In the world of personal finance, few things are as frustrating as seeing a substantial number in your account but being told you can only touch a fraction of it. If you’ve ever logged into the EPFO portal, seen a healthy PF balance, and then had your withdrawal claim rejected or "short-settled," you aren’t alone.

As we navigate 2026, the Employees' Provident Fund Organisation (EPFO) has introduced several reforms to make the system more flexible. However, the fundamental gap between what you have and what you can take remains a major point of confusion for millions of salaried employees.

This guide clarifies the difference between the PF balance and withdrawable amount and explains exactly how much can be withdrawn from a PF account under the latest 2026 guidelines.

1. My PF Balance Is ₹ X. Why Is EPFO Allowing Less?

It is a common Monday morning realisation for many: You check your EPF passbook, see a balance of, say, ₹5,00,000, and plan a major expense. But when you go to file a claim, the portal only allows you to apply for ₹1,50,000.

This leads to an immediate sense of being "short-changed." You might wonder, "It’s my money, deducted from my salary. Why is the government holding it back?"

The reality is that employees often view the PF account as a regular savings account. It isn't. It is a defined-contribution retirement scheme. The mismatch between your total balance and your withdrawable amount is not a system error or an attempt by the EPFO to "keep" your money. It is a built-in regulatory feature designed to protect your 60-year-old self from your current self's immediate needs.

2. PF Balance vs Withdrawable Amount (The One-Minute Explanation)

If you are in a hurry, here is the "cheat sheet" to distinguish between the two terms:

| Term | Meaning |

| PF Balance | The total accumulation of your contributions + employer contributions + interest in your account. |

| Withdrawable Amount | The specific portion of that total balance that EPFO rules allow you to access at this exact moment. |

Key Line to Remember: PF balance is a number. The withdrawable amount is a decision based on your life circumstances.

Check your eligible withdrawal amount!

3. Why PF Balance ≠ Withdrawable Amount

To understand the difference, you have to look at the philosophy of the Provident Fund.

Retirement-First System

The "P" in PF stands for Provident, which implies providing for the future. The system is architected to ensure that by the time you reach the age of 58, you have a "corpus" (a large sum) to sustain you without a monthly salary. If the EPFO allowed 100% liquidity at all times, most people would deplete their accounts for lifestyle choices, leaving them vulnerable in old age.

Exception-Based Withdrawals

Withdrawals are treated as "advances" or "settlements." Unlike a bank account, where you can withdraw ₹500 just because you want to, the EPFO requires a reason (e.g., medical, marriage, housing). Each reason has its own "cap." For example, for a medical emergency, you might only be allowed to take 6 months of basic wages, regardless of whether your balance is ₹10 Lakh or ₹50 Lakh.

Preventing Early Depletion

In 2026, the EPFO has intensified its focus on the Power of Compounding. Even a small withdrawal early in your career can reduce your final retirement corpus by lakhs of rupees due to lost interest. The rules act as a "speed bump" to keep your money growing.

Read the detailed guide on EPF withdrawal rules 2026 in India

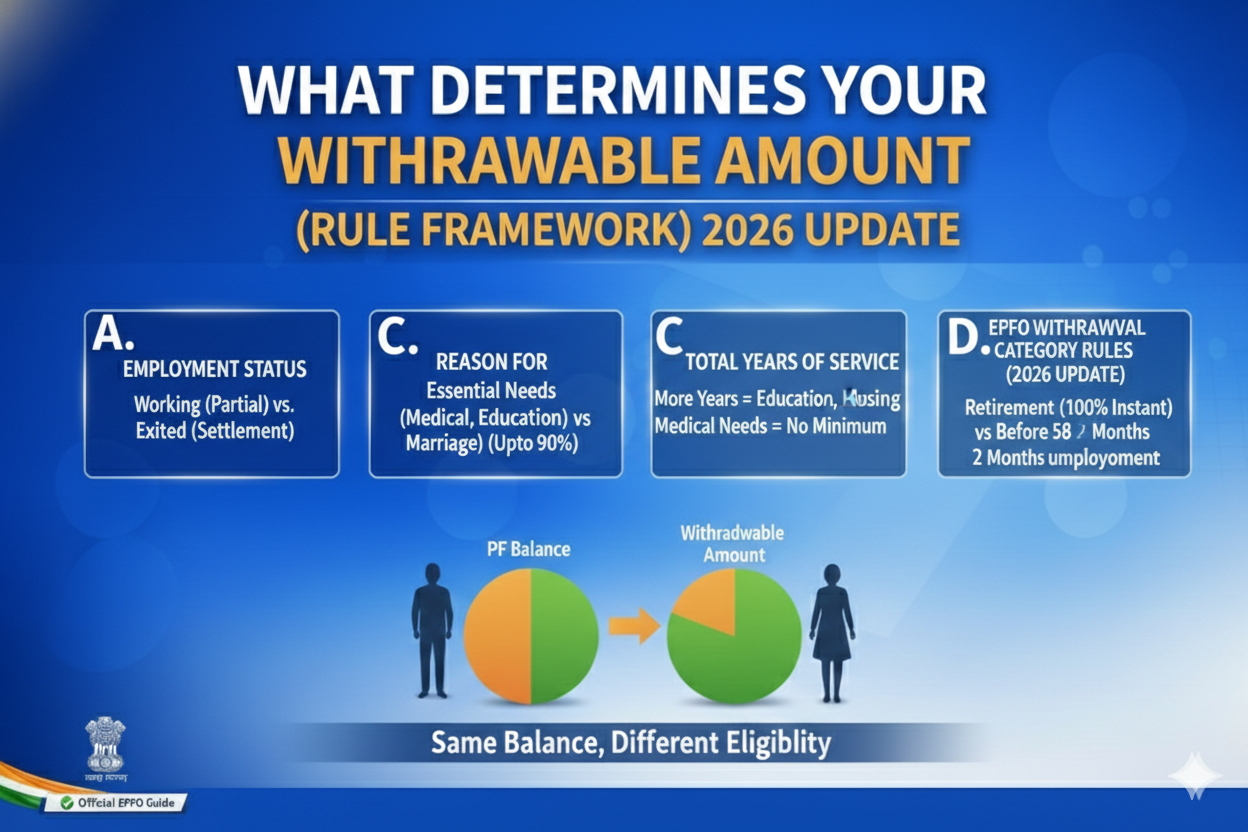

4. What Determines Your Withdrawable Amount (Rule Framework)

In 2026, four specific pillars determine exactly how much you can pull out of your account; employment status, reason for withdrawal, total years of service, and EPFO withdrawal category rules.

A. Employment Status (Working vs. Exited)

Are you currently on a company's payroll? If yes, you are only eligible for "Partial Withdrawals" or "Advances." If you have left your job and have been unemployed for a specific period, you enter the "Settlement" phase, which opens up more of your balance.

B. Reason for Withdrawal

The "Why" matters more than the "How Much."

- Essential Needs: (Medical, Education, Marriage) usually allow access to a percentage of the employee's share.

- Housing: Allows access to a much larger portion (up to 90%), but requires more years of service.

C. Total Years of Service

EPFO allows access to partial withdrawal under various categories requiring a minimum service period. However, the amount you can withdraw for medical treatment requires no minimum service period.

D. EPFO Withdrawal Category Rules (2026 Update)

You can apply instantaneously for your pf withdrawal after retirement upto 100%. Full withdrawal before age 58 requires 2 months of unemployment.

EPFO Withdrawal Rules Table

| Reason for Withdrawal | Minimum Service Required | Maximum Amount Allowed |

| Medical Treatment | No minimum requirement | Lower of 6 months' basic + DA OR the employee's total share with interest. |

| Education (Self/Children) | 7 years | Up to 50% of employee's share only. (Only 3 times in a lifetime) |

| Marriage (Self/Siblings/Children) | 7 years | Up to 50% of employee's share only. (Only 3 times in a lifetime) |

| Housing/Land Purchase | 5 years | Up to 90% of total balance (Employee + Employer share). Must be for self, spouse or Joint ownership. (Only 1 time withdrawal) |

| Home Renovation | 5 years after house purchase | Up to 12 months' Basic + DA OR employee share with interest OR cost of renovation. |

| Unemployment/ After retirement | 1 month (for 75%) | 75% of total balance after 1 month; 100% after 2 months. |

5. Common Scenarios: Balance vs. Actual Withdrawable Amount

Let's look at how this works in real-life situations without getting bogged down in math.

Scenario A: While Still Employed

If you are currently working and need money for a wedding, your PF Balance might be ₹10 Lakh. However, your Withdrawable Amount will likely be limited to 50% of your contribution only. The employer’s contribution and the remaining 50% of yours stay locked.

Scenario B: After Leaving a Job (The 75/25 Rule)

As per the latest 2026 norms, if you leave a job, you don't get 100% immediately.

- After 1 Month of Unemployment: You can usually withdraw up to 75% of your balance.

- After 2 Months of Unemployment: You can withdraw the remaining 25% for a full settlement.

Scenario C: Short Service (Under 5 Years)

Even if the portal shows you can withdraw a certain amount, doing so before 5 years of service might attract TDS (Tax Deducted at Source). Here, your Withdrawable Amount is effectively lower because the government takes a slice for taxes before it reaches your bank account.

PF TDS Rules. How to Fill Form 15G & 15H

6. Why Employer Share Is Sometimes Not Fully Withdrawable

'This is perhaps the biggest "shock" for employees. Your passbook shows two main columns: Employee Share and Employer Share.

You might think, "Both are part of my CTC (Cost to Company), so both are mine." While true in principle, the rules for the Employer Share are stricter:

- Pension Contribution: A significant portion of the "Employer's Share" actually goes into the EPS (Employees' Pension Scheme). This money isn't even part of your PF balance in the same way; it’s a credit toward a future monthly pension.

- Restrictive Access: For certain advanced categories, withdrawal is limited to the employee’s share. Employer contributions (and EPS portion) may not be fully available depending on the rule invoked.

- Policy-Driven: These restrictions are set by the Central Board of Trustees. Your employer has no power to "release" this money to you; only the EPFO rules can.

7. 4 PF Balance Situations That Commonly Mislead People

Don't let these four situations give you a false sense of liquidity:

- Old PF Accounts Not Transferred: You might see a high balance on an old UAN, but that amount isn't "withdrawable" until you transfer it to your current active account.

- Interest Shown but Not "Realized": Interest for the ongoing financial year is credited only after annual settlement. Interim balances shown may not include current-year accrued interest.

- Multiple PF Accounts: If you have four different PF accounts from four different jobs, you cannot withdraw from all of them simultaneously if they are unlinked. It is recommended to merge them to see your true withdrawable potential. Read How to Merge Multiple UANs

- Recently Updated Passbook: The passbook updates can lag. What you see today might not reflect a pending claim or a recent contribution, leading to "Claim Rejected" due to insufficient funds.

8. PF Money Withdrawal Time: What People Actually Mean

When users search for PF money withdrawal time, they are usually asking one of two very different questions.

"When can I apply?" (Eligibility Timing)

- For Advances: You can often apply as soon as the need arises (provided you meet the service criteria).

- For Full Settlement: You must wait 60 days after your "Date of Exit" is updated in the system.

"How long will EPFO take?" (Processing Time):

Once you hit the 'Submit' button on the UAN portal, the PF money withdrawal time typically ranges from 7 to 20 working days. However, if your KYC is updated and your Aadhaar is linked, many "Auto-Claims" are now being settled within 3 to 4 days.

Note: Seeing the balance in your portal does not mean the money is ready for immediate transfer. The balance is just a ledger entry; the "settlement" is a manual or algorithmic verification process.

9. PF Status Terms You See & How to Interpret Them

The EPFO portal can be a source of high anxiety. You might check your PF balance withdrawal status and see various labels. Here is how to decode them:

- Active PF Account: This means contributions are currently being made, or the account is live. You are likely only eligible for advances.

- Inoperative / Old PF Account: If no contributions have been made for 36 months, the account becomes inoperative. Interest continues to accrue, but you may need extra verification to withdraw.

- Claim Under Process: Your application has reached the regional PF office. The money has not yet left the EPFO's hands.

- Settled: The EPFO has approved the payment.

- Rejected: The claim was denied. Common reasons include "Member name mismatch," "Cheque leaf not clear," or "Ineligible for the applied Para."

10. What Happens to the Remaining PF Amount?

The remaining 25% of your PF amount does not go anywhere, it stays there invested:

- Stays Invested: The remaining balance continues to earn interest at the rate declared by the EPFO (~ 8.25%).

- Becomes Withdrawable Later: That 25% isn't "lost"; it's just "delayed." Once you meet the criteria for a full settlement (2 months of unemployment), you can claim every single rupee.

- Compounding Benefits: Even a small remaining amount can grow significantly over a decade.

Reassurance: Unwithdrawn PF does not disappear; it remains yours, earning interest in a sovereign-backed fund.

11. PF Balance vs Withdrawable Amount vs Claim Amount

To clear the air, let's look at the "Holy Trinity" of PF terminology:

| Term | What It Refers To | Example |

| PF Balance | Total savings in your name. | ₹10,00,000 |

| Withdrawable Amount | The maximum the law allows you to take. | ₹6,00,000 |

| Claim Amount | The specific amount you choose to ask for. | ₹4,00,000 |

You should not set your Claim Amount higher than your Withdrawable Amount. System auto-restricts claims in most online Form-31 filings. The claim may get short-settled or rejected.

12. Conclusion

Navigating the world of EPFO can often feel like solving a puzzle where the rules change just as you think you’ve figured them out. However, as we’ve explored in this 2026 guide, the distinction between PF Balance vs. Withdrawable Amount exists for a vital reason: to protect your future financial independence.

While it can be disheartening to see a large balance that you cannot fully touch, it is important to view your EPF not as a standard savings account, but as a "locked vault" for your retired self. The restrictions on your withdrawable amount are essentially the walls of that vault, ensuring that while you can access funds for genuine emergencies and milestones, the core of your wealth remains intact and continues to grow through the power of compounding interest.

By aligning your expectations with the current EPFO rule framework, considering your employment status, years of service, and the specific reason for your claim. You can avoid the frustration of rejected claims and "short-settled" amounts. Your money isn't going anywhere; it’s simply waiting for the right time to be used.

File your PF Claim on the Unified Portal

Useful Links & Official Resources

EPFO Official Portals

- Employees' Provident Fund Organisation Official Websitehttps://www.epfindia.gov.in

- EPFO Unified Member Portal (File PF withdrawal claims, check KYC, update details)https://unifiedportal-mem.epfindia.gov.in/memberinterface/

- EPFO Passbook Portal (Check PF balance and contribution history)https://passbook.epfindia.gov.in/MemberPassBook/Login

EPF Forms & Download Links

Form 19 Purpose: Final PF settlement after leaving employment Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form19.pdf

Form 31 Purpose: PF advance withdrawal (medical, housing, etc.)Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form31.pdf

Form 10C Purpose: Withdrawal benefit or EPS scheme certificate Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form10C.pdf

Form 10D Purpose: Monthly pension claim under EPS 1995Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form10D.pdf

Form 15G Purpose: Declaration to avoid TDS on PF withdrawal (if eligible) Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form15G.pdf

Form 15H Purpose: TDS declaration for senior citizens Download: https://www.epfindia.gov.in/site_docs/PDFs/Downloads_PDFs/Form15H.pdf

Pension & Retirement Information

- Employees' Pension Scheme (EPS) official overviewhttps://www.epfindia.gov.in/site_en/Pension.php

- EPF Interest Rate Announcementshttps://www.epfindia.gov.in/site_en/Interest.php

Grievance & Claim Support

If your PF claim is rejected, delayed, or short-settled, you can file an official grievance through:

- EPFiGMS Grievance Portalhttps://epfigms.gov.in

11. FAQs

Is the PF balance the same as the withdrawable amount?

No. Your PF balance is the total money in the pot. The withdrawable amount is the "ladle-full" the EPFO allows you to scoop out based on your current eligibility and reason.

Why can’t I withdraw my full PF balance?

Because the EPF is a social security tool. If you are currently employed, the law assumes you don't need your retirement corpus yet. Full withdrawal is generally reserved for retirement or prolonged unemployment.

Does PF balance reduce automatically after withdrawal?

Yes. Once your claim is settled, the amount is debited from your balance. Your passbook will show a "Claim Settled" entry, and your remaining balance will start earning interest on the new, lower principal.

Can my withdrawable amount change later?

Yes! As you complete more years of service (e.g., crossing the 5-year or 7-year mark), your eligibility for different types of advances increases, often increasing your withdrawable limit.

Is the withdrawable amount shown anywhere on the EPFO portal?

Not explicitly. The portal will show you your Balance, but you only find out the Withdrawable Amount when you select a "Reason" in the online claim form. The system then calculates your limit in the background.

How Kustodian Can Help!

Navigating EPFO technicalities can be frustrating, especially when your claim is rejected or your details are mismatched. Kustodian.life acts as your personal PF advocate, bridging the gap between you and the regional office.

- Audit & Health Check: We perform a thorough audit of your PF account to identify potential "blockers" like KYC errors or duplicate UANs before you apply.

- Correction Assistance: From correcting Name/DOB mismatches to updating outdated Aadhaar and bank details, we streamline the verification process.

- Stuck Claim Resolution: If your withdrawal is stuck or rejected repeatedly, our experts step in to resolve technical hurdles and coordinate with employers/EPFO offices.

- Legacy Claims: We specialise in merging multiple old accounts into your current UAN, ensuring your total balance is unified and withdrawable.

Disclaimer: This article is for informational purposes only and does not constitute legal or financial advice. Rules may vary based on individual records and EPFO processing.

![Why E-Khata Applications Get Rejected in Bangalore (And How to Fix Them) [2026]](/_next/image?url=https%3A%2F%2Fwebsite-assets-wix.s3.ap-south-1.amazonaws.com%2Fimages%2Fposts%2F3031ceb9f0274289aad5c5f140be716f.webp&w=828&q=75)