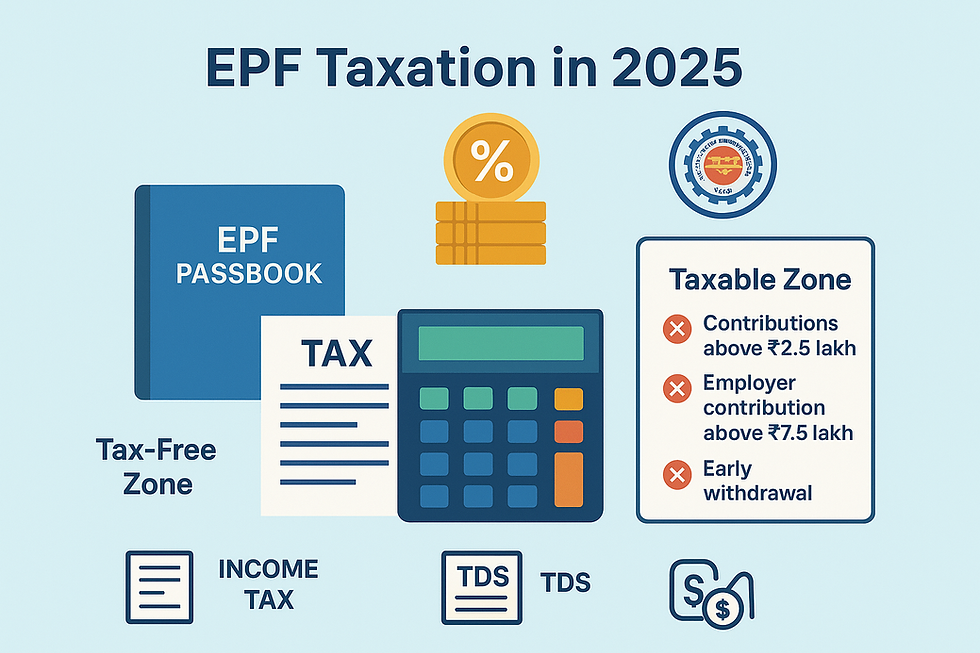

5. EPF Withdrawal Before vs After 5 Years (The Tax Trigger)

The 5-year rule is the most critical threshold for your pocket. It doesn’t dictate if you can take your money, but it heavily dictates how much the government keeps.

Feature | Withdrawal < 5 Years of Service | Withdrawal > 5 Years of Service |

Tax Status | Fully Taxable (as "Salary" income) | Generally Tax-Exempt |

TDS Rate (NRI) | 31.2% (Maximum Marginal Rate) | 0% (With proper documentation) |

Interest Earned | Taxed as "Income from Other Sources" | Tax-exempt |

Employer Share | Taxable | Tax-exempt |

Key 2026 Update: Unlike residents who can submit Form 15G to avoid TDS, NRIs are generally subject to a flat 30% plus cess (31.2%) TDS for early withdrawals. To reduce this, you may need to leverage DTAA (Double Taxation Avoidance Agreement) between India and your current country of residence.

DTAA and Form 10F – Practical Reality (2026): Indian tax law requires a valid Tax Residency Certificate (TRC) and Form 10F to claim DTAA benefits. While EPFO recognises DTAA relief in principle, there is currently no fully integrated EPFO system that automatically applies DTAA rates at source based on electronic Form 10F filings.

In many cases, NRIs may need to claim treaty benefits by filing an income-tax return in India, even if TRC and Form 10F are available.

6. FEMA Rules & EPF: The Repatriation Reality

FEMA does not govern your right to the money, but it strictly controls the path the money takes once it leaves the EPFO.

Mandatory NRO Routing: By law, the EPFO cannot credit funds into a foreign bank account or an NRE account. The money must land in an NRO (Non-Resident Ordinary) account.

Repatriation Limits: Once the money is in your NRO account, you can transfer it to your foreign country under the USD 1 Million Management Scheme.

Compliance Needs: To move the money from your NRO to your foreign account, your bank will require Form 15CA and 15CB (certified by a CA) to prove that all Indian taxes on the EPF withdrawal have been paid.

7. EPF Interest After Becoming an NRI

A widespread myth is that EPF interest stops the moment you leave India. This is incorrect.

Interest Accrual:

EPF balances generally continue to earn interest as notified by the government until the account is settled, subject to EPFO operational rules applicable at the time. Interest does not stop merely because contributions have ceased or because residential status has changed.

Tax Treatment of EPF Interest:

EPF interest is normally tax-exempt until withdrawal. However, a specific exception exists for interest earned on employee contributions exceeding ₹2.5 lakh in a financial year (made while the individual was employed in India). Interest on this excess portion is tracked separately by EPFO and taxed annually under “Income from Other Sources,” regardless of whether withdrawal occurs after five years. Apart from this limited exception, EPF interest is not taxed annually simply because a member becomes an NRI.

8. What NRIs Are Allowed vs Not Allowed to Do With EPF

Allowed | Not Allowed |

Withdraw EPF when eligible | Contribution from foreign salary |

Keep EPF without immediate withdrawal | Treat EPF like NRE funds |

Repatriate EPF as per FEMA | Ignore residential status updates |

Use NRO routing compliantly | Assume automatic repatriation |

This table captures practical boundaries without diving into process complexity.

9. 4 Common Misunderstandings (NRI EPF Myths vs Reality)

Common Myth | The 2026 Reality |

"I have to wait 2 months to apply." | False. NRIs can apply immediately under the "Settling Abroad" provision. |

"I can use my NRE account for credit." | False. FEMA 2026 regulations strictly require an NRO account; NRE credits will be rejected. |

"EPF becomes illegal if I don't withdraw." | False. It is your property. You can leave it there, but interest earned post-exit will be taxable. |

"I can submit Form 15G to avoid TDS." | False. Form 15G is for residents. NRIs must use DTAA (Tax Treaties) and PAN to manage a 31.2% TDS risk. |

FEMA regulations in 2026 strictly prohibit retirement credits to NRE accounts. Ensure your KYC reflects a valid NRO account to avoid rejection. Check our NRI Banking & KYC Compliance Checklist to verify your account status.

10. How Eligibility Decisions Affect the Entire EPF Journey

Eligibility is not just a starting checkbox; it shapes the entire EPF lifecycle for an NRI, from how smoothly your claim is processed to how easily money is repatriated later. Decisions made (or ignored) at this stage often determine whether EPF withdrawal feels routine or becomes a source of prolonged stress.

When eligibility is clearly understood and planned early, several downstream benefits follow:

Withdrawal claims move faster because employment status, service period, and exit conditions align cleanly with EPFO rules

Tax and TDS exposure can be anticipated, allowing time to plan around the 5-year rule, documentation, and reporting

Correct bank accounts (usually NRO) are used from the beginning, reducing rejections or reprocessing

FEMA repatriation becomes procedural, as routing and compliance are already aligned

When eligibility is misunderstood or ignored, problems rarely appear immediately. Instead, they surface much later, often at the withdrawal stage, when timelines are tight, and correction options are limited. At that point, even small eligibility gaps can lead to delays, excess TDS, or blocked remittances.

11. When Eligibility Questions Need Expert Review

While many EPF cases are straightforward, some situations benefit from expert review because small errors can have disproportionate consequences.

Professional review is usually advisable when:

Residential status changed mid-financial year

RNOR status creates mixed tax or FEMA treatment

The service period is short, but the EPF corpus is large

Employer guidance conflicts with EPFO or bank advice

In such cases, a structured review helps align EPF rules, FEMA compliance, and withdrawal timing before irreversible steps are taken.

Many NRIs lose access to their PRAN or UAN because of expired mobile numbers or outdated KYC. If you are locked out of your portal, follow our 2026 Troubleshooting Guide for NRI Portal Access to regain control.

Useful Links & Official Resources

EPF Portal & Member Services

Employees' Provident Fund Organisation Member Portal:https://unifiedportal-mem.epfindia.gov.in/memberinterface/

EPFO Official Website:https://www.epfindia.gov.in

UAN Activation & Account Services:https://unifiedportal-mem.epfindia.gov.in/memberinterface/

Track EPF Claim Status:https://passbook.epfindia.gov.in/MemberPassBook/Login

EPF Forms & Download Links

Form 19 – Used for final EPF settlement after leaving employment Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form19.pdf

Form 10C – Used to claim withdrawal benefits or obtain an EPS scheme certificate Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form10C.pdf

Form 31 – Used for partial PF advance withdrawal (medical, housing, education, etc.)Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form31.pdf

Form 15G – Declaration to avoid TDS on PF withdrawal (applicable only for residents)Details: https://www.incometax.gov.in/iec/foportal/help/how-to-file-form15g

Form 10F – Required to claim DTAA (Double Taxation Avoidance Agreement) benefits Details: https://www.incometax.gov.in/iec/foportal/help/how-to-file-form10f

FEMA & NRI Banking Regulations

Reserve Bank of India FEMA Regulations:https://www.rbi.org.in/scripts/Fema.aspx

RBI Guidelines for NRO & NRE Accounts:https://www.rbi.org.in/commonman/English/Scripts/FAQs.aspx?Id=52

RBI Remittance Rules for NRIs (USD 1 Million Scheme):https://www.rbi.org.in/Scripts/FAQView.aspx?Id=115

Income Tax & DTAA Resources

Income Tax Department of India Official Portal:https://www.incometax.gov.in

DTAA (Double Taxation Avoidance Agreements) List:https://incometaxindia.gov.in/Pages/international-taxation/dtaa.aspx

Tax Residency Certificate (TRC) Information:https://www.incometax.gov.in/iec/foportal/help/tax-residency-certificate

12. FAQs

Can an NRI keep EPF without withdrawing?

Yes. There is no legal requirement to withdraw EPF immediately after becoming an NRI. EPF can be held until withdrawal eligibility is triggered.

When can an NRI withdraw EPF?

After Indian employment ends. In cases of permanent settlement abroad or foreign employment, EPFO generally permits immediate withdrawal once the employer updates the exit date.

Does EPF earn interest after becoming an NRI?

Yes. Interest does not stop immediately and continues for a defined period as per the EPF scheme rules.

Is EPF governed by FEMA?

Yes, but FEMA governs routing and repatriation, not ownership or withdrawal eligibility.

Does the 5‑year EPF rule apply to NRIs?

Yes. The 5‑year rule affects tax treatment, not eligibility or legality of withdrawal.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.

Comments